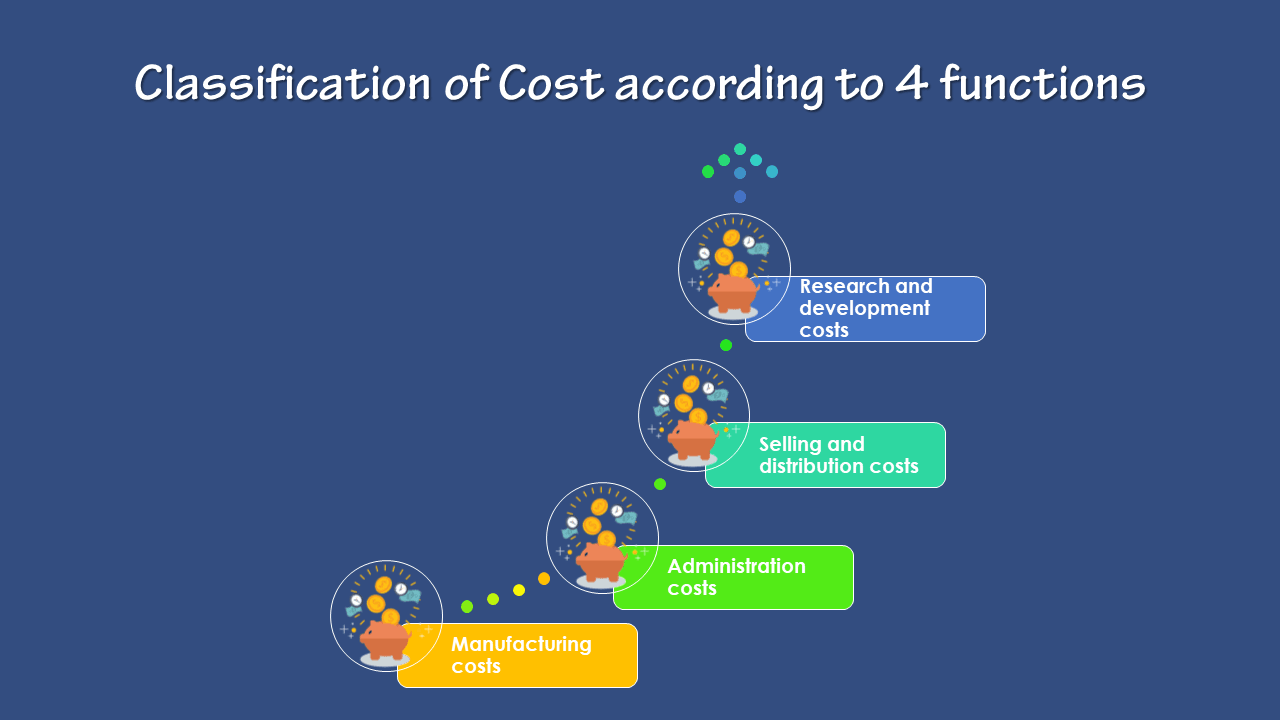

Classification of Cost according to 4 functions: This is a traditional classification. A business has to perform several functions like manufacturing, administration, selling, distribution, and research.

This article explains the topic of the Classification of Cost according to 4 functions.

Cost may have to ascertain for each of these functions.

On this basis, costs are classifying into the following groups:

How to the Classification of Cost according to 4 functions?

Manufacturing costs:

This is the cost of the sequence of operations. Which begins with supplying materials, labor, and services and ends with the completion of production. What are the manufacturing costs? Manufacturing costs are the costs of materials plus the costs to convert the materials into products. Manufacturing costs are the costs incur during the production of a product.

The costs are typically present in the income statement as separate line items. An entity incurs these costs during the production process. Direct material is the materials uses in the construction of a product. Direct labor is that portion of the labor cost of the production process that assigns to a unit of production. Manufacturing overhead costs are applying to units of production based on a variety of possible allocation systems. Such as by direct labor hours or machine hours incurred.

Administration costs:

This is general administrative cost and includes all expenditure incurs in formulating the policy, directing the organization and controlling the operations of an undertaking. Which is not directly related to production, selling and distribution, research and development activity or function.

Define administrative costs as the costs not directly related to operations. Generally, they are incurring in the process of directing a company. These costs, though indirect, are still important because they assist those who operate and sell company products by making their work more efficient.

Selling and distribution costs:

Selling cost is the cost of seeking to create and simulating demand and securing orders. Distribution cost is the cost of a sequence of operations. This begins with making the packed product available for despatch and ends with making the reconditioned returned empty package for re-use. There are some overhead about them;

What is Selling Overhead? Selling overhead is the indirect expenses incur for seeking to create and stimulate demand for the product and up to the stage of securing orders.

What is Distribution Overhead? Distribution overhead is the expenses incurred in connection with the execution of an order. It begins with making the packed product available for dispatch and ends with making the reconditioned empty package, if any, available for re-use.

The various items included in manufacturing administrative, selling and distribution costs ate available in Table:

Functional Classification of Costs – Table.

Research and development costs:

Research cost is the cost of searching for new or improved products or methods. It comprises wages and salaries of research staff, payments to outside research organizations, materials used in laboratories and research departments, etc. After completion of research, the management may decide to produce a new improved product or to employ a new or improved method.

Development cost is the cost of the process which begins with the implementation of the decision to produce a new product or to employ a new or improved method and ends with the commencement of formal production of that product or by that method. Pre-production cost is that part of the development cost which incurs in making in trial production run preliminary to formal production.

Top 17 Cost concepts in Cost accounting:They are; 1) Product and period costs, 2) Common and joint costs, 3) Short-run and long-run costs, 4) Past and future costs, 5) Controllable and non-controllable costs, 6) Replacement and Historical Costs, 7) Escapable and unavoidable costs, 8) Out of pocket and Book Costs, 9) Imputed and Sunk Costs, 10) Relevant and Irrelevant Costs, 11) Opportunity and Incremental Costs, 12) Conversion cost, 13) Committed cost, 14) Shutdown and Abandonment costs, 15) Urgent and Postponable costs, 16) Marginal cost, and 17) Notional cost.

Here are important topic or questions is Discussion; What is the Cost concepts in Cost accounting?

A clear understanding of various cost concepts is essential for the study of cost accounting and cost systems.

Top 17 Cost concepts in Cost accounting – List

The description of these cost concepts follows now for cost accounting.

1] Product and period costs:

First Cost concepts; The product cost is the aggregate of costs that are associated with a unit of product. Such Costs may or may not include an element of overheads depending upon the type of costing system in force-absorption or direct. Product costs are related to goods produce or purchase for resale and are initially identifying as part of the inventory.

These products or inventory costs become expenses in the form of the cost of goods sold only when the inventory sales. Product cost associated with the unit of output. The costs of inputs informing the product viz., the direct material, direct labor, factory overhead constitute the product costs. The period cost is a cost that tends to be unaffecting by changes in the level of activity during a given period. What is the importance of Cost accounting?

The period cost associative with a period rather than manufacturing activity and these costs deduct as expenses during. The current period without have been previously classifying as product costs. Selling and distribution costs are period costs and are deducting from the revenue without their existence regard as part of the inventory cost.

2] Common and joint costs:

The common cost is an indirect cost that incurs for the general benefit of several departments or for the whole enterprise and which is necessary for present and future operations. The joint costs are the cost of either a single process or a series of processes. That simultaneously produce two or more products of significant relative sales value.

3] Short-run and long-run costs:

The short-run costs are costs that vary with the output when fixed plant and capital equipment remain the same and become relevant. When a firm has to decide whether or not to produce more in the immediate future. The long-run-costs are those which vary with the output when all input factors including plant and equipment vary and become relevant. When the firm has to decide whether to set up a new plant or to expand the existing one.

The past costs are actual costs incur in the past and are generally containing in the financial accounts. These costs report past events and the time lag between event and its reporting makes the information out of date and irrelevant for decision-making.

These costs will just act as a guide for the future course of action. The future costs are costs expecting to incur at a later date and are the only costs that matter for managerial decisions because they are subject to management control.

Future costs are relevant for managerial decision making in cost control, profit projections, appraisal of capital expenditure, the introduction of new products, expansion programs, and pricing, etc.

5] Controllable and non-controllable costs:

The concept of responsibility accounting leads directly to the classification of costs as controllable or uncontrollable. The controllable cost is a cost chargeable to a budget or cost center. Which can influence the actions of the person in whom control the center vests? It is always not possible to predetermine responsibility, because the reason for deviation from expected performance may only become evident later.

For example, excessive scrap may arise from inadequate supervision or latent defect in purchased material. The controllable cost is a cost that can influence and regulate during a given period by the actions of a particular individual within an organization. The controllability of cost depends upon the level of responsibility under consideration.

Direct costs are generally controllable by shop level management. The uncontrollable cost is a cost that is beyond the control of a given individual during a given period. The distinction between controllable and uncontrollable costs are not very sharp and may be left to individual judgment. Some expenditure which may uncontrollably on a short-term basis controllably on a long-term basis,

There are certain costs which are difficult to control due to the following reasons.

Physical hazards arising due to flood, fire, strike, lockout, etc.

Economic risks such as increased competition, change in fashion or model, higher prices of inputs, import restrictions, etc.

Political risks like change in Government policy, political unrest, war, etc.

Technological risk such as a change in design, know-how, etc.

6] Replacement and Historical Costs:

The Replacement costs and Historical costs are two methods for carrying assets in the balance sheet and establishing the amounts of costs that use to determine income.

The Replacement cost is a cost at which material identical to that is to replace could purchase at the date of valuation (as distinct, from actual cost price at the date of purchase). The replacement cost is the cost of replacing an asset at any allow point of time either present or the future (excluding any element attributable to improvement).

The Historical cost is the actual cost, determined after the event. Historical cost valuation states the costs of plant and materials, for example, at the price originally paid for them whereas replacement cost valuation states the costs at prices that would have to pay currently.

Costs reported by conventional financial accounts are based on historical valuations. But during periods of changing price level, historical costs may not be the correct basis for projecting future costs. Naturally historical costs must adjust to reflect current or future price levels.

7] Escapable and unavoidable costs:

The Escapable cost is an avoidable cost that will not incur if an activity does not undertakes or discontinue. The avoidable cost will often correspond-with variable costs. The avoidable cost can identify with an activity or sector of a business and which would avoid if that activity or sector did not exist. The escapable costs refer to costs that can reduce due to the contraction in the activities of a business enterprise. It is the net effect on costs that is important, not just the costs directly avoidable by the contraction. Examples:

Closing an unprofitable branch house-storage costs of other branches and transportation charges would increase.

Reducing credit sales costs estimated may be less than the benefits otherwise available.

Note: Escapable costs are different from controllable and discretionary costs.

8] Out of pocket and Book Costs:

The out of pocket cost is a cost that will necessitate a corresponding outflow of cash. Also, the costs involving cash outlay or payment to other parties term as out of pocket costs. Book costs are those which do not require current cash payments.

Depreciation is a notional cost in which no cash transaction involves. The distinction between out of pocket costs and book costs primarily shows how costs affect the cash position.

Out of pocket costs are relevant in some decision-making problems. Such as the fluctuation of prices during the recession, make or buy decisions, etc. Book-costs can convert into out of pocket costs by selling the assets and having the item on hire. Rent would then replace depreciation and interest.

9] Imputed and Sunk Costs:

The imputed cost is a cost that does not involve actual cash outlay. Which uses only for decision making and performance evaluation. Imputed cost is a hypothetical cost from financial accounting. Interest on capital is a common type of imputed cost. No actual payment of interest makes but the basic concept is that had the funds been investing elsewhere they would have to earn interest. Thus, imputed costs are a type of opportunity costs.

The Sunk costs are those costs that have been investing in a project and which will not recover if the project terminates. The sunk cost is one for which the expenditure has to take place in the past. This cost does not affect a particular decision under consideration. Sunk costs are always results of decisions accept in the past.

This, the cost cannot change by any decision in the future. Investment in plant and machinery as soon as it installs its cost is sunk cost and is not relevant for decisions. Amortization of past expenses e.g. depreciation is sunk cost. Sunk, costs will remain the same irrespective of the alternative selected.

Thus, it need not consider by the management in evaluating the alternatives as it is common to all of them. It is important to observe that an unavoidable cost may not be a sunk cost. The Managing Director’s salary is generally unavoidable and also out of pocket but not sunk cost.

10] Relevant and Irrelevant Costs:

The relevant cost is a cost appropriate in aiding to make specific management decisions. Business decisions involve planning for the future and consideration of several alternative courses of action. In this process, the costs which are affecting by the decisions are future costs. Such costs call relevant costs because they are pertinent to the decisions in hand. The cost is saying to be relevant if it helps the manager in taking. The right decision in furtherance of the company’s objectives.

11] Opportunity and Incremental Costs:

The opportunity cost is the value of a benefit sacrifice in favor of an alternative course of action. It is the maximum amount that could obtain at any given point of time. If a resource was selling or put to the most valuable alternative use that would be practicable.

The opportunity cost of a good or service measure in terms of revenue. Which could have been earning by employing that good or service in some other alternative uses. Opportunity cost can define as the revenue forgone by not making the best alternative use. Opportunity cost is the prospective change in cost following the adoption of an alternative machine process, raw materials, etc. It is the cost of opportunity lost by the diversion of an input factor from use to another.

The incremental cost is the extra cost of taking one course of action rather than another. It also calls at different costs. The incremental cost is the additional cost due to a change in the level of nature of the business activity.

The change may take several forms e.g., changing the channel of distribution, adding a new machine, replacing a machine by a better machine, execution of export orders, etc. Incremental costs will be different in case of different alternatives. Hence, incremental costs are relevant to the management in the analysis of decision making.

12] Conversion cost:

The conversion cost is the cost incur for converting the raw material into the finished product. It refers to as the production cost excluding the cost of direct materials:

13] Committed cost:

The committed cost is a cost that primarily associates with maintaining the organization’s legal and physical existence over which management has little discretion. Also, the committed cost a fixed cost that results from the froth decision of the prior period.

The amount of committed cost as fixed by decisions. Which makes in the past and not subject to managerial control in the short-run? Since committed cost does not fluctuate with volume and remains unchanged until action takes to increase or reduce available capacity.

Committed cost does not present any problem in cost behavior analysis. Examples of committed costs are depreciation, insurance premium, rent, etc. This is an important Cost concept in accounting.

14] Shutdown and Abandonment costs:

The shutdown costs are the cost incur about the temporary closing of a department/division/enterprise. Such costs include those of closing as well as those of re-opening. Also, the shutdown costs asses as those costs which would incur in the event of suspension of the plant operation. And, which would save if the operations are continuing. Examples of such costs are the costs of sheltering the plant and equipment and construction of sheds for storing exposed property.

Further, additional expenses may have to incur when operations are restoring e.g.. Re-employment of workers may involve the cost of recruitment and training. The Abandonment cost is the cost incur in closing down. Also, A department or a division or in withdrawing a product or ceasing to operate in a particular sales territory etc.. The abandonment costs are the cost of retiring altogether a plant from service; Abandonment arises when there is a complete cessation of activities and creates a problem as to the disposal of assets.

15] Urgent and Postponable costs:

The urgent costs are those which must incur to continue operations of the firm. For example, the cost of material and labor must incur if production is to take place. The Postponable cost is that cost which can shift to the future with little or no effect on the efficiency of current operations. These costs can postpone at least for some time, e.g., maintenance relating to building and machinery.

16] Marginal cost:

The marginal cost is the variable cost of one unit of a product or a service i.e., a cost that would avoid. If the unit did not produce or provide. In this context, a unit in usually either a single article or a standard measure such as a liter or kilogram. But may in certain circumstances be an operation, process or part of an organization.

They are the amount at any allow volume of output by which aggregate costs are changing. If the volume of output increases or decreases by one unit. It uses full Cost concepts in accounting.

The marginal costing technique is the process of ascertaining marginal costs and of the effects of changes in the volume of the type of output on profit by differentiating between fixed and variable costs.

17] Notional cost:

Final Cost concepts; The Constitutional or notional cost is hypothetical to take into account in a particular situation to re-present. As well as, the benefits enjoying by an entity in respect of which no actual expense incurs. Maybe you understand your misinformation of the cost concepts in cost accounting.

What is the Cost concepts in Cost accounting? Discussion.

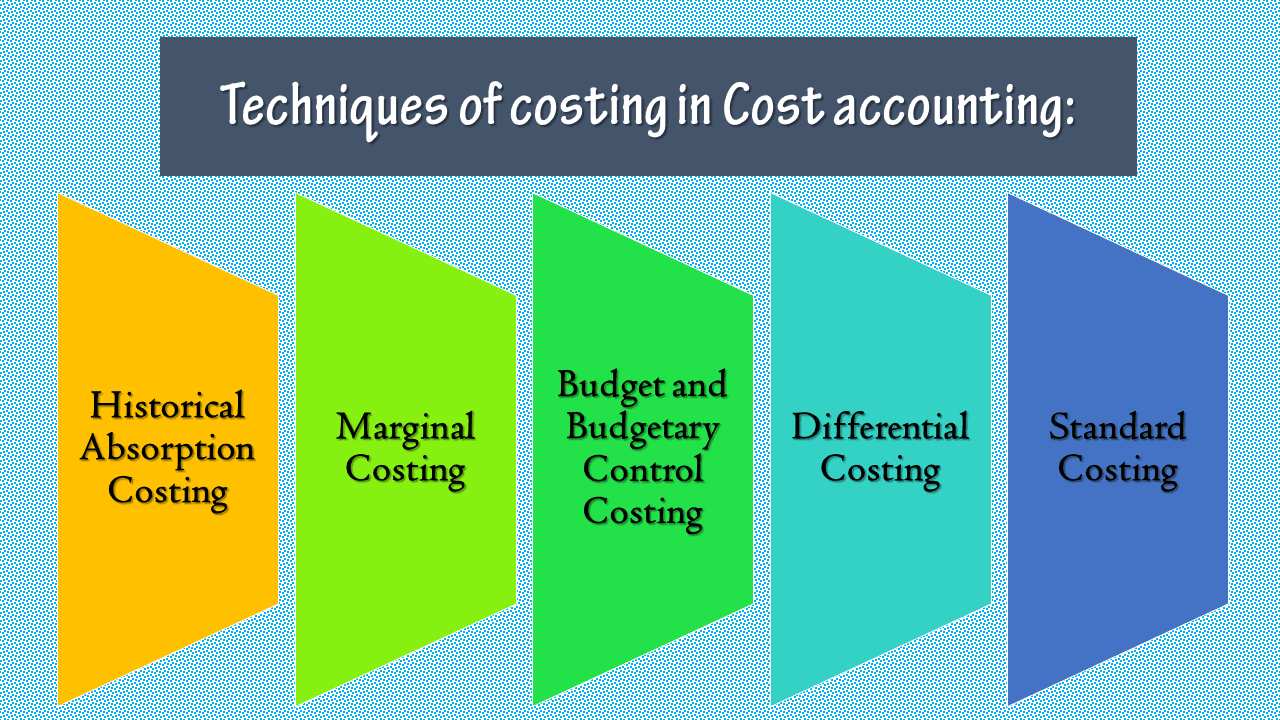

The techniques and methods of costing in Cost accounting are to explain their points one by one. First, Techniques of Costing:Historical Absorption, Marginal, Budget and Budgetary Control, Differential, and Standard Costing. As well as Methods of Costing: There are two methods of costing, namely; Job costing and Process costing.

What are the techniques and methods of costing in Cost accounting? Discussion.

In addition to the different costing methods, various techniques are also using to find the costs.

It’s the ascertainment of costs after they have been incurring. It defines as the practice of charging all costs, both variable and fixed, to operations, process or products. It also knows as traditional costing. Its ascertainment of costs after they have been incurring. It aims at ascertaining costs incurred on work done in the past.

It has a limited utility, though comparisons of costs over different periods may yield good results. Since costs are ascertaining after they have been incurring, it does not help in exercising control over costs. However, It is useful in submitting tenders, preparing job estimates, etc.

2] Marginal Costing:

It refers to the ascertainment of costs by differentiating between fixed costs and variable costs. In this technique, fixed costs are not treated as product costs. They are recovering from the contribution (the difference between sales and variable cost of sales).

The marginal or variable cost of sales includes direct material, direct wages, direct expenses, and variable overhead. It is the ascertainment of marginal cost by differentiating between fixed and variable costs.

It uses to ascertain the effect of changes in volume or type of output on profit. This technique helps management in taking important policy decisions such as product pricing in times of competition, whether to make or not, selection of product mix, etc.

3] Budget and Budgetary Control Costing:

A budget is a quantitative statement preparing before the defined period to help achieve certain objectives of the firm. When we talk about the techniques of costing, budgetary control is an important technique. This budget can be in the form of quantities or can be a monetary statement. A budget will lay down the objectives of this period, and the firm’s methods to achieve them.

For example, a production budget will deal with quantities of goods to produce. On the other hand, a marketing budget will be a monetary statement. Another important feature of a budget is that it prepares ahead of time. So the budget can be for the next quarter or the next year or any such predetermined period.

Budgetary control is the preparation of budgets and analysis of the actual performance of the firm in comparison to the budgeted numbers. If there is a lot of variation from the budget the firm can take corrective action. This is how budgetary control works.

4] Differential Costing:

Differential cost is the difference in total cost between alternatives-evaluate to assist decision making. This technique draws the curtain between variable costs and fixed costs. It takes into consideration fixed costs also (unlike marginal costing) for decision making under certain circumstances.

This technique considers all the revenue and cost differences amongst the alternative courses, of action to assist management in arriving at an appropriate decision.

5] Standard Costing:

It refers to the ascertainment and use of standard costs and the measurement and analysis of variances. Standard cost is a predetermining cost that computes in advance of production based on a specification of all factors affecting costs. A comparison makes of the actual cost with a pre-arranged standard cost and the cost of any deviation (called variances) analyzes by causes.

This permits management to investigate the reasons for these variances and to take suitable corrective action. The standards are fixed for each element of cost. To find out variances, the standard costs are comparing with actual costs. The variances are investigating later on and wherever necessary, rectification steps are initiating promptly. The technique helps in measuring the efficiency of operations from time to time.

Methods of Costing:

In this article, we are studying the topic techniques and methods of costing. After discussing the topic of Costing Techniques, so now we can study the topic of Costing Methods. The basic principles of ascertaining costs are the same in every system of cost accounting. However, the methods of analyzing and presenting the cost may vary from industry to industry. The method to use in collecting and presenting costs will depend upon the nature of production.

The methods of costing in Cost accounting

There are two methods of costing, namely: Job costing and Process costing.

A] Job costing:

Job costing uses where production is not repetitive and is done against orders. The work usually carries out within the factory. Each job treats as a distinct unit, and related costs are recording separately. This type of costing is suitable for printers, machine tool manufacturers, job foundries, furniture manufactures, etc.

The following methods are commonly associated with job costing:

1] Batch costing:

Where the cost of a group of product ascertains, it calls “batch costing”. In this case, a batch of similar products treats as a job. Costs are collecting according to batch order number and the total cost divide by the numbers in a batch to find the unit cost of each product. Batch costing generally follows in general engineering factories that produce components in convenient batches, biscuit factories, bakeries, and pharmaceutical industries.

2] Contract costing:

A contract is a big job and, hence, takes a longer time to complete. For each contract, the account keeps recording related expenses separately. It usually follows by concerns involve in construction work e.g. building roads, bridges, and buildings, etc.

B] Process Costing:

Where an article has to undergo distinct processes before completion, it is often desirable to find out the cost of that article at each process. A separate account for each process opens and all expenses are charging thereon. The cost of the product at each stage is, thus, accounted for.

The output of one process becomes the input to the next process. Hence, the process cost per unit in different processes adds to find out the total cost per unit at the end. Process costing is often found in such industries as chemicals, oil, textiles, plastics, paints, rubber, food processors, flour, glass, cement, mining, and meatpacking.

The following methods are used in process costing:

1] Output/Unit Costing:

This method follows by concerns producing a single article or a few articles which are identical and capable of being expressed in simple, quantitative units. This uses in industries like mines, quarries, oil drilling, cement works, breweries, brickworks, etc. for example, a tone of coal in collieries, one thousand bricks in brickworks, etc.

The object here is to find out the cost per unit of output and the cost of each item of such cost. A cost sheet prepares for a definite period. The cost per unit calculates by dividing the total expenditure incurred during a given period by the number of units produced during the same period.

2] Operating Costing:

This method is applicable where services are rendering rather than goods produce. The procedure is the same as in the case of unit costing. The total expenses of the operation are divide by the units and cost per unit of service arrives at. This follows in transport undertakings, municipalities, hospitals, hotels, etc.

3] Multiple Costing:

Some products are so complex that no single system of costing is applicable. Where a concern manufactures several components to assemble into a complete article, no one method would be suitable, as each component differs from the other in respect of materials and the manufacturing process.

In such cases, it is necessary to find out the cost of each component and also the final product by combining the various methods discussed above. This type of costing follows to cost such products as radios, airplanes, cycles, watches, machine tools, refrigerators, electric motors, etc.

4] Operating Costing:

In this method, each operation at each stage of production or process is separately identifying and cost. Also, the procedure is somewhat similar to the one followed in process costing. Process costing involves the costing of large areas of activity whereas operation costing confines to every minute operation of each process.

This method follows in industries with a continuous flow of work, producing articles of a standard nature, and which pass through several distinct operations sins a sequence to completion. Since this method provides for minute analysis of cost, it ensures greater accuracy and better control of costs.

The costs of each operation per unit and cost per unit up to each stage of operation can calculate quite easily. This method is in force in industries were toys, leather, and engineering goods are manufacturing.

5] Departmental Costing:

When costs are ascertaining department by department, such a method calls “departmental costing“. Where the factory divides into several departments, this method follows. The total cost of each department ascertains and divides by the total units produced in that department to obtain the cost per unit. This method follows departmental stores, publishing houses, etc.

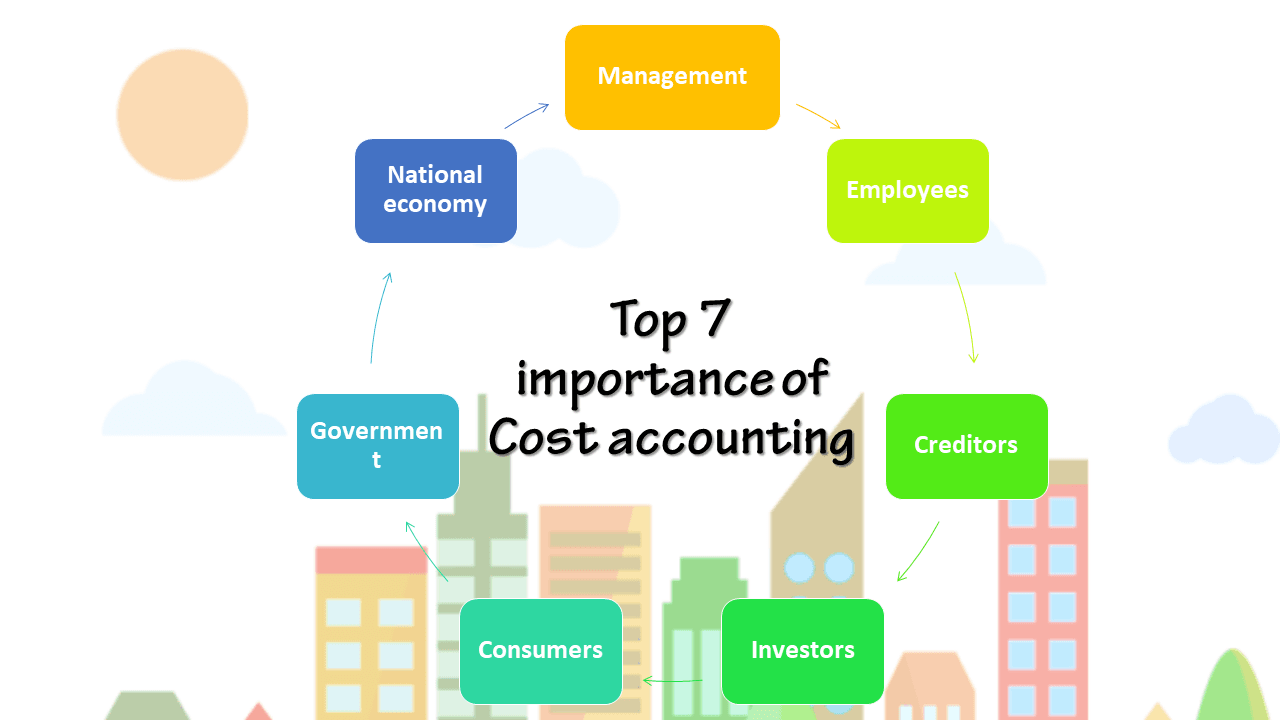

Importance of Cost accounting: Cost accounting is the accounting of the cost. It is made of two words-Cost and Accounting. This article explains the 7 important, the importance of Cost accounting: Management, Employees, Creditors, Investors, Consumers, Government, and National economy. The term cost denotes the total of all expenditures involved in the process of production. The shortcomings inherent in financial accounting have made the management to realize the importance of cost accounting. Whatever may be the type of business, it involves the expenditure on labor, materials and other items required for manufacturing and disposing of the product.

Here are answering the questions of What is the importance of Cost accounting?

Thus, it covers the costs involved in the production and the cost involved while receiving it. Moreover, big busyness requires delegation responsibility, division of labor and specialization. Management has to avoid the possibility of waste at each stage. Also, management has to ensure that no machine remains idle, efficient labor gets due initiative, proper utilization of by-products is made and costs are properly ascertaining.

Besides management, creditors and employees are also benefiting in numerous ways by the installation of a good costing system in an industrial organization. Cost accounting increases the overall productivity of an industrial establishment and, therefore, serves as an important tool in bringing prosperity to the nation.

Accounting, on the other hand, collects and maintains financial records of each income and expenditure and make avail of such information to the concerned officials. Thus, cost accounting is a practice and process of cost which determines the profitability of a business concern by controlling the cost with the application of accounting principle, process, and rules. Cost accounting includes the presentation of the information derived therefrom for purposes of managerial decision making.

Thus, cost accounting is an art as well as science. It is a science because it is a body of systematic knowledge having certain principles. It is an art as it requires the ability and skill with which a cost accountant can apply the principles of cost accounting in various managerial problems.

Definition:

The following definitions below are:

According to W.W.Bigg,

“Cost accounting is the provision of such analysis and classification of expenditure as will enable the total cost of any particular unit of production to be ascertained with a reasonable degree of accuracy and at the same time to disclose exactly how much total cost is constituted.”

According to R.N. Carter,

“Cost accounting is a system of recording in accounts the materials used and labor employed in the manufacture of a certain commodity or on a particular job.”

Top 7 importance of Cost accounting:

Thus, the importance of cost accounting in various spheres can summarize under the following headings:

Cost accounting provides an invaluable aid to management. It is so closely allied to management that it is difficult to indicate where the work of the cost accountant ends and managerial control begins. Adequate costing data help management in reaching certain important decisions such as, whether hand labor should replace by the machinery or not; whether a particular product line should discontinue or not etc. Costing checks recklessness and avoids the occurrence of mistakes.

Costs can reduce by the proper organization of the plant and executive personnel. As an aid to management, it also provides important information to enable management, to maintain effective control over stores and inventory, to increase the efficiency of the business, and to check waste and losses. It facilitates the delegation of responsibility for important tasks and ratings of employees. However, for all this, the management must be capable of using properly the information provided by the cost accounts.

The various advantages derived by managements on account of a good costing system can put as follows:

A] Useful in periods of depression and competition:

During trade depression, the business cannot afford to have leakages which pass unchecked. The management should know where economies may seek, waste eliminated and efficiency increased. The business has to wage a war for its survival. As well as, the management should know the actual cost of their products before embarking on any scheme of reducing the prices or giving tenders. The costing system facilitates this.

B] Helps in, pricing decisions:

Though economic law of supply and demand and activities of the competitors, to a great extent, determine the price of the article, the cost to the producer does play an important part. Also, the producer can take necessary guidance from his costing records.

C] Helps in estimates:

Adequate costing records provide a reliable basis upon which tenders and estimates may prepare. The chances of losing a contract on account of over-rating or the loss in the execution of a contract due to under-rating can minimize. Thus, ascertained costs provide a measure for estimates, a guide to policy, and control over current production.

D] Cost Accounting helps in channelizing production on the right lines:

Costing makes possible for the management to distinguish between profitable and non-profitable activities. Profits can maximize by concentrating or profitable operations and eliminating non-profitable ones.

E] Helps in reducing wastage:

As it is possible to know the cost of the article at every stage, it becomes possible to check various forms of waste, such as time, expense, etc., or in the use of machinery, equipment, and tools.

F] Costing makes comparison possible:

If the costing records are regularly kept, comparative cost data for different periods and various volumes of production will be available. It will help the management in informing future lines of action.

G] Provides data for periodical profit and loss accounts:

Adequate costing records supply to the management such data as may be necessary for the preparation of profit and loss account and balance sheet, at such intervals as may desire by the management. It also explains in detail the sources of profit or loss revealed by the financial accounts, thus helps in the presentation of better information before the management.

H] Costing results in increased efficiency:

Losses due to wastage of materials, idle time of workers, poor supervision, etc. will disclose if the various operations involved in manufacturing a product are studied by a cost accountant. Also, the efficiency can measure and costs controlled and through it, various devices can frame to increase efficiency.

I] Costing helps in inventory control and cost reduction:

Costing furnishes control which management requires in respect of stock of materials work-in-progress and finished goods. Costs can reduce in the long-run when alternates are tried. This is particularly important in the present-day context of global competition. Cost accounting has assumed special significance beyond, cost control this way.

J] Helps in increasing productivity:

The productivity of material and labor is requiring to increase to have growth and more profitability in the organization. Costing renders great assistance in measuring productivity and suggest ways to improve it.

What is the importance of Cost accounting? Discussion

2] Cost Accounting and Employees:

Employees have a vital interest in their employer’s enterprise and the industry, in which they are employed. They are benefiting in many ways by the installation of an efficient costing system in their enterprise. Cost accounting helps to fix the wages of the workers. Efficient workers are rewarding for their efficiency. It helps to induce an incentive wage plan in business. Also, they are benefiting because of systems of incentives, bonus plans, etc. They get benefit indirectly through an increase in consumer goods and directly through continuous employment and higher remuneration.

3] Cost accounting and creditors:

Investors, banks and other moneylenders have a stake in the success of the business concern and, therefore, are benefit immediately by the installation of an efficient costing system. They can base their judgment on the profitability and further prospects of the enterprise upon the studies and reports submitted by the cost accountants.

4] Cost accounting and investors:

Investors can obtain benefit fro the cost accounting. Investors want to know the financial conditions and earning capacity of the business. Also, they must gather information about the organization before making investment decisions and investors can gather such information from cost accounting.

5] Cost accounting and consumers:

The ultimate aim of costing is to reduce the cost of production to minimize the profit of the business. Reduction in the cost usually passes on the consumers in the form of lower prices. They get quality goods at a lower price.

6] Cost accounting and Government:

Cost accounting is one of the prime sources to provide reliable data to internal as well as external parties. It helps government agencies to determine excise duty and income tax. As well as, they formulate tax policy, industrial policy, export and import policy based on the information provided by the cost accounting.

7] Cost accounting and national economy:

An efficient costing system brings prosperity to the concerned business enterprise resulting in stepping up of the government revenue. Also, the overall economic development of a country takes place due to an increase in the efficiency of production. Control of costs, elimination of wastages and inefficiencies lead to the progress of the industry and in consequence of the nation as a whole.

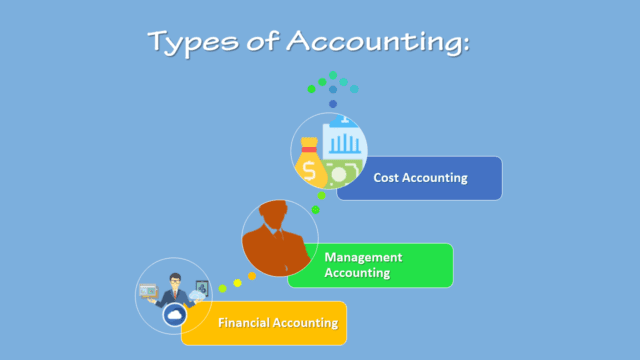

Types and utility of Accounting; This article in we discuss first the utility of accounting after that we will finally discuss the types of accounting. So, What is the utility of Accounting? There are three types and utility of accounting: financial, management, and also cost accounting. The preceding section only brought the importance of information to the fore. Effective decisions require accurate, reliable, and timely information. The quantity and quality requirement of information differs with the importance of that decision which should take based on that information.

Here are explains; The utility and types of Accounting, discussion each one.

Individuals can use accounting information to manage and manage their bank accounts, to evaluate job eligibility in the organization, to invest money, rent a house, and manage their routine matters. Business managers have to set goals, evaluate progress, and start corrective action in case of adverse deviations from planned courses of action.

Many such decisions require accounting information – purchasing equipment, maintenance of inventory, borrowing, and lending, etc. Investors and creditors are willing to evaluate the profitability and solvency of a company before giving benefits to the company. Therefore, they are interested in obtaining financial information about the company in which they are considering an investment.

Financial statements;

Financial statements are the main source of information for them, which are published in a company’s annual report and various financial dailies and journals. Government and regulatory agencies have the responsibility to direct a country’s Socio-economic system in such a way that it promotes the common good. For example, the Securities and Exchange Board of India (SEBI) makes it mandatory to disclose some financial information to the public investment for a company.

The government’s task of managing the industrial economy becomes simpler if accounting information such as profit, cost, tax, etc. is presented uniformly without any manipulation or “window-dressing”. Central and state governments make various taxes Therefore, taxation officials must know the company’s income to calculate the amount of the company tax.

The information generated by accounting helps them in such calculations and also helps in finding any attempt to tax evasion. Employees and trade unions use accounting information to resolve various issues related to wages, bonuses, profit sharing, etc. Consumers and the general public are also interest in knowing the amount of income earned by various business houses.

Accounting information helps in determining whether a company is overcharging or exploiting customers, whether companies are showing better business performance or not, whether the country is emerging from the economic recession, etc. The aspects are closely related to accounting information and our quality of life.

What are the types of Accounting?

The financial literature classifies accounting into two broad categories, viz, Financial Accounting, and Management Accounting. Financial accounting is primarily concerned with the preparation of financial statements whereas management accounting covers areas such as interpretation of financial statements, cost accounting, etc.

Types of Accounting – List

Both these utility and types of accounting are examining in below;

As mentioned earlier, financial accounting deals with the preparation of financial statements for the basic purpose of providing information to various interested groups like creditors, banks, shareholders, financial institutions, government, consumers, etc. Financial statements, i.e. the income statement and the balance sheet indicate. How the activities of the business have been conducting during a given period of time.

Financial accounting is charge with the primary responsibility for external reporting. The users of the information generated by financial accounting, like bankers, financial institutions, regulatory authorities, government, investors, etc. want the accounting information to be consistent to facilitate comparison.

Therefore, financial accounting is based on certain concepts and conventions. Which include a separate business entity, going concern concept, money measurement concept, cost concept, dual aspect concept, accounting period concept, matching concept, realization concept, and conventions of conservatism, disclosure, consistency, etc. All such concepts and conventions would deal with detail in subsequent lessons.

Importance of financial accounting;

The significance of financial accounting lies in the fact that it aids the management in directing and controlling the activities of the firm and to frame relevant managerial policies related to areas like production, sales, financing, etc.

However, it suffers from certain drawbacks which are discussing below;

The information provided by financial accounting is consolidating in nature. It does not indicate a break-up for different departments, processes, products, and jobs. As such, it becomes difficult to evaluate the performance of different sub-units of the organization.

Financial accounting does not help in knowing the cost behavior as it does not distinguish between fixed and variable costs.

The information providing by financial accounting is historical in nature and as such the predictability of such information is limited.

The management of a company has to solve certain ticklish questions like the expansion of business, making or buying a component, adding or deleting a product line, deciding on alternative methods of production, etc. The financial accounting information is of little help in answering these questions.

The limitations of financial accounting;

However, should not lead one to believe that it is of no use. It is the basic foundation on which other branches and tools of accounting analysis are based. It is the source of information, which can further analyze and interpreted according to the tailor-made requirements of decision-makers.

Management accounting is ‘tailor-made’ accounting. It facilitates management by providing accounting information in such a way. So, that it is conducive for policy-making and running the day-to-day operations of the business. Its basic purpose is to communicate the facts according to the specific needs of decision-makers by presenting. The information in a systematic and meaningful manner.

Management accounting, therefore, specifically helps in planning and control. It helps in setting standards and in case of variances between planning and actual performances. It helps in deciding the corrective action. An important characteristic of management accounting is that it is forward-looking. Its basic focus is one future activity to perform and not what has already happened in the past.

Since management accounting caters to the specific decision needs, it does not rest upon any well-defined and set principles. The reports generated by a management accountant can be of any duration– short or long, depending on the purpose. Further, the reports can prepare for the organization as a whole as well as its segments.

One important variant of management accounting is the cost analysis. Cost accounting makes elaborate cost records regarding various products, operations, and functions. It is the process of determining and accumulating the cost of a particular product or activity. Any product, function, job, or process for which costs are determining and accumulate, are calls cost centers. The basic purpose of cost accounting is to provide a detailed break- up of the cost of different departments, processes, jobs, products, sales territories, etc. So, that effective cost control can exercise.

Cost accounting also helps in making revenue decisions such as those related to pricing, product-mix, profit-volume decisions, expansion of business, replacement decisions, etc. The objectives of cost accounting, therefore, can summarize in the form of three important statements, viz, to determine costs. To facilitate planning and control of business activities and to supply information for short- and long-term decisions. Cost accounting has certain distinct advantages over financial accounting. Some of them have been discussing succeedingly.

Cost accounting system;

The cost accounting system provides data about profitable and non-profitable products and activities, thus prompting corrective measures. It is easier to segregate and analyze individual cost items and to minimize losses and wastages arising from the manufacturing process. Production methods can vary to minimize costs and increase profits. Cost accounting helps in making realistic pricing decisions in times of low demand, competitive conditions, technology changes, etc.

Various alternative courses of action can properly evaluate with the help of data generate by cost accounting. It would not be an exaggeration if it is saying that a cost accounting system ensures maximum utilization of physical and human resources. It checks frauds and manipulations and directs the employer and employees towards achieving the organizational goal.

What are the utility and types of Accounting? Discussion

Labor costs represent human contribution. Labor cost is sensitive. The second Major element of cost in most of the manufacturing undertakings is labor cost. Proper accounting and control of labor costs, therefore, constitutes one of the most important problems of management. In controlling labor costs, the problem is complicated by the human element.

Here are explain; What does Labor cost? Introduction, Meaning, and Control.

Introduction: Under the present political conditions with restive labor in an organized industry, it is very difficult to reduce labor costs. Therefore, proper control and accounting for labor costs are one of the most important problems of a business enterprise. But control of labor costs presents certain practical difficulties unlike the control of material cost. The human element in labor makes difficult the control of labor costs whereas materials, being inanimate, could subject to rigid control.

Labor is the most perishable commodity and as such should effectively utilize immediately. Labour, once lost, cannot recoup and is bound to increase the cost of production. On the other hand, materials, being durable, can use as and when required and can store without having to incur an immediate loss.

Meaning of Labor Cost:

Payment of remuneration to the workers for their service to the firm knows as labor payment. This is the second element of the total cost. It may be direct or indirect. If it treats as a direct expense, it will include prime cost and if it relates to the factory, it will treat as an item of factory cost. Direct labor costs or Direct wages represent the cost that is incurred directly to change the composition, form or condition of a product.

Its primary nature is that it can easily identify and allocated to specific cost units. It also varies directly with the volume of production/output. Indirect labor costs, on the other hand, are the number of wages paid to workers who are not related to change the form, composition of a product but they engage themselves to complete the product, e.g. Supervisor’s Salary works office staff salaries, etc.

Bakers Labor! #Pixabay.

It is interesting to note that the difference between direct labor costs/direct wages and indirect labor costs/indirect wages depends on the types of work/job done and at the same time, the conditions in which cost of labor incurred. Under the circumstances, some labor costs treated as direct whereas the same treats as indirect in some other cases.

So, they will treat as a direct one when; 1) the payment makes to the workers to change the composition of a product, and 2) identification of the job is possible. Similarly, labor costs will treat as indirect when; 1) the same is not directly related to change or form of a product, 2) identification is not possible.

Control of Labour Cost:

To control the cost of labor (both direct and indirect), it becomes necessary to study the behavior of labor, to control the attendance and departure of workers, measurement of performances, assessing the results, time and motion study, etc. It is the function of the management to control the cost of labor in every step whether the same is direct or indirect. Individual columns of timesheet and job cards should maintain direct and indirect labor costs for proper ascertaining and controlling the cost of labor.

We know that direct labor costs/direct wages an element of prime cost whereas indirect labor costs/indirect wages an element of factory cost. Direct labor cost can control easily as it relates to variable cost which varies with the quantity produced, i.e. if more quantity produces with the same rate of remuneration, a post per unit must reduce. But it is not so easy to control the indirect labor cost.

What does Labor cost? Introduction, Meaning, and Control. #Pixabay.

Control over Labor cost:

This is so because labor consists of a lot of different individuals, each with a different mental and physical capacity and each with a different personality.

Proper control over it involves the following:

Appropriate systems for recruitment and selection, training and placement of workers.

Satisfactory methods of labor remuneration.

Healthy working conditions consistent with legal requirements and competitive undertaking.

This cost incurs on the employees who engage directly in making the product. Their work can identify clearly in the process of converting. The raw materials into the finished product called direct labor costs. For example, wages paid to the workers engaged in the machining department, fabrication department, assembling department, etc.

Construction Labor; Direct and Indirect work! #Pixabay.

Indirect Labor Cost:

Indirect employees not directly associated with the conversion process. But assist in the process by way of supervision, maintenance, transportation of materials, material handling, etc. Their work benefits all the items being produced and cannot specifically identify with the individual products. Hence, the indirect labor cost should treat as production overhead. These costs will accumulate and apportion to different cost centers on an equitable basis and absorbed into product cost by applying the overhead absorption rates.

Items of Labour Cost:

They can analyze into the following:

Monetary benefits are payable immediately; Salaries and Wages, Dearness and other allowances, production incentive or bonus.

Monetary benefits after some time in the future; Employer’s contribution to P.F., E.S.I., Pension, Gratuity, Profit linked bonus, etc.

Non-monetary benefits (Fringe benefits); Free or subsidized food, free medical or hospital facilities, free or subsidized education to the employee’s children, free or subsidized housing, etc.

What is the Usefulness of Cost Accounting? The shortcomings inherent in financial accounting have made the management to realize the importance of cost accounting. Meaning: Usefulness of Cost accounting is the classifying, recording and appropriate allocation of expenditure for the determination of the costs of products or services, and the presentation of suitably arranged data for purposes of control and guidance of management. Whatever may be the type of business, it involves the expenditure on labor, materials and other items required for manufacturing and disposing of the product. Moreover, big business requires delegation of responsibility, the division of labor and specialization.

Know and understand the Usefulness of Cost Accounting to Managers.

Management has to avoid the possibility of waste at each stage. Management has to ensure that no machine remains idle, efficient labor gets due initiative, proper utilization of by-products makes and costs are properly ascertained.

Besides management, creditors and employees also benefit in numerous ways by the installation of a good costing system in an industrial organization. Cost accounting increases the overall productivity of an industrial establishment and, therefore, serves as an important tool in bringing prosperity to the nation.

How to understand the Usefulness of Cost Accounting to Manager?

The various advantages derived by management on account of a good costing system can be put as follows:

Costing helps in inventory control and cost reduction.

Costing furnishes control which management requires in respect of stock of materials, work-in-progress and finished goods. Costs can reduce in the long-run when alternates try. This is particularly important in the present-day context of global competition. Cost accounting has assumed special significance beyond cost control this way.

Costing makes comparison possible.

If the costing records are regularly kept, comparative cost data for different periods and various volumes of production will be available. It will help the management by informing future lines of action.

Provides data for periodical profit and loss accounts.

Adequate costing records supply to the management such data as may be necessary for the preparation of profit and loss account and balance sheet, at such intervals as may desire by the management. It also explains in detail the sources of profit or loss revealed by the financial accounts, thus helps in the presentation of better information before the management.

Costing results in increased efficiency.

Losses due to wastage of materials, the idle time of workers, poor supervision, etc. will disclose if the various operations involved in manufacturing a product study by a cost accountant. The efficiency can measure and costs controlled and through it, various devices can frame to increase efficiency.

Useful in periods of depression and competition.

During trade depression, the business cannot afford to have leakages which pass unchecked. The management should know where economies may seek, waste elimination and efficiency increase. The business has to wage a war for its survival. The management should know the actual cost of their products. Before embarking on any scheme of reducing the prices or giving tenders. The costing system facilitates this.

It helps in pricing decisions.

Though economic law of supply and demand and activities of the competitors, to a great extent. Determine the price of the article, the cost to the producer does play an important part. The producer can take necessary guidance from his costing records.

Helps in estimates.

Adequate costing records provide a reliable basis upon which tenders and estimates may prepare. The chances of losing a contract on account of over-rating or the loss in the execution of a contract due to under-rating can minimize. Thus, “Ascertained costs provide a measure for estimates, a guide to policy, and control over current production”.

It helps in channelizing production on the right lines.

Costing makes possible for the management to distinguish between profitable and non-profitable activities. Profits can maximize by concentrating or profitable operations and eliminating non-profitable ones.

It helps in reducing wastage.

As it is possible to know the cost of the article at every stage. It becomes possible to check various forms of waste, such as time, expense, etc., or in the use of machinery, equipment, and tools.

It helps in increasing productivity.

The productivity of material and labor requires to increase to have growth and more profitability in the organization. Costing renders great assistance in measuring productivity and suggest ways to improve it.

Understand the Usefulness of Cost Accounting to Managers.

Advantages of Cost Accounting:

For better understand the Usefulness of Cost Accounting to Manager, important advantages of Cost Accounting are as follows:

Profitable and Non-profitable Activities.

It will throw light upon those activities which bring profits and those activities which result in losses. This will be done only if the cost of each product or each job ascertain and compare with the price obtained.

Support and guide in Reducing Prices.

In certain periods it becomes necessary to reduce the price even below the total cost. This will be so when there is a depression or slump. Costs, properly ascertained, will guide management in this direction.

Information for Proper Planning.

For a proper system of Costing, it is necessary to have detailed information about the facilities available about machine and labor capacity. This helps in proper planning of work so that no section overwork and no section remains idle.

Control over all Materials.

Information about the availability of stocks of various materials and stores must be constantly available if there is a good system of Cost Accounting.

This helps in two ways. Firstly, production can be planned according to the availability of materials and fresh stocks can arrange in time when old stocks are exhausted. Secondly, loss due to carelessness or pilferage or any other mischief will know and, therefore, put down.

Decision Regarding Machine or Labor.

Some of the important questions before management can solve only with the help of information about costs.

For example, if there is the problem of replacement of labor by machinery, Cost Accounting will at least guide management in finding out what the cost of production will be if either machinery or labor use.

Expansion in Production.

Sometimes it is necessary to decide whether the production of one product or the other is to increase. This problem can also be solved only if proper information about costs is available.

Reasons for Losses Detected.

Exact causes of the existence of profits or losses will reveal by a system of Cost Accounting. For example, a concern may suffer not because the cost of production is high or prices are low but because the output is much below the capacity of the concern.

It is only Cost Accounting which will reveal this reason for the loss. It also helps in distinguishing between expenditure and loss which is necessary and that which is unnecessary, that is to say, between normal and abnormal losses.

Helps in Making Decisions.

Cost Accounting inculcates the habit of making calculations with pencil and paper before taking a decision. It will certainly check recklessness. Also, some of the silly mistakes that sometimes occur can avoid if there is a good Cost Accounting system.

To give an instance, a well-known firm once quoted for the supply of mosquito nets to the Government at a very low price. It was only after the order was obtained that the firm found that, by mistake. The price of materials was not included in the quotation.

Check on Accuracy of Financial Accounts.

A good system of Cost Accounting affords an independent and most reliable check on the accuracy of financial accounts. This check operates through the reconciliation of profits shown by Cost Accounts and by Financial Accounts. Based on various advantages of Cost Accounting. It can easily say that “a good system of costing serves as a means of control over expenditure and helps to secure economy in manufacture”.

Fixation of Prices.

In many cases, a firm can fix a price for its products based on the cost of production. Such a case, the price cannot be properly fixed if no proper figures of cost are available.

In the case of big contracts, no quotation can make unless the cost of completing that contract can ascertain. If prices fixed without costing information. The price quoted may either be too high. In which case orders cannot obtain, or it may be too low, in which case order will result in a loss.

It is a mistake on the part of any management to believe that a mere increase in sales volume will result in profits; increased sales at prices lower. Then the cost may well lead the concern to the bankrupt court. Only Cost Accounting will reveal what price will be profitable.

Understand the Measurement and Improvement of Efficiency.

The chief advantage to gain is that Cost Accounting will enable a concern too. First of all, measure its efficiency and then to maintain and improve it. This is done by suitable comparisons and analysis of the differences that may observe.

For example, if materials spent upon a pair of shoes in the Year come to $ 100 and for a similar pair of the shoe, the amount is $ 120 in next Year. It is an indication of a decline in inefficiency.

Of course, the increase may only be due to an increase in the price of materials; it may also be due to greater wastage in the use of materials or inefficiency at the time of buying. So, that unnecessarily high prices were paid. Comparisons may also be made with average figures for the whole industry (if such figures are available) and with ideal figures. Which may have been determined before the head.

In any case, it is this sort of comparison which tells management about the going up or coming down of efficiency. The study will certainly indicate the steps to take to remove the causes of inefficiency or to consolidate a factor which leads to greater efficiency.

What is the Time Value of Money? If an individual behaves rationally, then he would not equate money in hand today with the same value a year from now. In fact, he would prefer to receive today than receive after one year. The time value of money or TVM is a basic financial concept that holds that money in the present is worth more than the same sum of money to be received in the future. The time value of money is the greater benefit of receiving money now rather than later. It is founded on time preference. How do you Understand the Time Value of Money in Cost of Capital?

Here is explained the Time Value of Money in Cost of Capital.

Time value of money (TVM) is the idea that money that is available at the present time is worth more than the same amount in the future, due to its potential earning capacity. This core principle of finance holds that provided money can earn interest, any amount of money is worth more the sooner it is received. The time value of money explains why interest is paid or earned: Interest, whether it is on a bank deposit or debt, compensates the depositor or lender for the time value of money. It also underlies investment. Investors are willing to forgo spending their money now only if they expect a favorable return on their investment in the future, such that the increased value to be available later is sufficiently high to offset the preference to have money now.

The reasons cited by him for preferring to have the money today include:

The uncertainty of receiving the money later.

Preference for consumption today.

Loss of investment opportunities, and.

The loss in value because of inflation.

The last two reasons are the most sensible ones for looking at the time value of money. There is a ‘risk-free rate of return’ (also called the time preference rate) which is used to compensate for the loss of not being able to invest in any other place. To this, a ‘risk premium’ is added to compensate for the uncertainty of receiving the cash flows.

The required rate of return = Risk-free rate + Risk premium

The risk-free rate compensates for the opportunity lost and the risk premium compensates for risk. It can also be called as the ‘opportunity cost of capital’ for investments of comparable risk. To calculate how the firm is going to benefit from the project we need to calculate whether the firm is earning the required rate of return or not. But the problem is that the projects would have different time frames of giving returns. One project may be giving returns in just two months, another may take two years to start yielding returns.

If both the projects are offering the same %age of returns when they start giving returns, one which gives the earnings earlier is preferred. This is a simple case and is easy to solve where both the projects require the same capital investment, but what if the projects required different investments and would give returns over a different period of time? How do we compare them? The solution is not that simple. What we do in this case is bring down the returns of both the projects to the present value and then compare.

Before we learn about present values, we have to first understand future value.

Future Value:

Future value is the amount that is obtained by enhancing the value of a present payment or a series of payments at the given rate of interest to reflect the time value of money. If we are getting a return of 10 % in one year what is the return we are going to get in two years? 20 %, right. What about the return on 10 % that you are going to get at the end of one year? If we also take that into consideration the interest that we get on this 10 % then we get a return of 10 + 1 = 11 % in the second year making for a total return of 21 %. This is the same as the compound value calculations that you must have learned earlier.

Future Value = (Investment or Present Value) * (1 + Interest) No. of time Periods

The compound values can be calculated on a yearly basis, or on a half-yearly basis, or on a monthly basis or on a continuous basis or on any other basis you may so desire. This is because the formula takes into consideration a specific time period and the interest rate for that time period only. To calculate these values would be very tedious and would require scientific calculators. To ease our jobs there are tables developed which can take care of the interest factor calculations so that our formulas can be written as:

Future Value = (Investment or Present Value) * (Future Value Interest Factor n, i)

where n = no of time periods and i = is the interest rate.

Present Value:

When a future payment or series of payments are discounted at the given rate of interest up to the present date to reflect the time value of money, the resulting value is called present value. When we solve for the present value, instead of compounding the cash flows to the future, we discount the future cash flows to the present value to match with the investments that we are making today. Bringing the values to present serves two purposes:

The comparison between the projects become easier as the values of returns of both areas of today, and.

We can compare the earnings from the future with the investment we are making today to get an idea of whether we are making any profit from the investment or not.

For calculating the present value we need two things, one, the discount rate (or the opportunity cost of capital) and two, the formula. The present value of a lump sum is just the reverse of the formula of the compound value of the lump sum:

Present Value = Feature Value/(1 + i)n

Or to use the tables the change would be:

Present Value = Future Value * (Present Value Interest Factor n, i).

where n = no of time periods and i is the interest rate.

Perpetuity:

If the annuity is expected to go on forever then it is called perpetuity and then the above formula reduces to:

Present Value= A/i

Perpetuities are not very common in financial decision making as no project is expected to last forever but there could be a few instances where the returns are expected to be for a long indeterminable period. Especially when calculating the cost of equity perpetuity concept is very useful.

For growing perpetuity, the formula changes to:

Present Value= A/i – g

All these calculations take into consideration that the cash flow is coming at the end of the period.

Present Value of Future Money Formula:

The formula can also be used to calculate the present value of money to be received in the future. You simply divide the future value rather than multiplying the present value. This can be helpful in considering two varying present and future amounts. In our original example, we considered the options of someone paying your $1,000 today versus $1,100 a year from now. If you could earn 5% on investing the money now, and wanted to know what present value would equal the future value of $1,100 – or how much money you would need in hand now in order to have $1,100 a year from now – the formula would be as follows:

PV = $1,100 / (1 + (5% / 1) ^ (1 x 1) = $1,047

The calculation above shows you that, with an available return of 5% annually, you would need to receive $1,047 in the present to equal the future value of $1,100 to be received a year from now. To make things easy for you, there are a number of online calculators to figure the future value or present value of money.

Time value of money principle also applies when comparing the worth of money to be received in future and the worth of money to be received in further future. Time value of money is the concept that the value of a dollar to be received in future is less than the value of a dollar on hand today. One reason is that money received today can be invested thus generating more money. Another reason is that when a person opts to receive a sum of money in future rather than today, he is effectively lending the money and there are risks involved in lending such as default risk and inflation.

Understand Future Cost and Historical Cost; Future cost of capital refers to the expected cost of funds to be raised to finance a project. In contrast, historical cost represents cost incurred in the past in acquiring funds. In financial decisions, future cost of capital is relatively more relevant and significant. While evaluating the viability of a project, the finance manager compares expected earnings from the project with an expected cost of funds to finance the project.

Here are explained; What is the Future and Historical Cost?

Likewise, in making financing decisions, the attempt of the finance manager is to minimize the future cost of capital and not the costs already defrayed. This does not imply that historical cost is not relevant at all. In fact, it may serve as a guideline in predicting future costs and in evaluating the past performance of the company.

Future cost: Future costs are based on forecasts. The costs relevant for most managerial decisions are forecasts of future costs or comparative conjunctions concerning future situations. An estimated quantification of the amount of a prospective expenditure. Forecasting of future costs is required for expense control, the projection of future income statements; appraisal of capital expenditures, the decision on new projects and on an expansion programme and pricing.

Historical Cost: Historical cost is an accounting method in which the assets of the firm are recorded in the books of accounts at the same value at which it was first purchased. Cost and historical cost usually mean the original cost at the time of a transaction. The historical cost method is the most widely used methods of accounting as it is easy for a firm to ascertain what price was paid for the asset.

What is Opportunity Cost? Opportunity cost analysis is an important part of a company’s decision-making processes; but, does not treat as an actual cost in any financial statement. Opportunity cost is The profit lost when one alternative selecting over another. The concept is useful simply as a reminder to examine all reasonable alternatives before making a decision. So, what discusses is – Understand the Essay on Opportunity Cost in Managerial Economics.

The Concept of Opportunity Cost is to explain the Meaning, Definition, Principles, Advantages, and Disadvantages.

While the term opportunity cost has its roots in economics, it’s also a very important concept in the investment world. It’s a model that can apply to our everyday decisions, as we face choosing between the many options we encounter each day. For example, you have $1,000,000 and choose to invest it in a product line that will generate a return of 5%. If you could have spent the money on a different investment that would have to generate a return of 7%, then the 2% difference between the two alternatives is the foregone opportunity cost of this decision.

Meaning of Opportunity Cost:

Opportunity cost cannot always fully quantify at the time when a decision-maker. Instead, the person making the decision can only roughly estimate the outcomes of various alternatives; which means imperfect knowledge can lead to an opportunity cost that will only become obvious in retrospect. This is a particular concern when there is a high variability of return. The concept of opportunity cost does not always work since it can be too difficult to make a quantitative comparison of two alternatives. It works best when there is a common unit of measure, such as money spent or time used. Opportunity cost is not an accounting concept; and so does not appear in the financial records of an entity.

It is strictly a financial analysis concept [Hindi]. Opportunity costs represent the benefits an individual, investor, or business misses out on when choosing one alternative over another. While financial reports do not show opportunity cost; business owners can use it to make educated decisions when they have multiple options before them. Because of they unsee by definition, opportunity costs can overlook if one is not careful. By understanding the potential missed opportunities one forgoes by choosing one investment over another, better decisions can make.

Definition of Opportunity Cost:

Opportunity Cost refers to the expecting returns from the second-best alternative use of resources that are foregone due to the scarcity of resources such as land, labor, capital, etc. In other words, the opportunity cost is the opportunity lost due to limited resources. It is a very powerful concept when someone has to decide to select a particular product or making a choice.

In simple words, opportunity cost means choosing or making the best decision from a different option. When one has to decide between various actions to select only one particular work at a time calls opportunity cost.

When faced with a decision, the opportunity cost the value assigned to the next best choice. The value or opportunity not chosen by the decision-maker could take many forms, including assets (as a car or home), resources (as land), or even benefits. When companies make decisions to purchase one asset over another; they’re passing up the opportunity cost offered by the asset not chosen.

The Principles of Opportunity Cost:

The opportunity cost of a decision means the sacrifice of alternatives required by that decision. The concept of opportunity cost can best understand with the help of a few illustrations, which are as follows:

The funds employed in one’s own business is equal to the interest that could earn on those funds if the employee in other ventures.

The time as an entrepreneur devotes to his own business is equal to the salary he could earn by seeking employment.

Using a machine to produce one product is equal to the earnings forgone which would have been possible from other products.

Using a machine that is useless for any other purpose is zero since its use requires no sacrifice of other opportunities.

If a machine can produce either X or Y; the opportunity cost of producing a given quantity of X is equal to the quantity of Y; which it would have to produce. If that machine can produce 10 units of X or 20 units of Y; the opportunity cost of 1 X is equal to 2 Y.

The opportunity cost of if no information provides about quantities produced; except about their prices then the opportunity cost can compute in terms of the ratio of their respective prices, say Px/Py.

Holding 100 Dollars as cash in hand for one year is equal to the 10% rate of interest; which would have been earning had the money been keeping as the fixed deposit in a bank. Thus, it is clear that opportunity costs require the ascertaining of sacrifices. If a decision involves no sacrifice; its opportunity cost is nil.

For decision-making,