Learn about Treasury bill rates and how they are determined. Discover the benefits of investing in Treasury bills, including low risk, liquidity, and competitive returns. Find out how to invest in Treasury bills and diversify your portfolio. Whether you are a seasoned investor or just starting, Treasury bills can be a valuable addition to your investment strategy.

Understanding Treasury Bill Rates

When it comes to investing, there are a multitude of options available. One such option that often considered a safe and secure investment is Treasury bills (T-bills). T-bills are short-term debt instruments issued by the government to raise funds. They considered to be one of the most low-risk investments available in the market.

What are Treasury Bills?

Treasury bills issued by the government as a way to finance its operations and pay off its debts. They are typically issued for a duration of less than one year, with maturities ranging from a few days to 52 weeks. T-bills are sold at a discount to their face value, which means that investors can buy them for less than their eventual payout.

Investing in Treasury bills is essentially lending money to the government. In return, investors receive the face value of the bill at maturity, effectively earning interest on their investment. The difference between the purchase price and the face value the interest earned.

How are Treasury Bill Rates Determined?

The interest rates on Treasury bills determined through an auction process. The U.S. Department of the Treasury conducts regular auctions to sell T-bills to investors. The interest rate, also known as the discount rate, determined by the market demand for T-bills.

Investors bid on the T-bills, specifying the discount rate they are willing to accept. The Treasury then accepts the highest bids first until it has raised the desired amount of funds. The discount rate of the last accepted bid becomes the interest rate for all T-bills sold in that auction.

The interest rate on Treasury bills influenced by various factors, including the current state of the economy, inflation rates, and the overall demand for government debt. When the economy is strong and inflation is low, Treasury bill rates tend to be lower. On the other hand, when the economy is weak or inflation is high, Treasury bill rates tend to be higher.

Why Invest in Treasury Bills?

Treasury bills considered a safe and secure investment for several reasons:

1. Low Risk:

As T-bills backed by the full faith and credit of the government, they considered to be virtually risk-free. This makes them an attractive option for conservative investors who prioritize the preservation of capital.

2. Liquidity:

Treasury bills are highly liquid investments, meaning they can easily bought and sold in the secondary market. This allows investors to access their funds quickly if needed.

3. Competitive Returns:

While Treasury bills may not offer the highest returns compared to riskier investments, they still provide competitive returns relative to other low-risk investments, such as savings accounts or certificates of deposit.

4. Diversification:

Investing in Treasury bills can help diversify a portfolio by adding a low-risk asset that is not directly correlated to the stock market. This can help reduce overall portfolio volatility.

How to Invest in Treasury Bills

Investing in Treasury bills is relatively straightforward. Here are the steps to get started:

1. Open a TreasuryDirect Account:

To invest in Treasury bills, you will need to open an account with TreasuryDirect, which is the U.S. Department of the Treasury’s online platform for buying and managing Treasury securities.

2. Fund Your Account:

Once you have opened a TreasuryDirect account, you will need to fund it by linking it to your bank account. This will allow you to transfer funds to purchase Treasury bills.

3. Place an Order:

Once your account funded, you can place an order for Treasury bills through the TreasuryDirect website. You can specify the amount you wish to invest and the duration of the T-bills you want to purchase.

4. Monitor and Manage:

After purchasing Treasury bills, you can monitor and manage them through your TreasuryDirect account. You can track their maturity dates, interest rates, and even reinvest the proceeds into new T-bills if desired.

Conclusion

Treasury bill rates play a crucial role in the investment landscape, providing investors with a safe and secure option for preserving capital and earning competitive returns. By understanding how Treasury bill rates determined and the benefits of investing in T-bills, investors can make informed decisions about their investment strategies.

While Treasury bills may not offer the highest returns, their low-risk nature and liquidity make them an attractive option for conservative investors or those looking to diversify their portfolios. By investing in Treasury bills, investors can have peace of mind knowing that their funds backed by the full faith and credit of the government.

Whether you are a seasoned investor or just starting, considering Treasury bills as part of your investment strategy can be a prudent decision. Their simplicity, low risk, and competitive returns make them a valuable addition to any investment portfolio.

Discover how to buy treasury bills and make safe and reliable investments. Learn the steps involved and make informed financial decisions.

Introduction

Are you looking for a safe and reliable investment option? Treasury bills can be a great choice. In this blog post, we will guide you through the process of buying treasury bills, from understanding what they are to the steps involved in purchasing them. Let’s dive in!

Investing in Treasury Bills: Everything You Need to Know

Treasury bills, commonly known as T-bills, are a staple for savvy investors looking for safety and reliability in their investment portfolios. Issued by the government, these short-term debt instruments backed by the full faith and credit of the issuing government, making them an extremely safe investment choice. This guide covers everything you need to know about investing in treasury bills, from what they are to how you can buy them.

What are Treasury Bills?

Treasury bills are short-term securities issued by the government to meet its short-term financial needs. They do not bear interest in the traditional sense but sold at a discount. Investors buy these bills at a discounted rate and receive the full face value upon maturity, the difference being their earnings.

Why Invest in Treasury Bills?

Safety: T-bills considered one of the safest investments because the government backs them.

Liquidity: Due to their short maturity periods, ranging from a few days to one year, they are highly liquid.

Predictable Returns: The return on T-bills known at the time of purchase, which removes market volatility concerns.

How to Buy Treasury Bills

Step 1: Verify Your Eligibility

To invest in treasury bills, typically, you need to be an individual investor, a corporation, or a financial entity. Most countries require that you meet certain criteria and have valid identity proof.

Step 2: Choose Your Investment Provider

You can purchase treasury bills directly from the government through scheduled auctions or from banks and financial institutions. Choosing the right platform based on fees, service, and accessibility is crucial.

Step 3: Open an Investment Account

If you choose to buy T-bills from a financial institution, you’ll need to open a dedicated investment account. This process involves the submission of personal information and documents for identity verification.

Step 4: Decide on the Investment Amount

There is typically a minimum amount for investing in treasury bills. Ensure you are prepared with sufficient funds to meet this requirement.

Step 5: Place Your Order

Post-funding your account, place an order specifying the amount and the desired maturity of the T-bills. This can usually be conducted online or at a bank branch.

Upon confirmation of payment, you’ll receive details of your T-bill investment. You can thereafter decide to hold them until maturity or trade them in the secondary market.

Conclusion

Investing in treasury bills is a wise decision for those looking for security and stability in their investment choices. By understanding the nature of T-bills and following these steps, you can easily incorporate them into your investment portfolio. Remember, consulting with a financial advisor can provide personalized insights tailored to your financial situation. Happy investing!

The UNCITRAL Model Law defines an arbitration agreement as; “an agreement by the parties to submit to arbitration all or certain disputes which have arisen or which may arise between them in respect of a defined legal relationship, whether contractual or not”. This means that parties agree to settle their disputes in the arbitration process instead of public litigation. Parties can choose which kind of disputes fall under arbitration. It can mean that all disputes arising out of their legal relationship are to exist settled in the arbitration process, or on the other hand, parties can choose that only certain kinds of them fall under it. Also, as the wording of the definition states, they can draft before or after the dispute has arisen.

Here is the article to explain, How to define Arbitration Agreement?

They also define the scope of the arbitral tribunal’s jurisdiction. The arbitral tribunal does not have jurisdiction over matters which does not cover by they made by the parties. In other words, if the parties have agreed to settle certain kinds of disputes in the arbitration, the tribunal has no jurisdiction over other matters.

There are two types of arbitration agreements: “separate” arbitration agreements and arbitration clauses. Separate arbitration agreements are those which constitute a whole new deal, where parties agree to settle their dispute in arbitration. An arbitration clause means a provision, included in the contract between parties, which contains an obligation to settle disputes in arbitration.

National arbitration laws can set out different requirements for the form of the arbitration contract. The main rule is that they must be in writing. However, the requirement is pretty loose, because the requirement can exist fulfilled by the exchange of letters or telegrams, or in an otherwise documented way.

The seat of Arbitration;

The concept of the seat of arbitration determines the procedural rules of the arbitration proceedings. It refers to the geographical and legal jurisdiction to which the arbitration process stands tied. In other words, it is the place where the arbitration exists held. For example, the arbitration agreement can state that the proceedings are to exist held “in London under the rules of the ICC”. Parties are free to identify the seat of arbitration. If they fail to do so, the seat stands implied from an express choice of law governing the procedure. For example, if the arbitration contract states that the dispute exists settled following Indian law, the seat considers to be in India.

Meaning of Arbitration;

Have you ever owned a cellular telephone or credit card? If so, the percentages are when you signed an arbitration settlement. You additionally would possibly have signed a settlement while you started your present-day process. Or, when you started yours beyond task. Many human beings sign agreements without even knowing it. So, why do employers and corporations prefer to have people sign arbitration agreements? It comes down to decreasing the fees of capability litigation. Plus, groups want to make the dispute resolution manner green. (Oftentimes, court litigation isn’t efficient.) That’s why they ask such a lot of employees and customers to sign agreements. Arbitration clauses frequently appear as the fine print in lots of fashionable contracts. This leads to someone after individual signing an agreement without even figuring out it. Let’s now assess the meaning of a deal with the aid of going over compelled arbitration basics.

What is the Objective of an Arbitration Agreement?

An arbitration settlement is a device to limit litigation fees, test also Arbitration prices. But that’s not the simplest motive of a settlement. It additionally guarantees that disputes continue to be private. Keep in thoughts that signing an arbitration settlement forfeits certain. Rights. Before signing, it’s fine to evaluate each arbitration clause. You can renegotiate (or reject) any time that you dislike. Learn greater to understand the concept of Arbitration vs Litigation.

The Benefits of an Arbitration Agreement for Any Business or Employer;

Understanding the advantages of arbitration is prime to recognizing settlement blessings. Interest Arbitration is sort of always less expensive in comparison to filing complaints. Plus, the procedure goes faster and is way greater confidential. US courts regularly refuse to overturn the decisions of arbitration. Courts will step in to make certain arbitration awards get enforced. The arbitration system results in a final, binding outcome. In this manner, events can pass ahead inside months. Plus, they get to avoid the public scrutiny that a court trial creates. This can boost the results of any business imparting employment.

The law governing the arbitration agreement;

Let’s bounce right in and verify the which means of the common arbitration settlement. An arbitration agreement often features as a clause in a broader settlement. Through the agreement, events will settle their dispute out of the court docket. This applies to all varieties of legal disagreements that arise with any other party. You can find arbitration agreements in maximum consumer contracts. They’re also present in many employment contracts. They additionally often get blanketed in proposed additions for the duration of settlement negotiation. That’s whilst as a minimum one birthday party seeks to keep away from a future lawsuit taking vicinity.

The following arbitration agreement law governing below are;

The Governing Law;

The law governing they can be truly different if the parties choose to conclude a separate arbitration contract instead of the arbitration clause included in the substantive contract. In the case of separate arbitration agreements, parties are free to choose the law governing them.

This can lead to a situation where the proper law of the arbitration agreement can be different from the law governing the dispute because they and the contract from which the dispute arises are separate entities and are governed by different laws. But on the other hand, in the case of arbitration clauses, finding the governing law can be a bit more difficult. Firstly, the proper law of they will normally be the law applicable to the substantive contract as a whole.

So if the contract contains an express choice of law made by parties, the chosen law also governs the arbitration clause. Secondly, in the case where the parties have failed to express their choice of law, the law governing the contract exists normally implied from the seat of arbitration. And thirdly, if parties have failed to express their choice of law and they have not designated the seat of arbitration, the proper law of the arbitration clause is the law of the country with which it stands most closely connected.

Refusal of the Recognition of the Arbitration Agreement;

The national court can refuse their recognition of them if under the law of the country the dispute is not capable of settlement by arbitration. Usually, these types of issues are related to status and family law matters, and of course, criminal law matters, in which the parties have restricted ability to agree on the matters. In some countries, also consumers exist protected by setting additional requirements for the arbitration agreements.

Validity of the Arbitration Agreement;

The validity of the arbitration agreement stands considered under the choice of law governing them. But if there is no choice of law created by the parties, the validity of the arbitration contract consider based on the law of the country in which the award is to make. In some cases, it can be hard to say in which country the award is to exist made. In these cases, where there is no choice of law and the country in which the award will make cannot yet determine, the validity considers following the law of the country in which the court is considering the validity.

What is the Law of Equity? Maxims, Equitable Remedies, and its Essay; The law of equity began in the court of chancery which stood set up because a fair and just remedy could not give through common law as monetary compensation was not suitable; and, sometimes a well-deserving plaintiff was denied because the writs were quite narrow and rigid. Courts stood guided by the previous decisions and that’s how the twelve maxims existed formulated.

Here is the article to explain, What is the Law of Equity? also define the Maxims, Equitable Remedies, and its Essay!

These maxims limit the granting of equitable remedies for those who have not acted equitably. The decisions of the court of chancery and common law were constantly conflicting. This rivalry existed ended in The Earl of Oxford’s case 1615. In which the king stated ‘Where common law and equity conflict equity should prevail’. The two courts are now unified and the same judges give decisions out common law and equity.

Introduction to Equity Law;

“Equity is Not Past the Age of Childbearing”. The law relating to equity is largely built on precedent. The rules have stood built upon by previous situations which they have dealt with. Although there has been a lot of disagreement about changing laws and adding to the law of equity; the rules that have stood accepted by proceeding judges became precedent and stand now known as maxims and used as guidelines by the court. I agree with the statement by Denning as equity is born from the interpretation of judges and their problem-solving abilities.

There are a lot of different rules regarding equity that have all existed created through precedent. It is my opinion that although Equity dates back hundreds of years and the law is still just as relevant. There are alterations to the law as recent as the 1975 Eves V Eves case. I think that as long as there are judges to create precedent there can be new law created in equity.

The Maxims of Equity;

These are the general legal principles that have stood adopted through threw following precedent regarding equity. These maxims are the body of law that has developed about equity and this helps to govern the way equity operates. All maxims are discretionary and courts may choose whether they wish to apply these principles.

Equity will not suffer a wrong to be without a remedy:

This maxim developed as common law had no new remedies only monetary damages. Maxim must treat with caution as today’s laws stand made by the Oireachtas. Maxim can use by the beneficiary of a trust whose rights existed not recognized by the common law. Equitable remedies such as injunctions or specific performance may give. Attempts to alter this maxim in recent times by Lord Denning were unsuccessful.

Equity follows the law:

Courts will firstly apply common law and if this is not fair then an equitable remedy will be provided. This maxim sets out that equity is not in place to overrule judgments in common law but rather to make sure that parties don’t suffer injustice.

He who seeks equity must do equity:

A remedy will only be provided where you have acted equitably in the transaction. This maxim is discretionary and is concerned with the future conduct of the plaintiff.

He who comes to equity must come with clean hands:

This maxim link to the previous maxim and relates to the past conduct of parties. They must not have had any involvement in fraud or misrepresentation or they will not succeed in equity. A beneficiary failed in their action against the trustees to pay her back the assets of the trust she had already received as a result of a misrepresentation of her age.

Delay defeats equity:

Laches is an unreasonable delay in enforcing a right. If there is an unreasonable delay in bringing proceedings the case may exist disallowed in equity. Acquiescence is where one party breaches another’s rights and that party doesn’t take any action against them they may do not allowed to pursue this claim at a later stage. These may exist used as defenses about equity cases.

For a defense of laches, courts must decide whether the plaintiff has delayed unreasonably in bringing forth their claim and the defense of acquiescence can use; if the actions of the defendant suggest that they are not going ahead with the claim; so it is reasonable for the other party to assume that there is no claim.

Equality is Equity:

Where more than one person exists involved in owning a property the courts prefer to divide property equally. Prefer to treat all involved as equals. In the case of a business, any funds leftover from dissolution should stand divided equally.

Equity looks to the intent rather than the form:

The principle established in. This maxim is where the equitable remedy for rectification stood established this allows for a contract to correct when the terms do not correctly record. This maxim allows the judge to interpret the intentions of the parties if the terms don’t record properly.

Equity looks on that as done which ought to have been done:

The judges look at this contract from the enforceable side and the situation they would be in had the contract stood completed.

Equity imputes an intention to fulfill an Obligation:

If a person completes an act that could exist regarded as fulfilling an original obligation it will take as such.

Equity acts in personam:

This maxim states that equity relates to a person rather than their property. It applies to property outside a jurisdiction provided that a defendant is within the jurisdiction. English court ordered specific performance on land in the US.

Where the equities are equal, the first in time prevails:

Equity law, Where two parties have the right to possess an object the first one with the interest will prevail.

Where the equities are equal, the law prevails:

Where two parties want the same thing and the court can’t honestly decide who deserves it most they will leave it where it is

Equitable Remedies;

The following Equitable Remedies below are;

Injunction;

This is an order by the court to make a party complete an action or to make them refrain from doing an action. It exists awarded to protect a legal right rather than compensate for the breach of one. If a party breaches this court order it is a serious offense and can merit arrest or possible jail sentence. The reason for injunctions is that money would be an inadequate remedy for breaching the person’s right.

An injunction is a discretionary remedy that courts will only grant if they feel it is just and equitable in the circumstances to do so. Interim and interlocutory injunctions are temporary and last up until a specified date or until a trial hearing. Injunctions can exist used to stop trespass, pass off, prevent illegal picketing, and freeze assets. The conduct of the parties will also affect whether the judge will grant them an injunction.

Interlocutory Injunction;

Granted before a court hearing because the plaintiff may suffer unrepairable damage if the right exists breached which cannot exist compensated by money. The plaintiff must prove to the judge that there is sufficient reason to believe that the damage will exist caused to them.

Three-stage test on granting interlocutory injunctions existedintroduced in the English case (American Cyanamid) this stoodaccepted and followed as law in the Irish case:

If it is a serious and fair issue that will tried you need not prove it’ll be a successful claim.

Set out if damages would be a suitable remedy. It must be impossible to quantify damages and must give an undertaking which means in the event of an injunction not being granted they must compensate the other party for any losses.

Whether it is convenient or not to grant the injunction. The need for the plaintiff to protected must outweigh the right of the other party to grant the injunction.

Qui Timet Injunction;

Prevents an act before it has stood committed it may fear or could have existed threatened. The plaintiff must show that there is a strong possibility of this happening and the consequences of the act will be extremely damaging. The burden of proof is higher than a normal injunction.

Mareva Injunction;

This type of injunction can also stand known as a freezing injunction. Where one feels that they have a substantial case against the other they can apply to the courts for this only if they feel that the other may move of hiding assets. To gain this type of injunction plaintiffs must prove that they have a substantial case and must also prove that the assets are at risk. It must also be convenient to grant it.

This type of injunction stood introduced in the Nippon Case 1975 by Lord Denning where the defendant owed money to the plaintiff he existed not allowed to take out the amount he had owed from his account. This became another instrument of law when it stood confirmed in the Mareva Case.

Anton Piller Order;

This can also be known as a search order. It was thought of to prevent the defendant from destroying anything that could exist used by the plaintiff in court to assist their trial. It is granted without the other party’s knowledge to maintain the element of surprise. The order requires the defendant to allow the plaintiff or a representative to enter his premises and to collect what is relevant for evidence.

If the defendant does not follow the order then he shall be held in contempt of court. It is only granted where it is deemed to be necessary where it is feared that vital evidence will be destroyed. The order takes its name from the 1976 Anton Piller KG v Manufacturing Processes Ltd case

Specific Performance;

Is a form of injunction where a court orders an individual to complete a specific task which is generally part of a contract. This remedy is discretionary and only used when an individual cannot exist compensated by money. If they do not complete the contract they will exist held in contempt of court.

Rescission;

This remedy aims to return parties to the position they were in before they entered into the contract. The main grounds for rescission are mistake, misrepresentation, undue influence, and unconscionable transactions.

Law of Equity Essay Maxims Equitable Remedies; Image by Free-Photos from Pixabay.

What does the Stock Market Index mean? Stock Index futures offer the investor a medium for expressing an opinion on the general course of the market. The general movement of the stock market is usually measured by averages or indices consisting of groups of securities that are supposed to represent the entire stock market or its particular segments. Thus, Security Market Indices or Security Market Indicators provide a summary measure of the behavior of security prices and the stock market. So, what is the topic we are going to discuss: Purpose and Limitations of Stock Market Index!

Explained Stock Market Index Concept with their Purpose and Limitations!

The principal stock market indices used in India are the Bombay Stock Exchange Sensitive Index (BSE Sensex) and the S&P CNX Nifty known as the NSE Nifty (National Stock Exchange Fifty). In addition, these contracts can be used by portfolio managers in a variety of ways to alter the risk-return distribution of their stock portfolios. For instance, much of a sudden upward surge in the market could be missed by the institutional investor due to the time it takes to get money into the stock market.

Stock Index Futures:

By purchasing stock- index contracts, the institutional investors can enter the market immediately and then gradually unwind the long futures position as they are able to get more funds invested the stock. Conversely, after a run-up in the value of the stock portfolio (assuming it is well diversified and correlates well with one of the major indexes) a portfolio manager might desire to lock in the profits much after being required to report this quarterly return on the portfolio.

By selling an appropriate number of stock index futures contracts, the institutional investors could offset any losses on the stock portfolio with corresponding gains on future position. As a speculation tool, stock index futures represent an inexpensive and highly liquid short-run alternative to speculating on the stock market.

Instead of purchasing the stock that makes up an index or proxy portfolio, a bullish (bearish) speculation can take a long (short) position in an index futures contract, then purchase treasury securities to satisfy the major requirements. A long or short speculative futures position is referred to as a purely speculative position or a naked (outright) position.

The Purpose of an Index in the Stock Market:

The security market indices are indicators of different things and are useful for different purposes.

The following are the important uses of a stock market index:

Security market indices are the basic tools to help and analyze the movements of prices of various stocks listed on stock exchanges and are useful indicators of a country’s economic health.

Indices can be calculated industry-wise to know their tread pattern and also for comparative purposes across the industries and with the market indices.

The growth in the secondary market can be measured through the movement of indices.

The stock market index can be used to compare a given share price behavior with past movements.

Generally, stock market indices are designed to serve as indicators of broad movements in the securities market and as sensitive barometers of the changes in trading patterns in the stock market.

The investors can make their investment decisions accordingly by estimating the realized rate of return on the stock market index between two dates.

Funds can be allocated more rationally between stocks with knowledge of the relationship of prices of individual stocks with the movements in the market.

The return on the stock market index, which is known as the market return, is helpful in evaluating the portfolio risk-return analysis. According to modern portfolio theory’s capital asset pricing model, the return on a stock depends on whether the stock’s price follows prices in the market as a whole; the more closely the stock follows the market, the greater will be its expected return.

Purpose and Limitations of Stock Market Index, Image credit from #Pixabay.

Limitations of Stock Market Index (Indices):

Though stock market indices are the basic tools to help and analyze the movements of the price of the stock markets and are a useful indicator of a country’s economic health, they have their own limitations also.

The following points deal with those limitations:

Whenever a company issues rights in the form of convertible debentures (to be converted at a later stage) or other instruments (warrants) entitling the holder to acquire one equity share of the company at a specified price at a notified future date, the equity capital increases only on conversion of debentures or the exercise of warrants/Secured Premium Notes (SPNs), option for equity shares but the market adjusts the ex-rights price of the share immediately (on the day the share starts trading ex-rights) on the basis of the anticipated increase in equity capital and likely reduced earnings per share, etc.

Hence, some modification is needed to adjust the equity capital suitably in advance. But the exact procedure by which this can be done is very difficult to state since the internal market mechanism which adjusts the ex-rights share price is almost impossible to know precisely.

Again, this is a common limitation of all the indices and so far, the increased equity capital is considered only after the debentures are converted into shares and are acquired for warrants/SPNs and the new shares are listed for trading on the stock exchange.

The coverage (in terms of number of scrips, number of stock exchanges used and the respective weights assigned) is different for all the indices and hence, each index may give only a partial picture of the movement of prices or the state of the market presented may be misleading.

The financial institutions sometimes convert the loans extended by them to companies into equity shares at a specified date. This causes sudden and significant changes in the market capitalization and hence the weights assigned to those scrips change violently.

The various stock market indicators around the world have been in use for many years and it has satisfied the needs of millions of investors and stockbrokers. But the stock markets, by their very nature, are very dynamic and hence, the indices should be revised or adjusted periodically to reflect the changed conditions so that they continue to be relevant.

Whenever prices of scripts listed on more than one stock exchange are used, most liquid prices (on anyone stock exchange) should be used (rather than the present practice of using the arithmetic average of prices on all the exchanges, as the same script may not enjoy the identical degree of liquidity on all exchanges).

The limitations indicated may not be eliminated totally, but appropriate adjustments are certainly called for. The classification of industries into various groups for calculation of various industry indices is presently rather vague and presents problems in the case of diversified companies. Also learned, What does Welfare Economics mean? Measuring and Value decisions!

This should be made uniform or the classification should be made in such a way that it reflects the major operations carried on by each company. Overall, one can say that the various stock market indicators devised have more or less served their purpose, despite their limitations but these can be made more effective and dynamic by introducing appropriate modifications 0£ the existing ones to serve the investing public better.

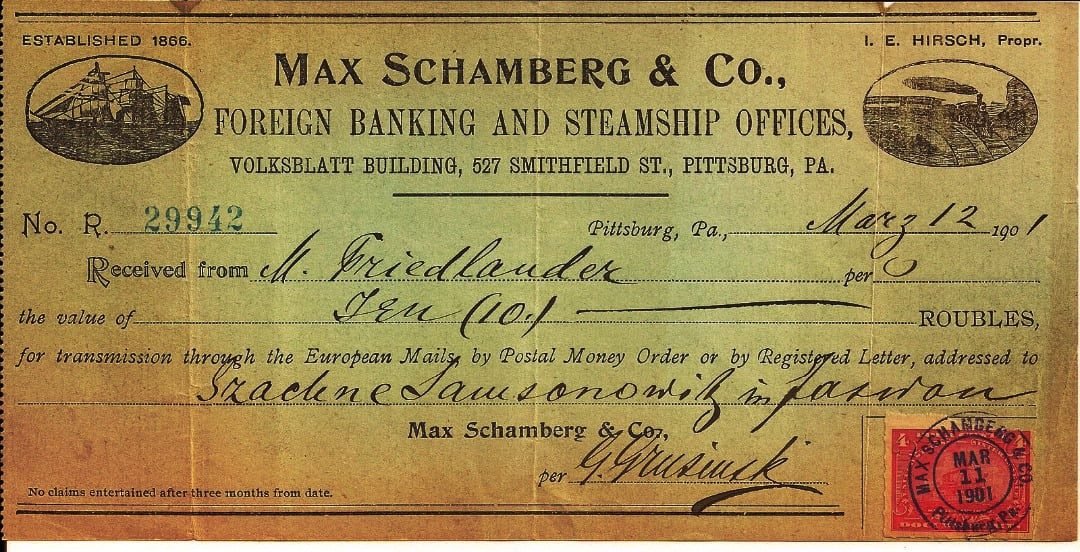

Meaning of Negotiable Instrument: A negotiable instrument is a specialized type of “contract” for the payment of money that is unconditional and capable of transfer by negotiation. The Concept of the study Explains – Negotiable Instruments: Types of Negotiable Instruments, Classification of Negotiable Instruments, Importance of Negotiable Instruments. Common examples include cheques, banknotes (paper money), and commercial paper. Also learned, Negotiable Instruments: Types, Classification, Importance!

Explain and Learn, Negotiable Instruments: Types, Classification, Importance!

A promissory note: is a Written promise by the maker to pay money to the payee. the most common type of promissory note is a bank note, Which is defined as a promissory note made by a bank and payable to bearer on demand. Through promissory note a person i.e. maker (drawer) promise to pay the payee a specific amount on a specified date Without any condition. “o the important points in a promissory note are 1) it is unconditional order 2) a specific amount 3) payable to the order of a person or on demand.

A bill of exchange: is a Written order by the drawer to the drawee to pay money to the payee. The most common type of bill of exchange is the cheque, which is defined as a bill of exchange drawn on a banker and payable on demand. &ills of exchange are used primarily in international trade and are written orders by one person to his bank to pay the bearer a specific sum on a specific date sometime in the future.

A cheque: is an unconditional order in writing drawn upon a specified banker signed by the drawer, directing to the banker to pay on demand a certain sum of money to or to the order of a person named therein or to the bearer.

#Types of Negotiable Instruments:

Parties to various types of Negotiable Instruments:

Drawer or Drawee:

The maker of a bill of exchange or cheque is called the “drawer”; the person thereby directed to pay is called the “Drawee”.

Drawee in case of need:

When in the bill or in any endorsement thereon the name of any person is given in addition to the Drawee to be resorted to in case of need such person is called a “drawee in case of need”.

Acceptor:

After the drawee of a bill has signed his assent upon the bill, or, if there are more parts thereof than one, upon one of such parts, and delivered the same, or given notice of such signing to the holder or to some person on this behalf, he is called the “acceptor”.

The acceptor for the honor:

When a bill of exchange has been noted or protested for non-acceptance or for better security, and any person accepts is supra protest for the honor of the drawer or of any one of the endorsers, such person is called an “acceptor for honor”.

Payee:

The person named in the instrument, to whom or to whose order the money is by the instrument directed to be paid, is called the “payee”.

Holder:

The “holder” of a promissory note, bill of exchange or cheque means any person entitled in his own name to the possession thereof and to receive or recover the amount due thereon from the parties thereto. Where the note, bill or cheque is lost or destroyed, its holder is the person so entitled at the time of such loss or destruction.

Holder in due course:

“Holder in due course” means any person who for consideration became the possessor of a promissory note, bill of exchange or cheque if payable to bearer, or the payee or endorse thereof, if (payable to order) before the amount mentioned in it became payable, and without having sufficient cause to believe that any defect existed in the title of the person from whom he derived his title.

Endorsement:

When the marker or holder of a negotiable instrument signs the same, otherwise than as such maker, for the purpose of negotiation, one the back or face thereof or on a slip of paper annexed thereto, or so signs for the same purpose a stamped paper intended to be completed as a negotiable instrument, he is said to endorse the same, and is called the “endorser”.

Capacity to make, etc., promissory notes, etc.: Every person capable of contracting, according to the law to which he is subject, may bind himself and be bound by the making, drawing, acceptance, endorsement, delivery and negotiation of a promissory note, bill of exchange or cheque.

Minor:

A minor may draw, endorse, deliver and negotiate such instruments so as to bind all parties except himself. Nothing herein contained shall be deemed to empower a corporation to make, endorse or accept such instruments except in cases in which, under the law for the time being in force, they are so empowered.

Agency:

Every person capable of binding himself or of being bound, as mentioned in section 26, may so bind himself or be bound by a duly authorized agent acting in his name. A general authority to transact business and to receive and discharge debts does not confer upon an agent the power of accepting or endorsing bills of exchange so as to bind his principal.

#Classification of Negotiable Instruments:

The Following Classification of Negotiable Instruments are:

Inland Instrument:

A promissory note, bill of exchange or cheque which is 1) both drawn or made in India and made payable in India, or 2) drawn upon any person resident in India, is deemed to be an inland instrument. A bill of exchange drawn upon a resident in India is an inland bill irrespective of the place where it was drawn.

Foreign Instrument:

An instrument, which is not an inland instrument, is deemed to be a foreign instrument. Foreign bills must be protested for dishonor if such protest is required by the law of the place where they are drawn. But protest in case of inland bills is optional.

Instruments payable on demand:

A cheque is always payable on demand and it cannot be expressed to be payable otherwise than on demand. A promissory note or bill of exchange is payable on demand:

When no time for payment is specified in it.

When it is expressed to be payable ‘on demand’, or ‘at sight’ or ‘on presentment’. The words ‘on demand’ is usually in a promissory note, the words ‘at sight’ are in a bill of exchange.

Ambiguous Instrument:

When an instrument owing to its faulty drafting may be interpreted either as a promissory note or a bill of exchange, it is called an ambiguous instrument. Its holder has to elect once for all whether he wants to treat it an as a promissory note or a bill of exchange. Once he does so he must abide by his election.

Forged Instrument:

An instrument is a forged when it is drawn, made or alternated in writing to prejudice another man’s rights. The most common form of forgery is signing another person’s signature, signing the name of the fictitious or none existing person. Fraudulently writing the name of an existing person is also the forgery.

Forgery is a nullity and, therefore, it passes no title. No holder of a forged instrument acquires any right on the instruments. Even a holder in due course gets no title if he comes into the possession of a forged instrument. A person has to pay money on a forged instrument by mistake, can recover it from the person to whom he has paid for it.

Bearer And Order Instruments:

An instrument is a bearer instrument when the amount payable thereon is payable to the bearer and him as a holder and in lawful possession, thereof is entitled to enforce payment due on it.

Negotiable Instrument is a certain type of document, which transfers the money. It makes easy to carry money from one place to another place. So, it is very important for the transfer of money in the business sector.

The following points can grasp as the importance of a Negotiable Instrument.

Negotiable Instrument is an easier means of transfer of money.

It is easy to delivery from one place to another place.

It helps to flourish in the business sector.

It creates the right of property.

It has the easy negotiability and somewhere it provides the security.

It makes the fast transaction of money.

It makes the security of money as well as personal security in course of the transaction of money.

Negotiable Instrument is an easier way to transfer money from one place to another place. It provides a safe way to deliver the money. It has an important role to develop the way of money transaction as well as the business realm.

A Promissory Note is an instrument in writing, except government note or bank currency, containing unconditional undertaking signed by the Maker to pay a certain sum of money only to, or to the order of or to the bearer or to a certain person related to the instrument. Section 2(f) of Negotiable Instrument Act, 2034 The person, who makes the promissory note or promises, is called a ‘Maker’ and he has to sign that document as a debtor.

The person to whom payment is to be made is called the ‘payee’. A promissory note is an unconditional promise to pay put into writing by a person or entity and signed by the borrower or person making the promise. Promissory notes are often created between a borrower and a lender in which the borrower promises to pay the lender a specific amount of money by the specified date.

A promissory note, similar to a contract, contains all of the details pertaining to the transaction such as the amount borrowed, late fees, interest rates, and so forth, and should contain the term “promissory note” within the body. In terms of enforceability, a promissory note lies somewhere between an informal IOU and a formal loan contract.

Bill of exchange is another type of Negotiable Instrument. It is also in practice in the business sector. A bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument.

It is defined under section 2(g) of the Nepalese Negotiable Instrument Act, 2034. Section 2(g) defines as “A bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money to, or to the order of a person or to a person or to the bearer of the instrument”.

On the basis of the above definition, there are three parties in the bill of exchange, which are as below:

Drawer: The maker of a bill of exchange.

Drawee: The person, who is directed to pay.

Payee: The person who receives the bill of exchange.

Another commonly used type of negotiable instrument is the bill of exchange. A bill of exchange is a financial document that states an individual or business will pay a certain amount on a specific date. The date may range from the date it is signed, to within six months into the future.

A bill of exchange must contain the signature of the individual promising to pay to be considered legally binding. Unlike a promissory note, a bill of exchange may be transferred to a third party, binding the payor to pay the third party who was not involved in the first place.

The cheque is a very common form of negotiable instrument. If you have a savings bank account or current account in a bank, you can issue a cheque in your own name or in favor of others, thereby directing the bank to pay the specified amount to the person named in the cheque. Therefore, a cheque may be regarded as a bill of exchange; the only difference is that the bank is always the drawee in case of a cheque.

The Negotiable Instruments Act, 1881 defines a cheque as a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand. From the above dentition, it appears that a cheque is an instrument in writing, containing an unconditional order, signed by the maker, directing a specified banker to pay, on demand, a certain sum of money only to, to the order of, a certain person or to the bearer of the instrument.

The person who draws a cheque is called the “Drawer”. The banker on whom it is drawn is the “Drawee” and the person in whose favor it is drawn is the “payee”. Actually, a cheque is an order by the account holder of the bank directing his banker to pay on demand, the specified amount, to or to the order of the person named therein or to the bearer.

A Negotiable Instrument is a document guaranteeing the payment of a specific amount of money, either on demand or at a set time, with the payer usually named on the document. The Concept of the study Explains – Negotiable Instruments: Meaning, Definition of Negotiable Instruments, Characteristics of Negotiable Instruments, and Features of Negotiable Instruments. More specifically, it is a document contemplated by or consisting of a contract, which promises the payment of money without condition, which may be paid either on demand or at a future date. The term can have different meanings, depending on what law is being applied and what country and context it is used in. Also learned, Commercial Bills, Negotiable Instruments: Definition, Characteristics, and Features! Read and share the given article in Hindi.

Explain and Learn, Negotiable Instruments: Definition, Characteristics, and Features!

Negotiable Instruments Act: The law relating to “Negotiable Instruments” is contained in the Negotiable Instruments Act, 1881, as amended up-to-date. It deals with three kinds of negotiable instruments, i.e., Promissory Notes, Bills of Exchange and Cherubs. The provisions of the Act also apply to “hands” (an instrument in oriental language), unless there is a local usage to the contrary.

Other documents like treasury bills, dividend warrants, share warrants, bearer debentures, port trust or improvement trust debentures, railway bonds payable to bearer etc., are also recognized as negotiable instruments either by mercantile custom or under other enactments like the Companies Act, and therefore, Negotiable Instruments Act is applicable to them.

#Definition of Negotiable Instruments:

The word “Negotiable” means “Transferable by delivery”, and the word “Instrument” means “A written document by which a right is created in favor of some person”. Thus, the term “Negotiable instrument” literally means “a written document transferable by delivery”.

According to Section 13 of the Negotiable Instruments Act,

“A negotiable instrument means a promissory note, bill of exchange or cheque payable either to order or to bearer.”

The Act, thus, mentions three kinds of negotiable instruments, namely notes, bills and cherubs and declares that to be negotiable they must be made payable in any of the following forms:

A) Payable to order:

A note, bill or cheque is payable to order which is expressed to be “payable to a particular person or his order”.

But it should not contain any words prohibiting the transfer, e.g., “Pay to A only” or “Pay to A and none else” is not treated as “payable to order” and therefore such a document shall not be treated as the negotiable instrument because its negotiability has been restricted.

There is, however, an exception in favor of a cherub. A cheque crossed “Account Payee only” can still be negotiated further; of course, the banker is to take extra care in that case.

B) Payable to bearer:

“Payable to bearer” means “payable to any person whom so ever bears it.” A note, bill or cheque is payable to bearer which is expressed to be so payable or on which the only or last endorsement is an endorsement in blank.

The definition given in Section 13 of the Negotiable Instruments Act does not set out the essential characteristics of a negotiable instrument. Possibly the most expressive and all-encompassing definition of negotiable instrument had been suggested by Thomas who is as follows:

“A negotiable instrument is one which is, by a legally recognized custom of trade or by law, transferable by delivery or by endorsement and delivery in such circumstances that (a) the holder of it for the time being may sue on it in his own name and (b) the property in it passes, free from equities, to a bonfire transferee for value, notwithstanding any defect in the title of the transferor.”

#Characteristics of Negotiable Instruments:

An examination of the above definition reveals the following essential characteristics of negotiable instruments which make them different from an ordinary chattel:

Easy negotiability:

They are transferable from one person to another without any formality. In other words, the property (right of ownership) in these instruments passes by either endorsement or delivery (in case it is payable to order) or by delivery merely (in case it is payable to bearer), and no further evidence of transfer is needed.

The transferee can sue in his own name without giving notice to the debtor:

A bill, note or a cheque represents a debt, i.e., an “actionable claim” and implies the right of the creditor to recover something from his debtor. The creditor can either recover this amount himself or can transfer his right to another person. In case he transfers his right, the transferee of a negotiable instrument is entitled to sue on the instrument in his own name in case of dishonor, without giving notice to the debtor of the fact that he has become the holder.

The better title to a bonfire transferee for value:

A bonfire transferee off a negotiable instrument for value (technically called a holder in due course) gets the instrument “free from all defects.” He is not affected by any defect of title of the transferor or any prior party. Thus, the general rule of the law of transfer applicable in the case of ordinary chattels that “nobody can transfer a better title than that of his own” does not apply to negotiable instruments.

Examples of Negotiable Instruments:

The following instruments have been recognized as negotiable instruments by statute or by usage or custom:

Bills of exchange;

Promissory notes;

Cheques;

Government promissory notes;

Treasury bills;

Dividend warrants;

Share warrants;

Bearer debentures;

Port Trust or Improvement Trust debentures;

Hindus, and;

Railway bonds payable to bearer, etc.

Examples of Non-negotiable Instruments:

These are:

Money orders;

Postal orders;

Fixed deposit receipts;

Share certificates, and;

Letters of credit.

Endorsement:

Section 15 defines endorsement as follows: “When the maker or holder of a negotiable instrument signs the same, otherwise than as such maker, for the purpose of negotiation, on the back or face thereof or on a slip of paper annexed thereto, or so signs for the same purpose a stamped paper intended to be completed as negotiable instrument, he is said to endorse the same, and is called the endorser.”

Thus, an endorsement consists of the signature of the holder usually made on the back of the negotiable instrument with the object of transferring the instrument. If no space is left on the back of the instrument for the purpose of endorsement, further endorsements are signed on a slip of paper attached to the instrument. Such a slip is called “along” and becomes part of the instrument. The person making the endorsement is called an “endorser” and the person to whom the instrument is endorsed is called an “endorse.”

Kinds of Endorsements:

Endorsements may be of the following kinds:

Blank or general endorsement: If the endorser signs his name only and does not specify the name of the indorse, the endorsement is said to be in blank. The effect of a blank endorsement is to convert the order instrument into a bearer instrument which may be transferred merely by delivery.

Endorsement in full or special endorsement: If the endorser, in addition to his signature, also adds a direction to pay the amount mentioned in the instrument to, or to the order of, a specified person, the endorsement is said to be in full.

Partial endorsement: Section 56 provides that a negotiable instrument cannot be endorsed for a part of the amount appearing to be due on the instrument. In other words, a partial endorsement which transfers the right to receive only a partial payment of the amount due on the instrument is invalid.

Restrictive endorsement: An endorsement which, by express words, prohibits the indorse from further negotiating the instrument or restricts the indorse to deal with the instrument as directed by the endorser is called “restrictive” endorsement. The indorse under a restrictive endorsement gets all the rights of an endorser except the right of further negotiation.

Conditional endorsement: If the endorser of a negotiable instrument, by express words in the endorsement, makes his liability, dependent on the happening of a specified event, although such event may never happen, such endorsement is called a “conditional” endorsement.

In the case of a conditional endorsement, the liability of the endorser would arise only upon the happening of the event specified. But they endorse can sue other prior parties, e.g., the maker, acceptor etc. if the instrument is not duly met at maturity, even though the specified event did not happen.

Negotiable Instruments: Definition, Characteristics, and Features!

#Features of Negotiable Instruments:

Negotiable Instrument, in law, a written contract or another instrument whose benefit can be passed on from the original holder to new holders. The original holder (the transferor) must countersign the instrument (as in the case of a cheque) or merely deliver it (as in the case of a bank note) to the new holder; the new holder is then entitled to the benefit of the instrument (in the case of a cheque, to the money from the bank; in the case of the banknote, to the sum promised on the note).

According to section 13 of the Negotiable Instruments Act, 1881, a negotiable instrument means,

“Promissory note, bill of exchange, or cheque, payable either to order or to bearer.”

Major features of negotiable instruments are:

The following features below are:

Easy Transferability:

A negotiable instrument is freely transferable. Usually, when we transfer any property to somebody, we are required to make a transfer deed, get it registered, pay stamp duty, etc. But, such formalities are not required while transferring a negotiable instrument.

The ownership is changed by mere delivery (when payable to the bearer) or by valid endorsement and delivery (when payable to order). Further, while transferring it is also not required to give notice to the previous holder.

Title:

Negotiability confers an absolute and good title on the transferee. It means that a person who receives a negotiable instrument has a clear and indisputable title to the instrument.

However, the title of the receiver will be absolute, only if he has got the instrument in good faith and for consideration.

Also, the receiver should have no knowledge of the previous holder having any defect in his title. Such a person is known as the holder in due course.

Must be in writing:

A negotiable instrument must be in writing. This includes handwriting, typing, computer print out and engraving, etc.

Unconditional Order:

In every negotiable instrument, there must be an unconditional order or promise for payment.

Payment:

The instrument must involve the payment of a certain sum of money only and nothing else.

For example, one cannot make a promissory note on assets, securities, or goods.

The time of payment must be certain:

It means that the instrument must be payable at a time which is certain to arrive. If the time is mentioned as “when convenient” it is not a negotiable instrument.

However, if the time of payment is linked to the death of a person, it is nevertheless a negotiable instrument as death is certain, though the time thereof is not.

The payee must be a certain person:

It means that the person in whose favor the instrument is made must be named or described with reasonable certainty.

The term “person” includes individual, body corporate, trade unions, even secretary, director or chairman of an institution. The payee can also be more than one person.

Signature:

A negotiable instrument must bear the signature of its maker. Without the signature of the drawer or the maker, the instrument shall not be a valid one.

Delivery:

Delivery of the instrument is essential. Any negotiable instrument like a cheque or a promissory note is not complete until it is delivered to its payee.

For example, you may issue a cheque in your brother”s name but it is not a negotiable instrument until it is given to your brother.

Stamping:

Stamping of Bills of Exchange and Promissory Notes is mandatory. This is required as per the Indian Stamp Act, 1899. The value of stamp depends upon the value of the pro-note or bill and the time of their payment.

Right to file suit:

The transferee of a negotiable instrument is entitled to file a suit in his own name for enforcing any right or claim on the basis of the instrument.

Notice of transfer:

It is not necessary to give notice of transfer of a negotiable instrument to the party liable to pay.

Presumptions:

Certain presumptions apply to all negotiable instruments, for example, consideration is presumed to have passed between the transferor and the transferee.

Procedure for suits:

In India, a special procedure is provided for suits on promissory notes and bills of exchange.

The number of transfer:

These instruments can be transferred indefinitely until they are at maturity.

Rule of evidence:

These instruments are in writing and signed by the parties, they are used as evidence of the fact of indebtedness because they have special rules of evidence.

Explain and Learn, Promissory Note: Definition, Types, and Features!

A promissory note is a written contract that requires a borrower to pay back a lender an amount of money on a future date. The Concept of the study Explains – Promissory Note: Definition of Promissory Note, Types of Promissory Note, and Features of Promissory Note, Ten-Points, Ten-Key! A promissory note, sometimes referred to as a note payable, is a legal instrument, in which one party promises in writing to pay a determinate sum of money to the other, either at a fixed or determinable future time or on demand of the payee, under specific terms. Also learned, Commercial Bills, Promissory Note: Definition, Types, and Features!

What is the definition of promissory note? Promissory notes usually refer to the borrower as the maker of the note. The borrower generally is said to have made the written agreement because he or she is initiating the transaction. The lender is referred to as the payee because it is the party that first pays the money to the borrower and then receives the payments at a future date. I know this is confusing. Just remember the maker is the borrower and the payee is the lender.

Businesses use notes to finance many different operations. Some companies use short-term notes to finance inventory purchases while other businesses use long-term notes to raise enough capital to purchase large equipment and machinery. Really this note is just a fancy way of saying a loan.

Promissory Note, in the law of negotiable instruments, the written instrument containing an unconditional promise by a party, called the maker, who signs the instrument, to pay to another, called the payee, a definite sum of money either on demand or at a specified or ascertainable future date. The note may be made payable to the bearer, to a party named in the note, or to the order of the party named in the note.

A promissory note differs from an IOU(An IOU (abbreviated from the phrase “I owe you“) is usually an informal document acknowledging debt) in that the former is a promise to pay and the latter is a mere acknowledgment of a debt. A promissory note is negotiable by endorsement if it is specifically made payable to the order of a person.

Definition:

A promissory note is a written agreement to pay a specific amount to specific party at a future date or on demand. In other words, it’s a written loan agreement between two parties that requires the borrower to pay the lender on a day in the future. This could be a set date or a date chosen by the lender.

According to section 4 of the Negotiable Instruments Act, 1881, a promissory note means “Promissory Note is an instrument in writing (not being a bank-note or a currency-note) containing an unconditional undertaking signed by the maker, to pay a certain sum of money only to, or to the order of, a certain person, or to the bearer of the instrument.”

A promissory note is a written and signed contract in which one party promises to pay a specified amount of money to the other party. The terms of a promissory can be tailored to the parties’ needs, as far as the amount borrowed, whether interest will be charged, the schedule or date by which the money must be repaid, and any other needed particulars.

There is no requirement that a promissory note is made on a certain type of paper or document, or that it contains complex language, though it is important to be as specific as possible. In fact, a promissory written and signed on a scrap piece of paper, back of a napkin, or even in an email or text message, is just as valid as a note drawn up by a lawyer.

Types of Promissory Note:

Though every good promissory note contains certain elements, there are several types of promissory note. These notes are largely classified by the type of loan issued or purpose for the loan. All of the following types of the promissory note are legally binding contracts.

Personal Promissory Note: This type is used to record a personal loan made between two parties. While not all lenders use legal writings when dealing with friends and family, it helps avoid confusion and hurt feelings later. A personal promissory note shows good faith on behalf of the borrower, and provides the lender with recourse should the borrower fail to pay back the loan.

Commercial Promissory Note: A commercial promissory note is typically required with commercial lenders. Commercial promissory notes are often more strict than personal notes. If the borrower defaults on its loan, the commercial lender is entitled to immediate payment of the full balance, not just the past due amount. In most cases, the lender on a commercial promissory note can place a lien on the borrower’s property until payment in full is received.

Real Estate Promissory Note: A real estate promissory note is similar to a commercial note, as it often stipulates that a lien can be placed on the borrower’s home or other property if he defaults. If the borrower does default on a real estate loan, the information can become public record.

Investment Promissory Note: An investment promissory note is often used in a business transaction. Investment promissory notes are exchanged to raise capital for the business, and they often contain clauses that deal with returns on investments for specific periods of time.

Features of a Promissory Note:

The promissory note must be in writing- Mere verbal promises or oral undertaking does not constitute a promissory note. The intention of the maker of the note should be signified by writing in clear words on the instrument itself that he undertakes to pay a particular sum of money to the payee or order or to the bearer

It must contain an express promise or clear undertaking to pay- The promise to pay must be expressed. It cannot be implied or inferred. A mere acknowledgment of indebtedness is not enough.

The promise to pay must be definite and unconditional- The promise to pay contained in the note must be unconditional. If the promise to pay is coupled with a condition, it is not a promissory note.

The maker of the pro-note must be certain- The instrument should show on the fact of it as to who exactly is liable to pay. The name of the maker should be written clearly and ascertainable on seeing the document.

It should be signed by the maker- Unless the maker signs the instrument, it is incomplete and of no legal effect. Therefore, the person who promises to pay must sign the instrument even though it might have been written by the promisor himself.

The amount must be certain- The amount undertaken to be paid must be definite or certain or not vague. That is, it must not be capable of contingent additions or subtractions.

The promise should be to pay money- The promissory note should contain a promise to pay money and money only, i.e., legal tender money. The promise cannot be extended to payments in the form of goods, shares, bonds, foreign exchange, etc.

The payee must be certain- The money must be payable to a definite person or according to his order. The payee must be ascertained by name or by designation. But it cannot be made payable either to bearer or to the maker himself.

It should bear the required stamping- The promissory note should, necessarily, bear sufficient stamp as required by the Indian Stamp Act, 1889.

It should be dated- The date of a promissory note is not material unless the amount is made payable at the particular time after date. Even then, the absence of date does not invalidate the pro-note and the date of execution can be independently proved. However to calculate the interest or fixing the date of maturity or lm\imitation period the date is essential. It may be ante-dated or post-dated. If post-dated, it cannot be sued upon till ostensible date.

Demand- The promissory note may be payable on demand or after a certain definite period of time.

The rate of interest- It is unusual to mention in it the rated interest per annum. When the instrument itself specifies the rate of interest payable on the amount mentioned it, interest must be paid at the rate from the date of the instrument.

Explain and Learn, Bill of Exchange: Content, Parties, and Advantages!

The Concept of the study Explains – Bill of Exchange: Content of Bill of Exchange, Parties of Bill of Exchange, and Advantages of Bill of Exchange! Definition of Bill of Exchange: Bill of Exchange, can be understood as a written negotiable instrument, that carries an unconditional order to pay a specified sum of money to a designated person or the holder of the instrument, as directed in the instrument by the maker. The bill of exchange is either payable on demand, or after a specified term. Also learned, Bill of Exchange: Content, Parties, and Advantages!

In a business transaction, when the goods are sold on credit to the buyer, the seller can make the bill and send it to the buyer for acceptance, which contains the details such as name and address of the seller and buyer, amount of bill, maturity date, signature, and so forth.

An instrument which a creditor draws upon his debtor.

It carries an absolute order to pay a specified sum.

The sum is payable to the person whose name is mentioned in the bill or to any other person, or the order of the drawer, or to the bearer of the instrument.

It requires to be stamped, duly signed by the maker and accepted by the drawee.

It contains the date by which the sum should be paid to the creditor.

For Example:

Sam gives a loan of Rs.1,00,000 to Alex, which Alex has to return after three months. Further, Joseph has bought certain goods from Peter, on credit for Rs. 1,00,000. Now, Joseph can create a document directing Alex, to pay Rs. 1,00,000 to Peter, after three months. The instrument will be called as Bill of Exchange, which is transferred to Peter, on whom the payment is due, for the goods purchased from him.

Parties to a Bill of Exchange:

There are three parties viz. ‘Drawer’, ‘Drawee’ and ‘Payee’ to a bill of exchange.

Drawer: A bill of exchange is drawn upon the buyer/debtor by the seller/creditor and the drawer is the person who makes and draws the bill. The drawer is entitled to receive money from the debtor.

Drawee: The person upon whom the bill of exchange is drawn is known as drawee. Bill of exchange is drawn on the drawee who is the purchaser of goods. The Drawee of a bill is called the acceptor when he writes the words “accepted” and puts his signatures on it. This process is known as acceptance. After acceptance, the bill of exchange becomes a legal document. This document now binds the drawee to honor the bill on the due date. This acceptance may be general or qualified. In the case of general acceptance, without stating any conditions, the only sign of the acceptor is required. However, in the case of qualified acceptance, the name of the bank or specified place for payment is mentioned.

Payee: The person to whom the payment is made is known as payee. In some cases, the drawer of the bill also becomes the payee when he himself keeps the bill till the date of maturity. Drawer and Payee is usually the same person.

However, in the following cases drawer and payee are two different persons:

(i) When the bill is discounted by the drawer, the person who discounted the bill becomes the payee.

(ii) When the bill is endorsed to a creditor, the endorsee will become the payee.

The content of Bills of Exchange:

The contents of bills of exchange are as under:

Date: The date of the bill on which it is drawn should be written on the top right comer of the bill. This aspect is very important to determine the maturity date of the bill.

Term: This is the tenure of the bill and runs from the date of the bill. This should be specified in the body of the bill. The grace period of three days should be given after the expiry of the term from the date of the bill.

Amount: Amount of the bill should be given both in figures and words. The amount in figures should be mentioned on the top left corner of the bill and amount in words should be mentioned in the body of the bill.

Stamp: Stamp of proper value which depends on the amount of bill shall be affixed on the bills of exchange.

Parties: There may be three parties to the bills of exchange, drawer, drawee, and payee. However, in some cases, drawer and payee may be the same person. All the names of the parties and their addresses should also be invariably mentioned in the bills of exchange.

For Value Received: This aspect is most important in the sense that law does not consider those agreements which have been made without consideration. Consideration means in lieu of and in the context of bills of exchange, it means that the bill has been issued in exchange of some consideration i.e., benefit has already been received.

Advantages of Bills of Exchange:

The bills of exchange are used frequently in business as an instrument of credit due to the following reasons:

Legal Relationship: Issuing bills of exchange provides a framework which converts and establishes a legal relationship between seller and buyer, from creditor and debtor to drawer and drawee. In the case of any dispute between the parties, this relationship provides a conclusive proof in the court of law.

Terms and Conditions: Bill of exchange contains all terms and conditions of payments viz., amount of the bill, date of payment, place of payment, interest to be paid if any. The maturity date of the bill is also known to the parties to the bill so they can make necessary arrangement for funds.

Mode of Credit: Bill of exchange has been defined as a negotiable instrument under the Negotiable Instruments Act, 1881. The buyer can buy the goods on credit and pay after the period of credit with the help of bill of exchange. In case of urgency, the drawer can also get the payment by discounting the bill from the bank and without waiting for the maturity period.

Easy Transferability: Bill of exchange can be used for settling the debt of the creditors. Mere delivery and endorsement of the bill give a valid title to the endorsee.

Wider Acceptance: In case of the foreign bill, wider acceptance is given to the parties through which payments can be received and made easily.

Mutual Accommodation: Sometimes, the bill can be issued for mutually accommodating the parties so that financial help can be given to each other.

Explain and Learn, Bill of Exchange: Meaning, Definition, and Features!

A bill of exchange is generally drawn by the creditor on his debtor. The Concept of the study Explains – Bill of Exchange: What is a Bill of Exchange? Meaning of Bill of Exchange, Definition of Bill of Exchange, and Features of Bill of Exchange! It should be accepted either by the debtor or any person(s) on his/her behalf. It is worth mentioning that before its acceptance by the debtor, it is just a draft. It should be accepted either by a person upon whom it is drawn or someone else on his/her behalf. The stage at which the purchaser of goods signs the draft and writes ‘Accepted’ on it, it becomes a bill of exchange. Also learned, Bill of Exchange: Meaning, Definition, and Features!

What is a Bill of Exchange?

According to section 5 of the Negotiable Instruments Act, 1881, defines Bill Of Exchange as “A bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument.”

A promise or order to pay is not “conditional”, within the meaning of this section and section 4, by reason of the time for payment of the amount or any installment thereof being expressed to be on the lapse of certain period after the occurrence of a specified event which, according to the ordinary expectation of mankind, is certain to happen, although the time of its happening may be uncertain.

The sum payable may be “certain”, within the meaning of this section and section and section 4, although it includes future indicated rater of change, or is according to the course of exchange, or is according to the course of exchange, and although the instrument provides that, on default of payment of an installment, the balance unpaid shall become due.

The person to whom it is clear that the direction is given or that payment is to be made may be a “certain person,” within the meaning of this section and section 4, although he is misnamed or designated by description only.

Meaning of Bill of Exchange:

T.P Mukherjee law Dictionary with pronunciation defines Bill of Exchange as under: “A bill of exchange is an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay, on demand or at a fixed or determinable future time, a sum certain in money to or the order of a specified person or to bearer.”

The legal and commercial dictionary defines Bill of Exchange as under: “Bill of Exchange includes a hundi and a cheque. A bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of certain. The person or to the bearer of the instrument.”

Black‘s Law Dictionary defines Bill of Exchange as under: “Bill of Exchange. A three-party instrument in which the first party draws an order for the payment of a sum certain on the second party for payment to a third party at a definite future time.”

Wharton ‘s law lexicon Dictionary defines Bill of exchange as under: “As an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand or at a fixed or determinable future time a sum certain in money to or to the order of a specified person, or to bearer.”