The Account is the art of conveying financial information about a business unit for shareholders and managers etc. Accountancy has call ‘business language’. In Hindi, the words ‘लेखा विधि’ (account law) and ‘लेखाकर्म’ (accounting) are also useful in ‘Accountancy’. Accounting Content, Financial, and Accountancy!

Also learn, Accountancy is a branch of mathematical science that is useful in finding out the reasons for success and failure in business. The principles of accountancy are applicable to business units on three divisions of practical arts, namely, accounting, bookkeeping, and auditing.

As Well as the definition “Accountancy refers to the art of writing business practices in a scientific manner and classifying articles and preparing summaries and interpreting the results.”

The functioning of Accountancy is to provide quantitative information regarding economic units, which are basically financially inadequate. Which is useful in taking financial decision-making, accountancy, identifying, and measuring. Analyzing information relevant to an economic event of an organization There is a process for doing and collecting. Which is used to prompt users of this information.

Diminishing or Reducing Balance Method; Under this method, depreciation calculates at a certain percentage each year on the balance of the asset which is brought forward from the previous year. The article from the calculation of Depreciation methods, the chapter of Depreciation in the Accounting Book. The amount of depreciation charged on each period is not fixed but it goes on decreasing gradually as the beginning balance of the asset in each year will reduce. Thus, the amount of depreciation becomes higher at the earlier periods and becomes gradually lower in subsequent periods, when repairs and maintenance charges increase gradually.

Diminishing or Reducing Balance Method of Depreciation: Meaning, Definition, Advantages, Disadvantages, and Differences.

What is the Diminishing or Reducing Balance Method? Reducing Balance Method, also known as declining balance depreciation or diminishing balance depreciation, the depreciation charges at a fixed rate like the straight-line method (also known as fixed installment method or straight-line depreciation). However, unlike the fixed installment method, the rate percent not calculates the cost of assets but on the book value of the asset, which in turn calculates by subtracting depreciation from its cost.

Under reducing-balance, the rate of depreciation is deliberately calculated to be higher, so most of the benefits of deducting the depreciation expense are seen early on. Typically, the percentages used are 200% (the double-declining balance formula) and 150%. Because you’re subtracting a different amount every year, you can’t simply repeat the same calculation each year, as you can with the straight-line method. As mentioned earlier, this approach is particularly useful for a property whose value will decrease rapidly after you acquire it.

Definition of Diminishing or Reducing Balance Method:

Diminishing Balance Method of Depreciation also called as reducing balance method where assets depreciate at a higher rate in the initial years than in the subsequent years. Under this method, a constant rate of depreciation applies to an asset’s (declining) book value each year. This method results in accelerated depreciation and results in higher depreciation values in the early years of the life of an asset.

The book value of an asset obtains by deducting depreciation from its cost. The book value of assets gradually reduces on account of charging depreciation. Since the depreciation rate percent applies to reduce the balance of assets, this method calls reducing balance method or diminishing balance method.

Under the fixed installment method the amount of annual depreciation remains the same but under reducing balance method the amount of annual depreciation gradually reduces. This method is especially suitable for assets with long life, e.g., plant and machinery, furniture, motor car, etc.

Under this method, the real cost of using an asset is the depreciation and repair expenses so this method gives better results because in the early years when repair expenses are less the depreciation is more. As the asset gets older repair charges on its increase and the number of depreciation decreases. So the combined effect of both these costs remains almost constant on the profit and loss of each year.

Advantages of Diminishing or Reducing Balance Method:

The following advantages below are;

It is a simple and easy method.

Every year, there is an equal burden for using the asset. This is because depreciation goes on decreasing every year whereas the cost of repairs increases.

The obsolescence problem gives due care since the major part of the depreciation charges in earlier years and the management may find it easy to replace the asset.

All items including additions are added together and depreciated at the same rate.

Income tax authorities recognize this method.

Disadvantages of Diminishing or Reducing Balance Method:

The following disadvantages below are;

It is difficult to determine an appropriate rate of depreciation.

The value of the asset cannot be brought down to zero.

It results in lower Net Income during the initial years of an asset as Depreciation is higher initially.

It is not an ideal method for those assets which don’t lose their value quickly like Equipment and Machinery.

Depreciation is neither based on the use of the asset nor distributed evenly throughout the useful life of the asset.

Diminishing or Reducing Balance Method of Depreciation, Image from Pixabay.

Differences between the Straight Line Method and Diminishing or Reducing Balance Method:

Key differences between the straight-line method and reducing balance method enumerate as following;

Differences in Straight-line method:

Meaning; Under this method, the cost of an asset uniformly fixed divides into the number of years of the useful life of an asset.

The rate of depreciation and the amount remain constant.

The cost of assets each year forms the basis of determining the depreciation percentage.

As the asset ages, the cost of its repair goes up. But as mentioned in point number one, the depreciation amount remains unchanged. This diminishes annual profit.

The value of an asset at the end of its life is zero.

The computation of depreciation under the straight-line method is relatively easy and straightforward.

Straight Line Depreciation Method is ideal for those assets which require negligible maintenance expenses and are not prone to technological obsolescence.

Differences in Diminishing or Reducing balance method:

Meaning; Under this method, a constant rate applies over the assets declining book value (Cost minus Accumulated Depreciation).

The rate of depreciation remains unchanged but the amount gradually decreases.

The book value of assets forms the basis of determining depreciation percentage.

As the asset ages, the cost of its repair goes up, but so does the depreciation amount. These two balance each other and hence there is little or no effect on annual profit/loss.

The value of an asset at the end of its life is never zero.

Computation of depreciation under reducing balancing method is always possible, but it comes with its share of complexities.

Declining Balance Method is appropriate for assets that require more repairs and maintenance expenses as they get older and also for those assets which are prone to technological obsolescence as it results in higher depreciation during the initial years of an asset’s life.

Differences between the Straight Line Method and Diminishing or Reducing Balance Method.

Forensic accounting is a branch of accounting that focuses on investigating the business and financial records to determine if fraud, money laundering, or other crime has occurred. The article is explaining Prevention with Techniques of Forensic Accounting, also studies along with the Advantages and Disadvantages of Forensic Accounting. “Forensic” means “belonging to or suitable to use in a court of law”, which is why forensic accountants strive to produce findings that can use in court.

Here is Explaining the Advantages, Disadvantages, Prevention with Techniques of Forensic Accounting.

These professionals are also calling on to give evidence during trials. Forensic accounting offers several benefits at first glance but, if you look closer, you’ll see that it also has its drawbacks. A forensic accountant can assist in the areas of Bankruptcy, Economic Damages, Family Law, Valuation and Fraud Prevention/Detection.

Specialized skill sets and knowledge needs for the practitioner to be effective. Because of what is required of a forensic accountant in these areas it is also important for them to be effective communicators to assist the attorney to accomplish their objective [1].

Forensic Accounting as Prevention [2]:

As respects a suitable reaction to a misrepresentation that has been distinguished, each foundation requires an incorporated corporate methodology. An irreverent business environment defiles genuine representatives. The economy can’t manage the cost of business to wind up a facilitator for wrongdoing and unscrupulousness, simply because it has ended up helpful not to convey guilty parties to equity.

In building up a fitting misrepresentation reaction arrangement, a foundation must consider the accompanying strides:

What are the association’s real hazard ranges and what is its arrangement position on culprits of misrepresentation?

To whom is the duty regarding dealing with the reaction apportioned? What is the level of extortion mindfulness inside an association?

Are controls powerful?

Are clients or exchanging accomplices mindful of the organization’s strategy on misrepresentation?

Do representatives comprehend the organization’s state of mind to misrepresentation and contemptibility?

Can representatives report misrepresentation secretly? Is enrollment hones perfect with a legit workforce?

Do disciplinary procedures apportion equity fairly and all the more vitally, are then seen to do as such?

Techniques of prevention of Forensic Accounting (Fraud) [2]:

The customary bookkeeping and evaluating with the assistance of various bookkeeping devices like proportion procedure, income strategy, a standard measurable device examination of proofs are all a player in legal bookkeeping.

In cases including critical measures of information, the present-day legal bookkeeper has innovation accessible to acquire or source information, sort and investigate information and even evaluate and stratify comes about through PC review and different strategies. Smith (2005), Gavish(2007), Dixon (2005), Frost (2004), Cameron (2001) had suggested some of the methods require in Forensic Accounting to inspect the cheats are:

Benford’s Law:

In 2000, Mark Nigrini distributed a critical book called “Advanced analysis using Benford’s Law”. Nigrini (2000). Even though Benford’s Law is presently exceptionally old and was examined in extortion writing. Slope (1995); Busta (1998); Nigrini(1999) before the book, Nigrini’s work acquainted the procedure with the substantial group of onlookers of reviewers.

It is a numerical instrument and is one of the different approaches to figure out if variable under study is an instance of inadvertent blunders (missteps) or extortion. On distinguishing any such marvel, the variable under study subjects to a definite examination. The law expresses that manufactured figures (as a marker of extortion) have an alternate example from irregular figures.

Meaning and Definition:

The means of Benford’s law are extremely basic. Once the variable or field of budgetary significance chooses, the left-most digit of the variable under study separate and compress for the whole populace. The rundown finishes by grouping the main digit field and ascertaining its watched check rate. At that point, Benford’s set connects. A parametric test called the Z-test completes gauging the criticalness of fluctuation between the two populaces, i.e.

Benford’s rate numbers for the first digit and watched rate of the first digit for a specific level of certainty. On the off chance that the information affirms to the rate of Benford’s law, it implies that the information is Benford’s set, i.e. there is 68% (right around 2/third) risk of no blunder or extortion. The principal digit may not generally be the main pertinent field.

Benford has given separate sets for second, 3rdand for the last digit also. It likewise works for blend numbers, decimal numbers, and adjusted numbers. There are numerous preferences of Benford’s Law like it not influence by scale invariance and is of help when there is no supporting archive to demonstrate the legitimacy of the exchanges.

Theory of Relative Size Factor (RSF):

It highlights every strange variance, which might steer from misrepresentation or certified blunders. RSF measures the proportion of the biggest number to the second biggest number of the given set.

Practically speaking there exist certain cutoff points (e.g. budgetary) for every element, for example, merchant, client, worker, and so on. These points of confinement might characterize or investigate from the accessible information if not characterize.

On the off chance that there is any stray occasion of that is route past the typical extent, then there is a need to examine further into it. It helps in the better discovery of peculiarities or outliners.

In records that fall outside the endorsed extent are associated with blunders or extortion. These records or fields need to identify with different variables or components to discover the relationship, consequently setting up reality.

Computer-Assisted Auditing Tools (CAATs):

CAATs are PC programs that the reviewer use as a major aspect of the review methods to process information of review criticalness contained in a customer’s data frameworks, without relying upon him. CAAT helps reviewers to perform different evaluating methodologies; for example, 1) Testing points of interest of exchanges and adjusts; 2) distinguishing irregularities or huge changes; 3) Testing general and application control of PC frameworks; 4) Sampling projects to concentrate information for review testing, and; 5) Redoing figuring performed by bookkeeping frameworks.

Data mining techniques:

Black (2002); Paletta (2005); Lovett (1955) It is an arrangement of help strategies intended to consequently mine substantial volumes of information for a new, cover-up or unforeseen data or examples. Information mining procedures are arranged in three ways: Discovery, Predictive displaying and Deviation, and Link examination.

It finds the typical learning or examples in information, without a predefined thought or theory about what the example might be, i.e. with no earlier information of fraud. It clarifies different affinities, affiliation, patterns and varieties as the contingent rationale. In prescient displaying, designs found from the database utilizes to foresee the result and to figure information for new esteem things.

In Deviation examination the standard discovers initially, and after that those things are recognizing that go amiss from the typical inside an offered edge (to discover abnormalities by removed examples). Join disclosure has risen as of late to detect a suspicious example. It, for the most part, uses deterministic graphical strategies, Bayesian probabilistic easygoing systems. This technique includes “design coordinating” calculation to “concentrate” any uncommon or suspicious cases.

Ratio Analysis:

Another helpful fraud recognition procedure is the figuring of information investigation proportions for key numeric fields. Like money related proportions that give signs of the monetary soundness of an organization, information investigation proportions report on the extortion wellbeing by distinguishing conceivable side effects of fraud.

According to the perspectives by Albrecht, et. Al (2009) three generally utilized proportions are:

The proportion of the most noteworthy quality to the least esteem (max/min).

The proportion of the most astounding quality to the second most noteworthy worth (max/max2), and.

Also, the proportion of the present year to the earlier year.

Utilizing proportion investigation, a money related master concentrates on connections between indicated expenses and some measure of creation, for example, units sold, dollars of offers or direct work hours. For instance, to touch base at overhead expenses per direct work hour – Total overhead expenses may isolate by aggregate direct work hours. Proportion investigation may help forensic accountants to gauge costs.

After Prevention and Techniques, The following three advantages of Forensic Accounting below are;

It helps to solve financial crimes: As mentioned above, forensic accounting can greatly help in solving financial crimes. These can involve bribery within government offices as well as fraud and money laundering within business organizations. Forensic accounting not only helps with gathering evidence for crimes but can also use in detecting and identifying crimes.

It helps monitor professionals: Forensic accounting can use to assess the work of professionals, including accountants themselves. The findings from this assessment, in turn, can use to file professional negligence claims against those who have been proving to have made critical errors (whether intentionally or not).

Also, it helps businesses with their finances: Businesses can use forensic accounting to detect anomalies among their staff and with third parties they’re working with. For instance, a company can ask a forensic accountant to check an employee’s purchasing records to see if all of his purchases were for business use or if he diverted some for his personal use.

Disadvantages of Forensic Accounting [3]:

The following three disadvantages of Forensic Accounting below are;

It takes a lot of time: Forensic accounting is never easy. It requires accountants to go through every piece of document to ensure that their investigation is complete and that they’ll uncover every evidence that will solve the case. This can take many days and can even stretch to many weeks or months, depending on the magnitude of the case; the size of the organization involved, and the number of documents to review.

They can be expensive: Because of the lengthy period need, forensic accounting can turn out to be expensive. This isn’t a problem for huge corporations that have more than enough funds; but, it can be an issue for smaller businesses that have limited budgets.

Also, it can be distracting: Forensic accounting can cause a distraction among employees, particularly when outside accountants are brought in. The process can disrupt the staff’s normal routine and cause their productivity and efficiency to suffer.

What is Forensic Accounting? The application of accounting skills to provide quantitative financial information about matters before the courts. This article explains to Forensic Accounting definition along with their practice and also need to know about by concept. The series of accounting scandals in the early years of the 21st century led to profound changes and transition in the accounting profession, laws, and regulations. Among these developments was the emergence of forensic accounting.

Forensic Accounting: Definition, Concept, Need, Practice, Role, and significance.

Forensic accounting frequently uses on construction claims, financial contract disputes, environmental claims, government contract claims, and fraud investigations, among others. Professionals involved in this field are often engaged in examination and evaluation of financial evidence; the advancement and improvement of computer applications; that will aid and support the forensic accountants in analyzing and presenting financial evidence; providing services and support in legal proceedings. Also, Forensic accounting is the study of financial fraud and misconduct.

The Association of Certified Fraud Examiners described financial accounting as;

“A set of skills used in potential or actual civil or criminal cases, including generally accepted accounting and auditing ones; determining loss of profits, revenues, property, or damage; and assessment of internal controls, fraud, and everything else that leads to the applying of accounting knowledge to the legal system.”

As well as, Forensic accounting is an integration of auditing, accounting, and investigative skills, and presents an accounting evaluation; that is appropriate and acceptable to the court; which will then establish the basis for discourse, debate, and the settlement of arguments.

Definition of Forensic Accounting:

The definition of forensic accounting is changing in response to the growing needs of corporations.

Bologna and Lindquist had defined forensic accounting as;

“The application of financial skills, and an investigative mentality to unresolved issues, conducted within the context of rules of evidence. As an emerging discipline, it encompasses financial expertise, fraud knowledge, and a sound knowledge and understanding of business reality and the working of the legal system.”

According to AICPA as;

“Forensic accounting is the application of accounting principles, theories, and discipline to facts or hypotheses at issues in a legal dispute and encompasses every branch of accounting knowledge.”

Forensic accounting defines by Zia as,

“The science that deals with the relation and application of finance, accounting, tax, and auditing knowledge to analyze, investigate, inquire, test and examine matters in civil law, criminal law, and jurisprudence in an attempt to obtain the truth from which to render an expert opinion.”

Concept of Forensic Accounting:

After definition, the principle point of forensic accounting [Are from, for a support article] is not just to see how extortion was submitted, however, to report it with the most astounding conceivable precision. As indicated by Gomide, a great Forensic accounting consolidates accounting examination furthermore requires great accounting and investigative aptitudes.

In the talk, EFG refers to that;

“It falls under general data or certain points, or subjects as it can sort general articulations that individuals make to portray the subject, as investigative accounting or even Forensic auditing”.

Forensic accounting can characterize as help with a question in regards to assertions or suspicion of extortion; which are liable to include case, master assurance, and inquiry by a fitting power, and examinations of suspected misrepresentation, abnormality or indecency which could prompt common, criminal or disciplinary procedures.

The emphasis is basically on accounting issues; however, the part of the forensic bookkeeper may stretch out to more broad examination which incorporates proof social affairs. It is a result of the way that by definition, forensic assignments are identified with a legal or semi-legal debate determination; that the Forensic specialist requires a fundamental comprehension of the material statutory and customary law, the law of confirmation and the law of methodology.

The most skilfully led examination will be of no quality to the customer ought to the confirmation accumulated rule to forbid or the master accounting witness find to miss the mark in appreciation of the necessities of ability, believability, or autonomy.

Why need to know about Forensic accounting? or Need for Forensic accounting.

Forensic accounting identifies with the use of accounting ideas and systems to lawful issues. Measurable accountants for the most part research and archive money related extortion and cushy wrongdoings. The result of the measurable examination, including appraisals of misfortunes, harms, and resources would utilize as prosecution backing to lawyers and law requirement staff.

They offer imperative help for legitimate cases in numerous regions of the law; for example, securities exchange controls, value altering plans, item risk, shareholder debate, and breaks of agreement. Forensic accounting, forensic auditing or financial forensics is the forte practice range of accounting that depicts engagements; that outcome from genuine or expected debate or suit.

First Things:

“Forensic” signifies “appropriate for use in a courtroom”, and it is to that standard and a potential result that legal accountants, for the most part, need to work. These accountants, additionally alluded to as Forensic examiners or investigative evaluators, frequently need to give master proof at the inevitable trial. Crumbley, D. Larry; Heitger, Lester E.; Smith, G. Stevenson (2005) All of the bigger accounting firms, and also numerous medium-sized and boutique firms, and different Police and Government organizations have pro Forensic accounting divisions.

Inside these gatherings, there might be further sub-specializations: some forensic accountants may, for instance, simply represent considerable authority in protection claims, individual harm claims, extortion, development. Cicchella, Denise (2005). Alternately sovereignty reviews. Parr, Russell L.; Smith, Gordon V. (2010).

Second Things:

“While Forensic Accountants (“FAs”) typically don’t give assessments, the work performed and reports issued will frequently give answers to the how, where, what, why and who. The FAs have and are keeping on advancing as far as using innovation to help with engagements to distinguish oddities and irregularities. Remember that it is not the Forensic Accountants that decide misrepresentation, but rather the court.” Bhasin Madan(2007).

Also, Forensic accountants have been depicting as experience evaluators, accountants, and specialists of legitimate and money related reports that are employed to investigate conceivable suspicions of false movement inside an organization; or are procured by an organization that may simply need to keep deceitful exercises from happening. They likewise give administrations in zones, for example, accounting, antitrust, harms, investigation, valuation, and general counseling.

Third Things:

Forensic accountants have likewise been utilized as a part of separations, protection claims, individual damage claims, fake cases, development, sovereignty reviews, and following psychological warfare by exploring monetary records. Numerous forensic accountants work intimately with law requirement faculty and legal counselors amid examinations and frequently show up as master observers amid trials.

It is an amalgam of forensic science and accounting. Even though the instituting of the term Forensic Accounting says to go back to 1946, the practice is moderately new in Nigeria. Hopewood, A.G.(2009). The requirement for a forensic accountant has been attributed to the way that the review framework in an association has neglect to recognize certain mistakes in the administrative framework.

Forth Things:

Forensic Accounting is examination accounting which includes breaking down, testing, asking and looking at the common and criminal matters lastly giving an impartial and genuine report. Pretty much as forensic examinations and lab reports are requires in the court to understand the homicide and dacoit puzzles; correspondingly forensic accounting assumes a key part in following the financial fraud and clerical wrongdoings.

Be that as it may, forensic accounting covers an extensive variety of operations of which misrepresentation examination is a little part where it is generally predominant. There are two noteworthy angles inside legal accounting hone; prosecution benefits that perceive the part of a Chartered Accountant as a specialist or expert and investigative administrations that make utilization of the Chartered Accountant’s abilities, which could prompt court declaration.

The practice of Forensic Accounting:

Arnoff, Norman B., and Sue C. Jacobs. (2001) had clarified the administrations rendered by the forensic accountants are in incredible interest in the accompanying territories;

Fraud detection where employees commit Fraud:

Where the employee enjoys fake exercises; Where the representatives are gotten to have submitted misrepresentation the forensic accountant tries to find any benefits made by them out of the assets defalcated; then take a stab at questioning them and attempting to discover the concealed truth.

Criminal Investigation:

Matters identifying with money related ramifications the administrations of the forensic accountants are benefited of. The report of the accountants considers getting ready and present as proof.

Outgoing Partner’s settlement:

If the active accomplice is not upbeat about his settlement he can utilize a forensic accountant; who will accurately evaluate his contribution (resources) and also his liabilities effectively.

Cases relating to professional negligence:

Proficient carelessness cases are taken up by the forensic accountants. Non-adaptation to Generally Accepted Accounting Principles (GAAP) or rebelliousness to examining hones or moral codes of any calls; they are expected to gauge the misfortune because of such expert carelessness or deficiency in administrations.

Arbitration service:

Forensic accountants render assertion and intercession administrations for the business group since they experience extraordinary preparing in the region of option question determination.

Facilitating settlement regarding the motor vehicle accident:

As the forensic accountant is very much familiar with the complexities of laws identifying with engine vehicles; and, other applicable laws in power, his administrations get to be vital in measuring monetary misfortune when a vehicle meets with a mishap.

Settlement of insurance claims:

Insurance agencies connect with forensic accountants to have a precise evaluation of cases to settle. Also, policyholders look for the assistance of a legal accountant; when they have to challenge the case settlement as worked out by the insurance agencies. A legal accountant handles the cases identifying with significant misfortune arrangement, property misfortune; because of different dangers, devotion protection and different sorts of protection cases.

Dispute settlement:

Business firms connect with legal accountants to handle contract debate, development claims, item risk cases, and encroachment of patent and trademarks cases; obligation emerging from the break of agreements et cetera.

Matrimonial dispute cases:

Forensic accountants engage cases relating to matrimonial disputes wherein their part simply restricts to following, finding and assessing any type of advantage included.

Aside from learning of accounting, law, and criminology, a forensic accountant likewise should acquaint with corporate financial management and administration. He additionally needs PC aptitudes, great correspondence and meeting abilities.

Forensic accounting is a legal term. It is in its simplest form application of accounting techniques and concepts in issues concerning legal matters. The requirement comes due to the high rate of white-collar crimes like embezzlement, fraudulent financials, and various other financial wrongdoings.

As well as, Forensic Accountant calls upon to investigate various financial frauds by the employees, clients, Customers either independently; or in collusion one another and misappropriating the assets of the company.

Forensic Accountants also help the Government in the enforcement of regulatory requirements. Many bank fraud is common with the collusion of the borrower and bank staff etc.; where the expertise of the Forensic Accountant comes in unfolding the fraud and helping the corporates nail the fraudsters.

Also, Forensic Accountants help needs in price fixations, stock market manipulations and at times even manipulation of the financial figures by the managements to window dress; the balance sheet and profit and loss account figures to hide real facts from the stakeholders and general public; for the funds misused or misappropriated by the top management.

Learn the Concept of Centralized and Decentralized Purchasing; Organization of the purchase function will vary according to particular conditions and ideas. Purchases may centralized or decentralized. This article explains centralized and decentralized purchasing and their point in pdf or ppt – meaning, advantages, disadvantages, and difference. In centralized purchasing, there is a separate purchasing department entrusted with the task of making all purchases of all types of materials. The head of this department usually designates as Purchase Manager or Chief Buyer. Also, in decentralized purchasing, each branch or department makes its purchases.

Here explains the Centralized and Decentralized Purchasing and their topics – Meaning, Advantages, Disadvantages, and Difference.

If the branches of plants are located in different places, it may not be possible to centralize all purchases. What is the difference between centralized and decentralized purchasing? or What are the difference between centralised and decentralised purchasing? or What is the centralised and decentralised purchasing and supply chain functioning? In such cases, decentralized purchasing can better meet the situation by making purchases in the local market by plant or branch managers.

Centralized Purchase refers to purchasing all the requirements under the central point of the organization. Likewise, Decentralized Purchase refers to the purchasing of requirements of each production center in an organization.

Meaning of Centralized and Decentralized Purchasing:

Centralization and Decentralization are the two types of structures, that can find in the organization, government, management, and even in purchasing. Centralization of authority means the power of planning and decision making are exclusively in the hands of top management. It alludes to the concentration of all the powers at the apex level. On the other hand, Decentralization refers to the dissemination of powers by the top management to the middle or low-level management. It is the delegation of authority, at all levels of management.

What is Centralized purchasing?

Under centralized purchasing purchases are made at one central point for the whole organization and material is issued to respective departments or jobs as and when needed. Also, Centralized purchasing is suitable in cases where the organization runs one plant. It will bring about economies of purchasing and buying in small lots will avoid.

It ensures consistent buying policies in the future and purchasing powers are concentrated in the hands of one person, the in-charge of the purchasing department. This type of purchasing is very helpful in the quick implementation of decisions regarding purchasing. It also ensures bulk buying which ensures favorable prices. The staff requirements under this type are limited and specialists in buying may appoint.

Centralized purchasing is further helpful to the vendors since their selling costs are reduced as they can easily coordinate and supply goods to a single buyer instead of a large number of buyers. The most important benefit which can draw from centralized buying is that it keeps the inventories in control and checks the wasteful investment in materials and equipment etc. thereby ensuring the overall economy in purchasing.

What is Decentralized purchasing?

Decentralized purchasing is just the reverse of centralized purchasing. This is suitable for organizations running more than one plant. Under this type, each plant has its purchasing agents. In other words, every department makes its purchases. This also calls localized purchasing. Also, Decentralized purchasing is quite flexible and can quickly adjust following the requirements of a particular plant.

More attention can pay by the departmental head to buying problems as he will be carrying the limited number of activities in his department and he can hold responsible for the purchase of goods and the overall performance of the plant. The serious drawback which emerges from this type is the lack of uniformity in purchasing procedure in the organization.

At the same time, uniformity in prices cannot ensure and every departmental head may not possess the caliber of an expert buyer. This method also poses the problems of coordination among various departments of the organization and usually leads to unplanned buying. In comparison to centralized buying, this method involves a lesser economy in purchasing.

Advantages and Disadvantages of Centralized and Decentralized Purchasing:

The following advantages and disadvantages of centralized and decentralized purchasing below are – PDF;

Advantages of Centralised Purchasing:

A centralized purchasing system generally prefers because of the following advantages of it;

Specialized and expert purchasing staff can concentrate on one department.

Better layout of storage space.

Utilization of high technical skills.

A firm policy can initiate which may result in favorable terms of purchase, e.g., higher trade discount, easy terms of payment, etc.

Standardization of quality of raw material facilitates.

Minimum finance required.

Better supervision of materials usage, and.

Also, better control over purchasing is possible because reckless buying by various individuals avoid. Keeping all records of purchase transactions in one place also helps in control.

Disadvantages of Centralised Purchasing:

A centralized purchasing system generally refuses because of the following disadvantages of it;

The high cost of internal transport.

The creation and maintenance of a special purchasing department lead to higher administration costs which small concerns may not be in a position to afford.

Non-availability of materials for production in time.

Greater risk of obsolescence, and.

Centralized purchasing is not suitable for plants or branches located at different places that are far apart.

Advantages of Decentralized Purchasing:

A Decentralized purchasing system generally prefers because of the following advantages of it;

Materials can purchase by each department locally as and when required.

Timely availability of materials.

Materials are purchasing in the right quantity of the right quality for each department easily.

No heavy investment requires initially.

Less cost of internal transport.

Lower chance of obsolescence.

Purchase orders can place quickly, and.

The replacement of defective materials takes little time.

Disadvantages of Decentralized Purchasing:

A Decentralized purchasing system generally refuses because of the following disadvantages of it;

Organization losses the benefit of a bulk purchase.

Poor layout of space.

More finance requires.

Duplicate purchase of materials.

Specialized knowledge may be lacking in purchasing staff.

There is a chance of over and under-purchasing of materials.

Fewer chances of effective control of materials.

Less technical skill obtains.

More clerical work, and.

Lack of proper co-operation and co-ordination among various departments.

Centralized and Decentralized Purchasing: Meaning, Advantages, Disadvantages, and Difference.

Differences Between Centralized and Decentralized Purchasing:

Learn and understand the points given below are noteworthy. So far as the difference between centralized and decentralized purchasing concerns;

Control on buying exercise effectively, Effective control is not possible.

The economy in large scale purchase is possible, Large scale benefits are not available.

Skills of the purchasing officer are high, Purchasing skill is available from the purchaser or purchasing officer.

Purchasing specialization obtains, Purchasing specialization not obtains.

Uniformity in the purchase follows, There is a lot of difference in the purchase.

Standard materials are purchased, Quality of the material is questionable.

There is a misunderstanding between the production center and purchase department, There is no such misunderstanding since the concerned department purchases the materials.

The comparative advantage and disadvantages of the two systems are as below:

Meaning:

Centralized is the retention of powers and authority concerning planning and decisions, with the top management, knows as Centralization. However, decentralized is the dissemination of authority, responsibility, and accountability to the various management levels know as Decentralization.

Terms of Purchase:

Centralized is Due to the large scale order, better terms of purchase may be available, but Decentralized in Less favorable terms may be available.

Nature:

Centralized is usually involves two people; a manager and his subordinate. But decentralized involves the entire organization; from the top management to individual departments.

Advantage:

Centralized is proper coordination and Leadership, but Decentralized is sharing of burden and responsibility.

Control:

Centralized is controlling by the manager or the delegator controls it. But decentralized control rests with the respective departments or classes.

Need:

Centralized need all organizations to need delegation to get things done, Delegating authority is essential to assign responsibility. But decentralized is an optional mode of working, Organizations can also work in a centralized manner.

Responsibility:

Centralized Responsibility is the delegator can delegate authority but the responsibility remains with him, the delegator is accountable for the task. However, decentralized is the head of the departments responsible for the activities performed under him, Therefore, responsibility is fixed at the department-level.

Involves:

Centralized is involves in Systematic and consistent reservation of authority. Similarly, decentralized involves Systematic dispersal of authority.

Process Costing is a method of costing used to ascertain the cost of a product at each process or stage of manufacture. You will be able to understand the Process Costing based on the points given to them; 1) introduction, 2) meaning of process costing, 3) definition of process costing, 4) characteristics of process costing, 5) objectives of process costing, and 6) principles of process costing. In this method, the costs of materials, wages and overheads are accumulated for each process separately, for a gives period, and then carrying forward cumulatively from one process to the next process till the last process complete.

This article explains the topic of Process Costing: Introduction, Meaning, Definition, Characteristics, Objectives, and Principles.

Process costing is probably the most widely used method of cost ascertainment. Records are also maintaining to account for process losses. These losses may be normal or abnormal. Separate accounting is done for normal and abnormal losses, opening and closing work-in-progress and inter-process profits, if any. This method of costing used in those industries where mass production of identical units undertakes continuously and finish products are subject to several production stages call processes before completion.

The system of process costing is suitable for industries involving continuous production of the same product or products through the same process or set of processes. It is in use in the plant producing paper, rubber products, medicines, chemical products. It is also very much common in flour mill, bottling companies, canning plants, breweries, etc.

Meaning of Process Costing:

They refer to a method of accumulating the cost of production by the process. It uses in mass production industries producing standard products like steel, sugar, chemicals, oil, etc. In all such industries, goods produced are identical and all factory processes are standardizing. Output in such industries consists of like units and every unit of the product undergoes a similar operation in the process.

So it implies that the same cost of material, labor and overhead charges to each unit of the production process. Under this method, costing an individual unit is impossible. It so-calls because under process costing cost of the product ascertain process-wise.

They also know as “Continuous Costing” because industries that adopt process costing undertake the production of goods continuously. They also know as “Average Costing” because the cost per unit of each process ascertains by averaging the expenditure incurred on that process during a period by the number of units produced in that process during the period.

Definition of Process Costing:

After their meaning, Process Costing defines by different scholars as under:

According to Wheldon,

“Process costing is a method of costing used to ascertain the cost of the product at each process, operation or stage of manufacture.”

According to the Institute of Cost and Management Accountants, London,

“Process costing is that form of operation costing which applies where standardized goods are produced.”

Characteristics or Features of Process Costing:

It is that aspect of operation costing which uses to ascertain the cost of the product at each process or stage of manufacture. Where processes are carrying on having one or more of the following characteristics of Process costing:

Production over having a continuous flow of identical products except. Where plant and machinery are shut-down for repairs, etc.

Clearly defined process cost centers and the accumulation of all costs (materials, labor, and overheads) by the cost centers.

The maintenance of accurate records of units and part units produced and cost incurred by each process.

The finished product of one process becomes the raw materials of the next process or operation and so on until the final product obtains.

Avoidable and unavoidable losses usually arise at different stages of manufacture for various reasons. Treatment of normal and abnormal losses or gains is to study in this method of costing.

Extra characteristics:

Sometimes goods are transferring from one process to another process, not at cost price but transfer price just to compare this with the market price and to have a check on the inefficiency and losses occurring in a particular process. The elimination of the profit elements from stock is to learn in this method of costing.

To obtain accurate average costs, it is necessary to measure the production at various stages of manufacture. As all the input units may not convert into finish goods; some may be in progress. The calculation of effective units is to learn in this method of costing.

Different products with or without by-products are simultaneously producing at one or more stages or processes of manufacture. The valuation of by-products and apportionment of the joint cost before the point of separation is an important aspect of this method of costing. In certain industries, by-products may require further processing before they can sell.

The main product of one firm may be a by-product of another firm and in certain circumstances. It may be available in the market at prices which are lower than the cost to the first-mentioned firm. It is essential, therefore, that this cost knows so that advantages can take of these market conditions.

The output is uniform and all units are identical during one or more processes. So the cost per unit of production can ascertain only by averaging the expenditure incurred during a particular period.

Process Costing: Meaning, Characteristics, and Objectives, #Pixabay.

Objectives of Process Costing:

How do you know what cost you need? If you know the total cost of production of each process. The following are the main objectives of process costing:

To Ascertain the Cost of Each Process: It is necessary to know the cost at every stage of production and this fulfills by the process costing method. On this basis, management can decide concerning the make or buy the required commodities.

To Ascertain the Cost of Bye-Product: Bye-product is that which obtains with the main product in the course of the production. For example; while producing mustard oil, the cake also obtains. Which terms as bye-product and the cost of which is necessary to know the actual cost of the main product? Cost of bye-product ascertains by preparing bye-product Account, under process costing.

To Know the Wastage in Each Process of Production: During the courage of production, different wastages, such as; loss in weight, normal wastage, and abnormal wastage, etc. may arise. Management of any concern may know about these wastages by Process Costing Account.

To Ascertain the Profit or Loss of Each Process: The output or the part of output at the stage of every process can sell out either at profit or loss. Thus the management can know about the profit or loss at every process by preparing Processes Account.

The base of the Valuation of Opening and Closing Stock of Each Next Process: If the total cost of production of any process divides by the number of units, we get the cost of production per unit of that particular process and on this basis opening and closing stock of next process value.

Principles of Process Costing:

The essential stages in principles of process costing are:

The factory divide into several processes and an account maintains for each process. Each Process Account debit with material cost, labor cost, direct expenses, and overheads allocate or apportion to the process.

The output of a process transfer to the next process in the sequence. In other words, the finished output of one process becomes input (materials) of the next process. The production records of each process are keeping in such a way as to show. The quantity of production and the wastage and scrap and the cost of production of each process for each period.

Extra things:

In some cases, the whole output of one process not transfers to the next process. A part of the output may transfer to the next process. And, a certain portion of the output may sell in semi-finish form or may keep in stock and transfer to Process Stock Account. If the output of any process sells at a profit in semi-finish form. Then profit on that particular sale will show on the debit side of that concerning profit, as profit on goods sale or transfer.

In case there is loss or wastage of units in any process. The loss has to born by the good units produced in that process and as a result. The average cost per unit increases to that extent. It may note that, if there is loss or wastage in any process, the quantity of loss or wastage should enter on the credit side of the concerned Process Account in the quantity column. In case the wastage has some scrap value. It should appear on the credit side of the concerned Process Account in the value column against the entry for wastage. But, if the scrap value of the wastage does not specifically give in the problem. It should take as nil.

The total cost of production of each process for a particular period divided by the number of units produced in that process during that period. And, the average cost per unit of production for a period obtain. The finished output of the last process transfer to the Finish Goods Account.

The single Costing method of the ascertainment of the cost of production is suitable for those industries in which manufacturing is continuous and units of output are identical. You will be able to understand the Single Costing based on the points given to them; introduction, the meaning of single costing, the definition of single costing, characteristics of single costing, and objectives of single costing. One operation costing method of costing by units of production and adopts where production is uniform and a continuous affair, units of output are identical and the cost units are physical and natural.

This article explains the topic of Single Costing: Introduction, Meaning, Definition, Characteristics, and Objectives.

The cost per single determines by dividing the total cost during a given period by the number of units produced during that period. This method of costing generally adopt where an undertaking engages in producing only one type of product or two or more products of the same kind but of varying grades or quality. The industries where this method of costing uses are the dairy industry, beverages, collieries, sugar mills, cement works, brick-works, paper mills, etc.

Meaning of Single Costing:

Single or Unit or Output costing is the method of costing in which cost is ascertained per unit of a single product in continuous manufacturing activity. Every Single or per unit, the cost calculates by dividing total production cost by several units produced.

This method knows as “Single costing” as industries adopting this method manufacture, in most cases, a single variety of products. This method also knows as “Unit costing”, as not only the cost of the total output but also the cost per unit of output ascertains under this method. Under this method cost units are identical. This method also calls “Output costing”, as the cost ascertains for the total output of a product.

Definition of Single Costing:

The following definitions below are;

According to J.R. Batliboi,

“Single or output cost system is used in businesses where a standard product is turned out and it is desired to find out the cost of a basic unit of production.”

The Institute of Cost and Management Accountants, London,

“output costing is the basic costing method applicable where goods or services result from a series of continuous or repetitive operations or processes to which costs are charged before being averaged over the units produced during the period.”

From the above definitions, it is clear that this costing is a method of costing under. Which there is the costing of a single product, which produces by continuous manufacturing activity. Though under this method of costing a single variety of product manufacturers. It may vary concerning size, grade, color, etc. The example of industries that make use of this method of costing is; brick, sugar, cloth, coal, cement, fisheries, food canning, quarries, plantation industries, etc.

Thus single costing adopts for cost ascertainment in those manufacturing organizations. Which is engaging in producing only one type of product or two or more products of the same kind but of varying grades or qualities? This method uses in industries like mines, quarries, oil drilling; breweries, cement works, brick-works, .sugar mills, steel manufacture and aluminum products, etc.

In all those industries where single costing uses, there is a standard or natural unit of cost. For example, a tonne of coal in collieries, one thousand bricks in brick-works, a quintal of sugar in the sugar industry, a tonne of cement in the cement industry, etc. In this costing, the cost of production usually ascertains by preparing a cost sheet or a cost statement.

Single Costing: Meaning, Characteristics, and Objectives, #Pixabay.

Characteristic or Features of Industries Which Use Single Costing:

The following are the characteristics or features of the industries where the single costing method uses:

The cost per unit of output, determined under a single. Costing enables the management to make a real comparison between different periods and between different firms within the same industry, as the unit of output is a common factor between different periods and between different firms within the same industry.

Equality of cost is an important feature of this method. That is, under this method, identical cost units will have identical costs.

Production is on a large scale and is continuous.

The units of production are identical and homogeneous.

One cost is the method of costing adopt in concerns where there is a production of a product. Or, a few grades of the same product differing only in size, shape or quality by the continuous process of manufacture. The units of production or output are identical and the costs of units are physical and natural.

The cost units are physical and natural and capable of being expressed in a convenient unit of measurement.

This method is the simplest method of all the methods of cost; in the sense that the cost collection and the cost ascertainment are quite simple.

In most cases, the unit of measure is also the cost unit, viz., one unit (in the case of T.V., radio, camera), 1,000 units (in the case of bricks), one gross (in the case of pencils, slates, bolts, and nuts), one liter (in the case of paints), one tonne (in the case of coal, cement, and steel), one bale (in the case of cotton), etc.

Objectives of Single Costing:

Single costing is a very simple method of costing. Its principal objectives are as follows;

To ascertain the per-unit cost of production by dividing the total cost of production by the number of units produced.

Help in the preparation of tenders and fixation of selling prices.

To facilitate a comparison of the cost of production of two accounting periods.

To control the cost of the product through the comparative study of the costs of any two periods. Or, the comparison of the actual costs with the Pre-determined standard cost.

The analyze the expenditure by nature, classify them into the element of cost and know. The extent to which each element of cost contributes to the total cost.

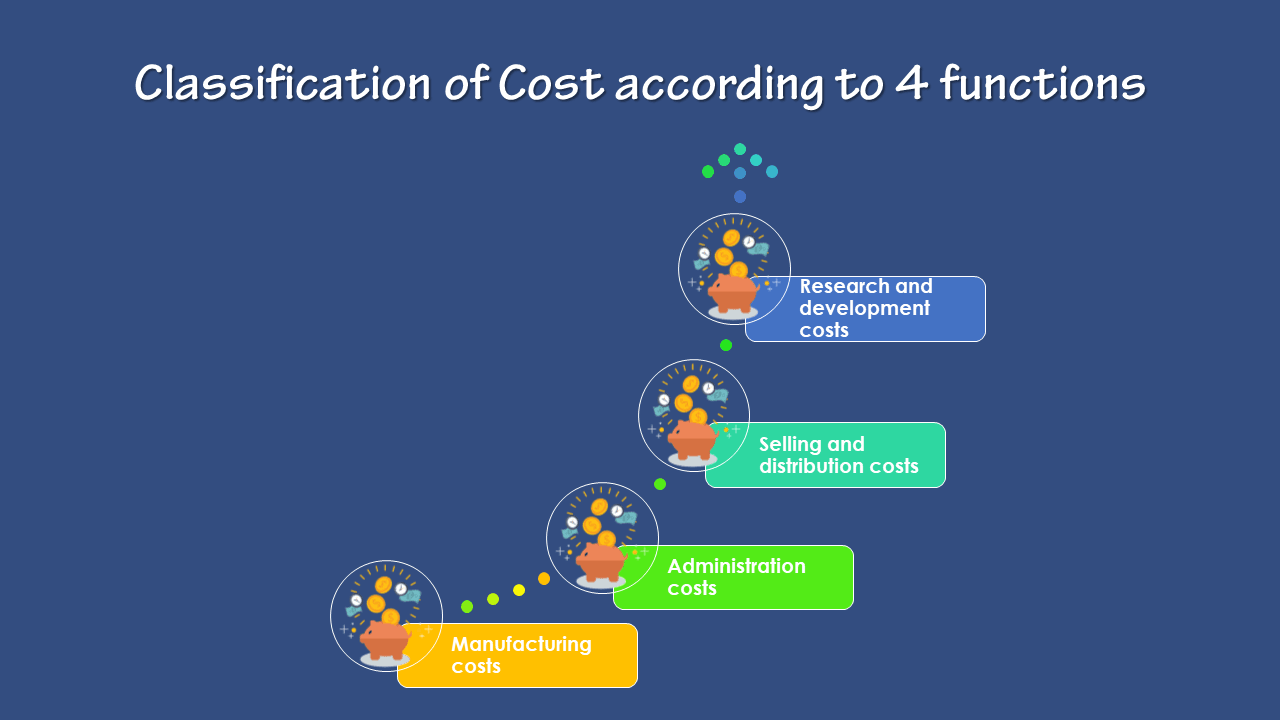

Classification of Cost according to 4 functions: This is a traditional classification. A business has to perform several functions like manufacturing, administration, selling, distribution, and research.

This article explains the topic of the Classification of Cost according to 4 functions.

Cost may have to ascertain for each of these functions.

On this basis, costs are classifying into the following groups:

How to the Classification of Cost according to 4 functions?

Manufacturing costs:

This is the cost of the sequence of operations. Which begins with supplying materials, labor, and services and ends with the completion of production. What are the manufacturing costs? Manufacturing costs are the costs of materials plus the costs to convert the materials into products. Manufacturing costs are the costs incur during the production of a product.

The costs are typically present in the income statement as separate line items. An entity incurs these costs during the production process. Direct material is the materials uses in the construction of a product. Direct labor is that portion of the labor cost of the production process that assigns to a unit of production. Manufacturing overhead costs are applying to units of production based on a variety of possible allocation systems. Such as by direct labor hours or machine hours incurred.

Administration costs:

This is general administrative cost and includes all expenditure incurs in formulating the policy, directing the organization and controlling the operations of an undertaking. Which is not directly related to production, selling and distribution, research and development activity or function.

Define administrative costs as the costs not directly related to operations. Generally, they are incurring in the process of directing a company. These costs, though indirect, are still important because they assist those who operate and sell company products by making their work more efficient.

Selling and distribution costs:

Selling cost is the cost of seeking to create and simulating demand and securing orders. Distribution cost is the cost of a sequence of operations. This begins with making the packed product available for despatch and ends with making the reconditioned returned empty package for re-use. There are some overhead about them;

What is Selling Overhead? Selling overhead is the indirect expenses incur for seeking to create and stimulate demand for the product and up to the stage of securing orders.

What is Distribution Overhead? Distribution overhead is the expenses incurred in connection with the execution of an order. It begins with making the packed product available for dispatch and ends with making the reconditioned empty package, if any, available for re-use.

The various items included in manufacturing administrative, selling and distribution costs ate available in Table:

Functional Classification of Costs – Table.

Research and development costs:

Research cost is the cost of searching for new or improved products or methods. It comprises wages and salaries of research staff, payments to outside research organizations, materials used in laboratories and research departments, etc. After completion of research, the management may decide to produce a new improved product or to employ a new or improved method.

Development cost is the cost of the process which begins with the implementation of the decision to produce a new product or to employ a new or improved method and ends with the commencement of formal production of that product or by that method. Pre-production cost is that part of the development cost which incurs in making in trial production run preliminary to formal production.

Top 17 Cost concepts in Cost accounting:They are; 1) Product and period costs, 2) Common and joint costs, 3) Short-run and long-run costs, 4) Past and future costs, 5) Controllable and non-controllable costs, 6) Replacement and Historical Costs, 7) Escapable and unavoidable costs, 8) Out of pocket and Book Costs, 9) Imputed and Sunk Costs, 10) Relevant and Irrelevant Costs, 11) Opportunity and Incremental Costs, 12) Conversion cost, 13) Committed cost, 14) Shutdown and Abandonment costs, 15) Urgent and Postponable costs, 16) Marginal cost, and 17) Notional cost.

Here are important topic or questions is Discussion; What is the Cost concepts in Cost accounting?

A clear understanding of various cost concepts is essential for the study of cost accounting and cost systems.

Top 17 Cost concepts in Cost accounting – List

The description of these cost concepts follows now for cost accounting.

1] Product and period costs:

First Cost concepts; The product cost is the aggregate of costs that are associated with a unit of product. Such Costs may or may not include an element of overheads depending upon the type of costing system in force-absorption or direct. Product costs are related to goods produce or purchase for resale and are initially identifying as part of the inventory.

These products or inventory costs become expenses in the form of the cost of goods sold only when the inventory sales. Product cost associated with the unit of output. The costs of inputs informing the product viz., the direct material, direct labor, factory overhead constitute the product costs. The period cost is a cost that tends to be unaffecting by changes in the level of activity during a given period. What is the importance of Cost accounting?

The period cost associative with a period rather than manufacturing activity and these costs deduct as expenses during. The current period without have been previously classifying as product costs. Selling and distribution costs are period costs and are deducting from the revenue without their existence regard as part of the inventory cost.

2] Common and joint costs:

The common cost is an indirect cost that incurs for the general benefit of several departments or for the whole enterprise and which is necessary for present and future operations. The joint costs are the cost of either a single process or a series of processes. That simultaneously produce two or more products of significant relative sales value.

3] Short-run and long-run costs:

The short-run costs are costs that vary with the output when fixed plant and capital equipment remain the same and become relevant. When a firm has to decide whether or not to produce more in the immediate future. The long-run-costs are those which vary with the output when all input factors including plant and equipment vary and become relevant. When the firm has to decide whether to set up a new plant or to expand the existing one.

The past costs are actual costs incur in the past and are generally containing in the financial accounts. These costs report past events and the time lag between event and its reporting makes the information out of date and irrelevant for decision-making.

These costs will just act as a guide for the future course of action. The future costs are costs expecting to incur at a later date and are the only costs that matter for managerial decisions because they are subject to management control.

Future costs are relevant for managerial decision making in cost control, profit projections, appraisal of capital expenditure, the introduction of new products, expansion programs, and pricing, etc.

5] Controllable and non-controllable costs:

The concept of responsibility accounting leads directly to the classification of costs as controllable or uncontrollable. The controllable cost is a cost chargeable to a budget or cost center. Which can influence the actions of the person in whom control the center vests? It is always not possible to predetermine responsibility, because the reason for deviation from expected performance may only become evident later.

For example, excessive scrap may arise from inadequate supervision or latent defect in purchased material. The controllable cost is a cost that can influence and regulate during a given period by the actions of a particular individual within an organization. The controllability of cost depends upon the level of responsibility under consideration.

Direct costs are generally controllable by shop level management. The uncontrollable cost is a cost that is beyond the control of a given individual during a given period. The distinction between controllable and uncontrollable costs are not very sharp and may be left to individual judgment. Some expenditure which may uncontrollably on a short-term basis controllably on a long-term basis,

There are certain costs which are difficult to control due to the following reasons.

Physical hazards arising due to flood, fire, strike, lockout, etc.

Economic risks such as increased competition, change in fashion or model, higher prices of inputs, import restrictions, etc.

Political risks like change in Government policy, political unrest, war, etc.

Technological risk such as a change in design, know-how, etc.

6] Replacement and Historical Costs:

The Replacement costs and Historical costs are two methods for carrying assets in the balance sheet and establishing the amounts of costs that use to determine income.

The Replacement cost is a cost at which material identical to that is to replace could purchase at the date of valuation (as distinct, from actual cost price at the date of purchase). The replacement cost is the cost of replacing an asset at any allow point of time either present or the future (excluding any element attributable to improvement).

The Historical cost is the actual cost, determined after the event. Historical cost valuation states the costs of plant and materials, for example, at the price originally paid for them whereas replacement cost valuation states the costs at prices that would have to pay currently.

Costs reported by conventional financial accounts are based on historical valuations. But during periods of changing price level, historical costs may not be the correct basis for projecting future costs. Naturally historical costs must adjust to reflect current or future price levels.

7] Escapable and unavoidable costs:

The Escapable cost is an avoidable cost that will not incur if an activity does not undertakes or discontinue. The avoidable cost will often correspond-with variable costs. The avoidable cost can identify with an activity or sector of a business and which would avoid if that activity or sector did not exist. The escapable costs refer to costs that can reduce due to the contraction in the activities of a business enterprise. It is the net effect on costs that is important, not just the costs directly avoidable by the contraction. Examples:

Closing an unprofitable branch house-storage costs of other branches and transportation charges would increase.

Reducing credit sales costs estimated may be less than the benefits otherwise available.

Note: Escapable costs are different from controllable and discretionary costs.

8] Out of pocket and Book Costs:

The out of pocket cost is a cost that will necessitate a corresponding outflow of cash. Also, the costs involving cash outlay or payment to other parties term as out of pocket costs. Book costs are those which do not require current cash payments.

Depreciation is a notional cost in which no cash transaction involves. The distinction between out of pocket costs and book costs primarily shows how costs affect the cash position.

Out of pocket costs are relevant in some decision-making problems. Such as the fluctuation of prices during the recession, make or buy decisions, etc. Book-costs can convert into out of pocket costs by selling the assets and having the item on hire. Rent would then replace depreciation and interest.

9] Imputed and Sunk Costs:

The imputed cost is a cost that does not involve actual cash outlay. Which uses only for decision making and performance evaluation. Imputed cost is a hypothetical cost from financial accounting. Interest on capital is a common type of imputed cost. No actual payment of interest makes but the basic concept is that had the funds been investing elsewhere they would have to earn interest. Thus, imputed costs are a type of opportunity costs.

The Sunk costs are those costs that have been investing in a project and which will not recover if the project terminates. The sunk cost is one for which the expenditure has to take place in the past. This cost does not affect a particular decision under consideration. Sunk costs are always results of decisions accept in the past.

This, the cost cannot change by any decision in the future. Investment in plant and machinery as soon as it installs its cost is sunk cost and is not relevant for decisions. Amortization of past expenses e.g. depreciation is sunk cost. Sunk, costs will remain the same irrespective of the alternative selected.

Thus, it need not consider by the management in evaluating the alternatives as it is common to all of them. It is important to observe that an unavoidable cost may not be a sunk cost. The Managing Director’s salary is generally unavoidable and also out of pocket but not sunk cost.

10] Relevant and Irrelevant Costs:

The relevant cost is a cost appropriate in aiding to make specific management decisions. Business decisions involve planning for the future and consideration of several alternative courses of action. In this process, the costs which are affecting by the decisions are future costs. Such costs call relevant costs because they are pertinent to the decisions in hand. The cost is saying to be relevant if it helps the manager in taking. The right decision in furtherance of the company’s objectives.

11] Opportunity and Incremental Costs:

The opportunity cost is the value of a benefit sacrifice in favor of an alternative course of action. It is the maximum amount that could obtain at any given point of time. If a resource was selling or put to the most valuable alternative use that would be practicable.

The opportunity cost of a good or service measure in terms of revenue. Which could have been earning by employing that good or service in some other alternative uses. Opportunity cost can define as the revenue forgone by not making the best alternative use. Opportunity cost is the prospective change in cost following the adoption of an alternative machine process, raw materials, etc. It is the cost of opportunity lost by the diversion of an input factor from use to another.

The incremental cost is the extra cost of taking one course of action rather than another. It also calls at different costs. The incremental cost is the additional cost due to a change in the level of nature of the business activity.

The change may take several forms e.g., changing the channel of distribution, adding a new machine, replacing a machine by a better machine, execution of export orders, etc. Incremental costs will be different in case of different alternatives. Hence, incremental costs are relevant to the management in the analysis of decision making.

12] Conversion cost:

The conversion cost is the cost incur for converting the raw material into the finished product. It refers to as the production cost excluding the cost of direct materials:

13] Committed cost:

The committed cost is a cost that primarily associates with maintaining the organization’s legal and physical existence over which management has little discretion. Also, the committed cost a fixed cost that results from the froth decision of the prior period.

The amount of committed cost as fixed by decisions. Which makes in the past and not subject to managerial control in the short-run? Since committed cost does not fluctuate with volume and remains unchanged until action takes to increase or reduce available capacity.

Committed cost does not present any problem in cost behavior analysis. Examples of committed costs are depreciation, insurance premium, rent, etc. This is an important Cost concept in accounting.

14] Shutdown and Abandonment costs:

The shutdown costs are the cost incur about the temporary closing of a department/division/enterprise. Such costs include those of closing as well as those of re-opening. Also, the shutdown costs asses as those costs which would incur in the event of suspension of the plant operation. And, which would save if the operations are continuing. Examples of such costs are the costs of sheltering the plant and equipment and construction of sheds for storing exposed property.

Further, additional expenses may have to incur when operations are restoring e.g.. Re-employment of workers may involve the cost of recruitment and training. The Abandonment cost is the cost incur in closing down. Also, A department or a division or in withdrawing a product or ceasing to operate in a particular sales territory etc.. The abandonment costs are the cost of retiring altogether a plant from service; Abandonment arises when there is a complete cessation of activities and creates a problem as to the disposal of assets.

15] Urgent and Postponable costs:

The urgent costs are those which must incur to continue operations of the firm. For example, the cost of material and labor must incur if production is to take place. The Postponable cost is that cost which can shift to the future with little or no effect on the efficiency of current operations. These costs can postpone at least for some time, e.g., maintenance relating to building and machinery.

16] Marginal cost:

The marginal cost is the variable cost of one unit of a product or a service i.e., a cost that would avoid. If the unit did not produce or provide. In this context, a unit in usually either a single article or a standard measure such as a liter or kilogram. But may in certain circumstances be an operation, process or part of an organization.

They are the amount at any allow volume of output by which aggregate costs are changing. If the volume of output increases or decreases by one unit. It uses full Cost concepts in accounting.

The marginal costing technique is the process of ascertaining marginal costs and of the effects of changes in the volume of the type of output on profit by differentiating between fixed and variable costs.

17] Notional cost:

Final Cost concepts; The Constitutional or notional cost is hypothetical to take into account in a particular situation to re-present. As well as, the benefits enjoying by an entity in respect of which no actual expense incurs. Maybe you understand your misinformation of the cost concepts in cost accounting.

What is the Cost concepts in Cost accounting? Discussion.

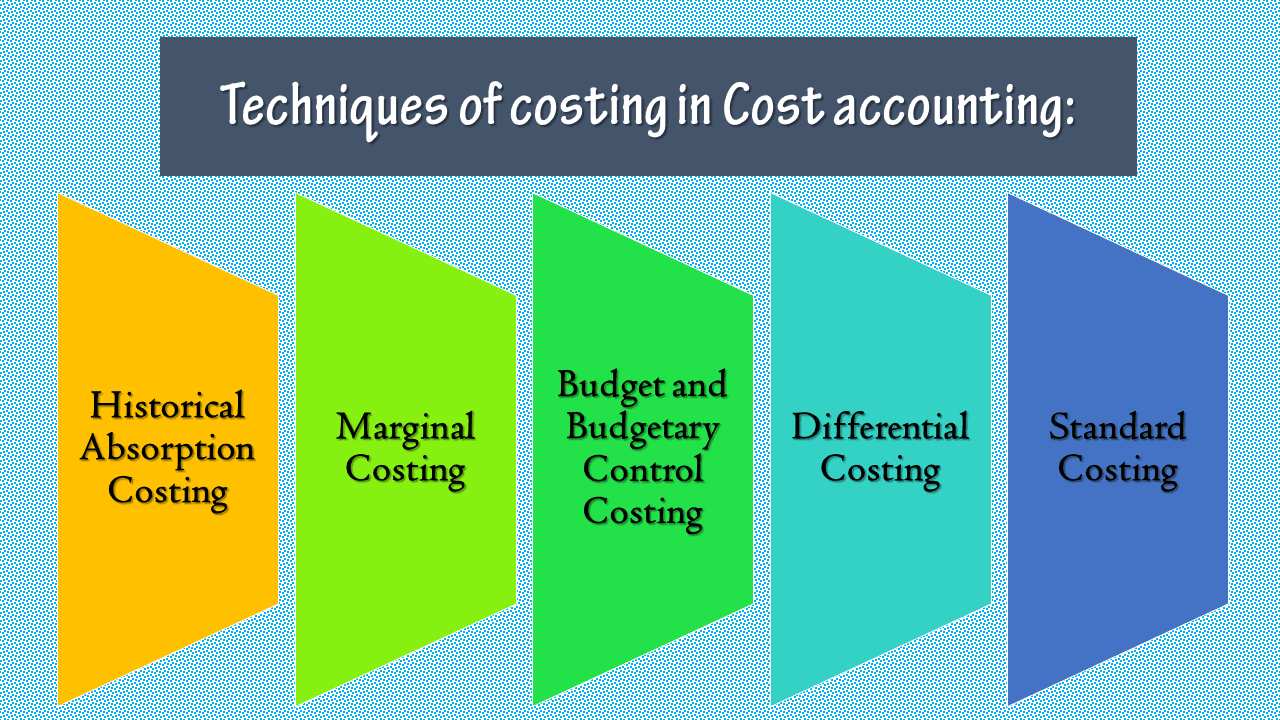

The techniques and methods of costing in Cost accounting are to explain their points one by one. First, Techniques of Costing:Historical Absorption, Marginal, Budget and Budgetary Control, Differential, and Standard Costing. As well as Methods of Costing: There are two methods of costing, namely; Job costing and Process costing.

What are the techniques and methods of costing in Cost accounting? Discussion.

In addition to the different costing methods, various techniques are also using to find the costs.

It’s the ascertainment of costs after they have been incurring. It defines as the practice of charging all costs, both variable and fixed, to operations, process or products. It also knows as traditional costing. Its ascertainment of costs after they have been incurring. It aims at ascertaining costs incurred on work done in the past.

It has a limited utility, though comparisons of costs over different periods may yield good results. Since costs are ascertaining after they have been incurring, it does not help in exercising control over costs. However, It is useful in submitting tenders, preparing job estimates, etc.

2] Marginal Costing:

It refers to the ascertainment of costs by differentiating between fixed costs and variable costs. In this technique, fixed costs are not treated as product costs. They are recovering from the contribution (the difference between sales and variable cost of sales).

The marginal or variable cost of sales includes direct material, direct wages, direct expenses, and variable overhead. It is the ascertainment of marginal cost by differentiating between fixed and variable costs.