The Account is the art of conveying financial information about a business unit for shareholders and managers etc. Accountancy has call ‘business language’. In Hindi, the words ‘लेखा विधि’ (account law) and ‘लेखाकर्म’ (accounting) are also useful in ‘Accountancy’. Accounting Content, Financial, and Accountancy!

Also learn, Accountancy is a branch of mathematical science that is useful in finding out the reasons for success and failure in business. The principles of accountancy are applicable to business units on three divisions of practical arts, namely, accounting, bookkeeping, and auditing.

As Well as the definition “Accountancy refers to the art of writing business practices in a scientific manner and classifying articles and preparing summaries and interpreting the results.”

The functioning of Accountancy is to provide quantitative information regarding economic units, which are basically financially inadequate. Which is useful in taking financial decision-making, accountancy, identifying, and measuring. Analyzing information relevant to an economic event of an organization There is a process for doing and collecting. Which is used to prompt users of this information.

Personal Loan: A good interest rate can be said to be one that is lower than your national average. A lot of factors go into play to decide the best interest rate offers for you. In general, the rates can vary from 9% to 36%. However, interest is not the only factor that you should be concerned about when looking for a personal loan. There’s more that you have to see and understand! Let’s take a look!

What Influences Personal Loan Interest Rates?

Personal loans are known as unsecured loans as there’s no collateral to back them up. This is one of the reasons why the interest rates may go high for a personal loan. At times, in the personal loan, you may also come across the term, “annual percentage rate”, which stands for the extra loan costs other than the principal balance. This number reflects the amount that you are going to submit with your interest.

The personal loan interest rates highly depend upon the credit score. The higher the credit score is, the lesser will be the interest rates. If you have a record of on-time payments, then your credit score will go high, ultimately lowering down the interest rate. In short, the higher the interest rate, the lesser will be the interest rate of your personal loan. Also, don’t forget about the debt-to-income ratio. In this case, the lower the DTI is, the lower would be the interest rate.

In case, you aren’t able to grab the lower interest rates, then you may apply with a potential co-applicant. The lender will go through the co-applicants repayment ability, annual income, DTI, etc. to determine the interest rate. Don’t forget that your co-applicant would be equally responsible for the repayment of the loan, in case you aren’t able to meet the deadlines.

How Personal Loans May Affect The Credit Score?

It’s important to look around for the lowest interest rate; however, the submission of applications to various lenders may bring a slight hit on your credit score. The best way to exclude multiple hard inquiries is through performing a comparison shop, within a short while, as that will lower down the impact. If within a matter of a few weeks only, the various hard inquiries occur, then some credit score models may count them as single events only.

If you are lucky, then you may get pre-approval; and, that may lead to very few inquiries, or in short, the process ends up becoming a lot easier. If you make a habit of making on-time payments for your personal loans then it can even improve the whole credit score. Though, if you fail to meet the deadlines, then the sweet credit score is definitely going to see a drop.

Factors to Look For When Considering Offers:

They below are;

Fees:

Get to know about any and every kind of feed that’s out there. Find out how many fees the lender is going to charge in the name of prepayment penalties, late fees, origination fees for clearing the loan early.

Loan Term:

It’s basically how much duration or payment installments is going to take to clear off the loan amount. It’s simple, the shorter the period or installments are, the cheaper the APR will be.

Monthly Payment:

What’s your monthly salary? Will you be able to afford the monthly payments, and even meet the other debts, and necessary expenses?

Discounts Available:

If you take a loan from a financial institution where you already have an account, then you may expect the rate to go down.

Conclusion:

It’s essential to know the personal loan interest rates before applying for a loan, and that’s why we recommend you to spend enough time among the lenders so that you can perform a good comparative analysis. More than knowing the interest rates that fit their credit profile, one must first ascertain whether or not they will be able to catch up with the monthly payments of the personal loan. Lastly, we just want to say that play with a personal loan in such a manner, so that there’s enough room for other financial needs that you may have to take in the future.

Ledger Merchant Account: The ledger system of double-entry bookkeeping includes the utilization of various record administered books (known as a bunch of books) to record exact data, in cash esteems, of every day exchanging activities of a business. Accounting essay present; Ledger Account is a diary where an organization keeps up the information of the relative multitude of exchanges and fiscal summary. The organization’s overall cartulary account coordinate under the overall cartulary with the monetary record grouped into various records like resources, Accounts receivable, creditor liability, investors, liabilities, values, incomes, charges, costs, benefit, misfortune, reserves, advances, bonds, stocks, compensations, compensation, and so forth.

Ledger Merchant Account: Meaning, Definition, Types, Features, Advantages, and Disadvantages.

Before understanding What ledger accounts are? Let us take a concise prologue to Ledger. Diary is utilized to record the exchanges sequentially. Yet, Journal just gives the impact of individual exchanges. The proprietor of a business, in any case, isn’t just keen on thinking about the impacts of individual exchanges on fiscal summaries yet also the gathered impact of each Account.

For instance, if he needs to know the aggregate sum of buys identifying with a specific bookkeeping period, at that point it will be a chaotic task to discover it from the Journal as it contains countless exchanges identifying with buys at better places as indicated by their particular dates of the event. In any case, he can without much of a stretch locate the number of all-out buys from the “Buys Account”. Subsequently, it requires that exchanges of a comparative sort should figure out and collected in one spot. This spot is a cartulary.

Meaning of Ledger Merchant Account:

What Does Accounting Ledger Mean? The notes or diary gives a total posting of the everyday exchanges of a business. Be that as it may, it doesn’t give data about a particular record in one spot. For instance, to realize how much money balance we have, the bookkeeping agent would need to check all the diary sections in which money includes, and this is an arduous work; because there are hundreds or even great many money exchanges recorded on various pages of the diary. To dodge this trouble, the charge and credit of journalized exchanges move to ledger accounts. Hence all the progressions for a solitary record are situated in one spot – in a cartulary account. This makes it simple to decide the current equilibrium of any record.

At the point when all the exchanges of a given period have been journalized, the following thing is to characterize them as per the records influenced. All comparative exchanges must unite. For example, all exchanges identifying with money must place in one spot. Likewise, all exchanges with a client or a provider must collect in one spot. The book in which this characterization do know as the ledger.

Definition of Ledger Merchant Account:

What is the Ledger in Business? The cartulary is a book that contains a consolidated and arranged record of the relative multitude of financial exchanges of the business by and large brought, moved, or posted from the books of unique section.

The cartulary knows as the ruler of all books of records since all sections from the books of unique passage must present on the different records in the ledger. It should notice that the diary contains a sequential record while the cartulary contains an ordered record, all things considered.

Kinds of Types of Ledger Merchant Account:

A cartulary is where all ledger accounts are kept up in a summed up manner. What are 3 different types of Ledger double entry? All records joined to make a cartulary book. A cartulary otherwise calls the chief book of records and it shapes a perpetual record of all business exchanges. Prevalently there are 3 unique types of the ledger – Sales, Purchase, and General ledger.

Sales Ledger or Debtor’s Ledger:

Deals or Sales Ledger is a cartulary where the organization keeps up the exchange of selling the items, administrations, or cost of merchandise offered to clients. This cartulary gives the possibility of deals with income and pays explanation. First among various sorts of ledgers is “Deals or Debtors’ ledger”.

It is a gathering of all records identified with clients to whom products have been sold using a loan (Credit Sales). The Sum of all the cash owed to a business by their clients appears here and name as Accounts Receivable, Trade Debtors, or Sundry Debtors. The records generally organize in sequential requests, be that as it may, these days all the cartulary accounts are kept up with the assistance of bookkeeping ERPs.

Purchase Ledger or Creditor’s Ledger:

Purchase or Buy Ledger is a cartulary where the organization puts together the exchange of buying the administrations, items, or products from different organizations. It gives the permeability of how much sum the organization paid to different organizations. It is a gathering of all records identified with vendors from whom products have been bought using a loan (Credit Purchases).

The Sum of all the cash owed by a business to their merchants is appeared here and name as Accounts Payable, Trade Creditors, or Sundry Creditors. The all-out money related sum inside the bought cartulary appears in the preliminary equilibrium and the asset report at its fitting spot.

General Ledger:

General Ledger isolates into two kinds – Nominal and Private Ledger. An ostensible cartulary gives data on costs, pay, deterioration, protection, and so on Also, a Private ledger gives private data like compensations, compensation, capitals, and so on Private ledger isn’t open to everybody. Organizations typically make a solitary general ledger which incorporates 2 extra subtypes of ledgers for example ostensible and private ledger.

These two might remember for the rundown for various sorts of ledgers in bookkeeping. An overall cartulary is a brought together gathering for all the cartulary records of a business. It contains a wide range of records which can find in an association; for example, resources, liabilities, capital or value, incomes, costs, and so forth

According to conventional or UK style bookkeeping; It comprises of all ostensible and genuine records important to plan financials for an organization. For example Building, Office hardware, Furniture, etc.

Nominal Ledger: As the name recommends it contains all ostensible records for example cost, misfortunes, wages, and gains. Models – Salaries, Sales, Purchases, Returns Inward/Outward, Rent, Stationery, Insurance, Depreciation, and so on

Private Ledger: They comprise records that are secret in nature, for example; capital, drawings, compensations, and so forth These records are just available by chosen people.

A few organizations do make separate general, ostensible, and private ledger.

Features or highlights or characteristics of Ledger Merchant Account:

The ledger has the following main characteristics or features:

It has two indistinguishable sides – the left-hand side (charge side) and the right-hand side (credit side).

The charge part of the relative multitude of exchanges record on the charge side; and, credit parts of the relative multitude of exchanges record on the credit side as per date.

The contrast between the sums of the different sides speaks to adjust. The overabundance of the charge side over the credit side demonstrates charge balance; while an abundance of the credit side over the charge side shows the credit balance. On the off chance that the different sides are equivalent, there will be no equilibrium.

For the most part, the equilibrium draws at the year-end; and, recorded on the lesser side to make the equivalent of the different side. This equilibrium knows as the end balance.

The end equilibrium of the current year turns into the initial equilibrium of the following year.

Ledger Merchant Account: Meaning, Advantages, and Features; Image from Pixabay.

Merits or Benefits or Advantages of Ledger Merchant Account:

What are the advantages of Ledger double entry? Keeping up the ledger is an unquestionable requirement in each bookkeeping framework. It is important as will be obvious from its preferences.

Exchanges identifying with a specific individual, thing, or heading of use or pay to assemble in the concern record in one spot.

At the point when each record occasionally adjusts it mirrors the net situation of that account.

Ledger is the venturing stone for getting ready Trial Balance – which tests the arithmetical exactness of the bookkeeping books.

Since the sections recorded in the diary refer to in the cartulary the chance of mistakes of defalcations decreases to the base.

Ledger is the objective of all sections made in diary or sub-diaries.

Ledger is the “storage facility” of all data which consequently utilize for getting ready last records and fiscal summaries.

The accompanying focuses feature the best eight focal points of a ledger. The points of interest are:

The readiness of Trial Balance:

It is preposterous to expect to set up a Trial Balance without ledgers. Since a Trial Balance sees up by taking up the cartulary accounts balance. Besides, arithmetical precision is unimaginable.

Twofold Entry System finishes just when we present the diaries on various cartulary accounts.

Deciding Results of Each Account:

The consequences of each record can get from the cartulary dependent on Double Entry standards.

Keeping up Classified Accounts Indirect Advantages:

The points of interest of grouped records might uncover in the wake of recording in the cartulary account appropriately.

Introducing Statistical Information:

The cartulary accounts with their separate adjust are the wellsprings of measurable data that utilize by the administration while dynamic.

Gathering Information:

The cartulary might know as the assortment or storeroom of different exchanges.

Present Financial Position:

The monetary situation of an endeavor (i.e., after setting up the last record) must know whether we keep up the cartulary account appropriately.

Demerits or Limitations or Disadvantages of Ledger Merchant Account:

As Merchant Account Keeping up the ledger is an unquestionable requirement in each bookkeeping framework. Its disadvantages will be obvious from its preferences;

Ledger is dependent on the journal entry, they are not working independently. It is fully helpless without journal data.

They are not opening entry while closing entry, and also they analyze from the fixed data record.

Ledger is a system of double-entry bookkeeping; but, some data is both side columns belong as cash or bank or name is all depend on credit or debit entry.

Copy Book or Journal: In Accounting Essay – The word journal has been gotten from the French word “Jour” Jour implies a day. Along these lines, the journal implies every day. Journal in records book names as the book of the original passage. It knows as the book of the original section since, in such a case that any monetary exchange happens, the bookkeeper of an organization would initially record the exchange in the Daybook. That is the reason a journal in bookkeeping is basic for anybody to comprehend. Regardless of what your identity is, an eventual bookkeeper, an account devotee, or an investor who might want to comprehend the characteristic exchanges of an organization, you have to realize how to pass a Daybook passage before whatever else.

Copy Book or Journal: Meaning, Definition, Types, Features or Characteristics, Advantages or Benefits, and Limitations or Disadvantages.

Exchanges record day by day in a Day book and thus it has named so. When an exchange happens its charge and credit perspectives are investigated and above all else, recorded sequentially (in the order of their event) in a book along with its short portrayal. This book knows as a Daybook. Thus we see that the main capacity of a journal is to show the connection between the two records associated with an exchange. This encourages the composition of a record. Since exchanges are first of all recorded in quite a while, so it knows as the book of original passage or prime section or essential passage or starter passage, or first passage. Accounting Essays;

Meaning and Definition of Copy Book or Journal:

Which means and definition of Journal; Journal is the book of an original section wherein, in the wake of adhering to the guidelines of charge and credit, all business exchanges record in sequential order. Hence, a Daybook implies a book that records all financial exchanges of a business on a regular schedule. The money-related exchanges record in sequential order i.e., in the order of their event.

As the recording of exchanges is done first in the journal, it likewise calls the book of original passage or a prime section. Journalizing characterizes as the way toward recording exchanges in the Daybook. In the wake of deciding the specific record to charge and credit, every exchange independently record.

A journal might characterize as the book of the original or prime section containing a sequential record of the exchanges from which presenting is done on the record. The exchanges record first in the Daybook in the order in which they happen. In the bookkeeping world, Journal alludes to a book wherein exchanges are logged for the absolute first time, and that is the reason it additionally calls as “Book of Original Entry”. In this book, all the ordinary business exchanges enter consecutively, for example, when they emerge.

From that point forward, the exchanges are presented on the Ledger, in the concerned records. At the point when the exchanges record in the journal, they call Journal Entries. According to the Double Entry System of Book Keeping, each exchange influences different sides, for example, charge and credit. Thus, the exchanges enter in the book according to the Golden Rules of Accounting, to realize which record is to charge and which one is to credit.

Types of Copy Book or Journal:

There are two types of the journal:

General Journal:

General Journal is one in which a small business entity records all the day to day business transactions

Special Journal:

In the case of big business houses, the journal classifies into different books called special Day books. Transactions record in these special Day books based on their nature. These books also know as subsidiary books. It includes cash book, purchase day book, sales day book, bills receivable book, bills payable book, return inward book, return outward book, and journal proper.

The Daybook proper uses for entering infrequent transactions such as opening entries, closing entries, and rectification entries.

Characteristics or Highlights or Features of Copy Book or Journal in Accounting:

The first step of the accounting process is to maintain a journal or journalizing of transactions. Journal has the following features:

Journal is the main effective advance of the twofold section framework. An exchange records most importantly in the journal. So the Daybook knows as the book of the original section.

An exchange record around the same time it happens. Along these lines, the journal calls Day Book.

Exchanges record sequentially, So, the journal knows as an ordered book

For every exchange, the names of the two concerned records demonstrating which charges and which credits, are obviously written in two back to back lines. This makes record posting simple. That is the reason the Day Book designates “Partner to Ledger” or “auxiliary book”

The portrayal composes beneath every section.

The sum writes in the last two segments – the charge sum in the charge section and the credit sum in the credit segment.

From the definitions and its recording procedures, the following features of the journal mark:

Book of essential passage:

The primary phase of the bookkeeping cycle is to keep up a Day Book. Exchanges first record in the Daybook. That is the reason the Day Book knows as the fundamental book of records.

Day by day record book:

Not long after the event and recognizable proof of exchanges, these record in the Day Book in sequential order of dates. Since exchanges record on the day co-event in the Day Book, it knows as a day by a daily record book.

Sequential order:

Everyday exchanges record in a Day Book in sequential order of dates. For this explanation, the Daybook likewise calls an order book of records.

Utilization of double parts of exchanges:

According to the standards of the twofold passage framework, each exchange records in a Daybook in double viewpoints, for example, charging one record and crediting the other record.

Utilization of clarification:

Journal passage of each exchange trails by clarification or portrayal since clarifications of sections fill the need for future reference.

Various segments:

Each page of the journal separates into five segments: Date, account titles and clarification, record folio, charge cash section, and credit cash segment.

An equivalent measure of cash:

For the journal section of every exchange, a similar measure of cash writes in charge of cash and credit cash segments.

Auxiliary book:

Journalizing the exchange helps the planning of the record helpfully. That is the reason the Day Book knows as an auxiliary book to the record.

Utilization of various journal books:

Journal implies a general daybook. Be that as it may, considering size-nature and volume of exchanges daybooks sub-separate into numerous classes. For instance; Purchase daybook deals daybook, buy return daybook, deals return daybook, money receipt Journal, money payment daybook dry daybook appropriate. The employments of the Day Book resolve thinking about the need of the organization.

Copy Book or Journal: Meaning, Advantages, and Futures; Image from Pixabay.

The Utility or Advantages or Benefits of the Copy Book or Journal:

The following advantages or benefits below are;

An essential book of the original section:

As the principal recording of exchange is done in the daybook, it knows as the book of the original section or prime passage. All business exchanges first discover a spot in quite a while and afterward, just the record in isolated record accounts.

A central book following the twofold passage bookkeeping:

In the wake of deciding the specific record to charge and credit, every exchange independently record. If we don’t open daybooks in an endeavor, the odds of keeping up books of records, according to the standards of the twofold section framework are far off.

Exchanges in sequential order:

All the exchanges record in the daybook in sequential order. In this way, the odds of discarding any exchanges in the books of records are dainty.

Complete information about business exchanges:

All journal passages support with brief portrayals. These portrayals help to comprehend the importance and motivation behind the exchange in future dates.

Grouping of all exchanges gets simpler:

All journal passages depend on vouchers and record in the journal as and when they happen. Thus, the exchanges are ordering immediately when they happen.

Aides in the division of labor:

In a huge business, a journal sub-separate into more than one. This sub-division assists with recording one sort of exchange in that book. For instance, deals book records just credit deals and buy book records just credit buys. These sub-journals took care of and constrained by various and separate people. In such cases, normally, that individual procures ability which causes the endeavor to accomplish its shared objective productively and adequately.

Guarantees arithmetical precision:

In the journal, the complete of the charge segment and credit segment should coordinate and concur. The difference is a speedy sign of the responsibility of certain errors, which can handily recognize and amended.

Limitations or disadvantages of Copy Book or Journal:

The following disadvantages or limitations below are;

Massive and voluminous:

Journal is the principal book of original passage which records all business exchanges. Now and again, it turns out to be so cumbersome and voluminous that it can’t be taken care of without any problem.

Information in the dispersed form:

In this book, all information records in routine and dispersed form; thus it is hard to find a specific exchange except if one recollects the date of the event of that exchange.

Tedious:

In contrast to posting from auxiliary books, posting the exchanges from daybook to record accounts take an excessive amount of time because each time one needs to post the exchanges in various record accounts.

Absence of interior control:

Dissimilar to different books of original sections like auxiliary books and money books, the daybook doesn’t encourage inner control, because the journal just exchanges record in sequential order. Be that as it may, auxiliary books and money book gives an away from of the unique sort of exchanges recorded in that.

Balance Sheet: The accounting essay on the meaning and significance of the balance sheet is an announcement of the resources, capital, and liabilities of the business. It is the announcement, which portrays the monetary situation of the business on a specific date. This note has data about the balance sheet. It’s anything but a record rather than a fiscal summary. It presents the risk on the left-hand side and the resources on its right-hand side either arranged by changelessness or request of liquidity.

Here are the articles of Balance Sheet: meaning, definition, objectives, advantages or benefits, and limitations or disadvantages.

What is the balance sheet in Accounting? A balance sheet is an announcement arranged to know the monetary situation of a business association on a given date. It is a mirror that mirrors the genuine situation of the resources and liabilities on points of interest date. So balance sheets otherwise called proclamations of monetary position. It gets ready toward the finish of a bookkeeping period and after finishing the arrangement of exchanging and benefit and misfortune account.

Definition of Balance Sheet:

A balance sheet is an announcement drawn up toward the finish of each exchanging period expressing in that all the resources and liabilities of a business organized in the standard request to display the valid and right situation of the worry as on a given date. A balance sheet is set up from a preliminary balance after the balances of ostensible records are moved to the exchanging account or the benefit and misfortune account.

The rest of the balances of individual or genuine records speak to either resources or liabilities at the end date. These resources and liabilities are appeared yet to be a determined sheet in an ordered structure; the resources are shown on the correct side and the liabilities on the left-hand side.

The accompanying fundamental definitions of the balance sheet underneath are;

According to Palmer;

“Balance sheet is a statement of a particular date showing on one side the trader’s property and on the other side, the liabilities.”

According to AICPA;

“Balance sheet is a list of balances in the assets and liabilities accounts. The list depicts the position of assets and liabilities of a specific business at a specific point of time.”

The Committee on Terminology of the American Institute of Certified Public Accountants defines the balance sheet as;

“A list of balances in the assets and liability accounts. This list depicts the position of assets and liabilities of a specific business at a specific point of time.”

Purpose or Objectives of the Balance Sheet:

The main purpose or objectives of preparing a balance sheet can describe as follows below are:

To Reveal The Financial Position; The main purpose of preparing a balance sheet is to know the short term and long term financial position of the firm.

To show the profitability of Assets and Liabilities; Balance prepares to know the value of assets and liabilities of the company at the end of the year.

Information about Debtors And Creditors; The balance sheet provides a true picture of trade debtors and creditors for a specific period.

To reveal Liquidity Position; The balance sheet shows the liquidity position of the firm.

To show Solvency Position; The balance sheet helps to know the solvency position of the business.

To Calculate Ratios; Accounting ratios are calculated based on data provided by the balance sheet. It helps the management to know the strength and weaknesses of the business.

To provide Financial Information; The balance sheet provides true and reliable financial information to the management, government, shareholders, lenders, etc.

Other Objectives:

Principal Objectives: The main purpose of preparing a balance sheet is to know the financial position of the business at a particular date.

Subsidiary Objectives: Though the main aim is to know the exact financial position of the firm at a particular date, yet it serves other purposes as well; 1] It gives information about the actual and real owner’s equity. Though the capital of the owner indicates the owner’s equity, yet some other liabilities are to account for against it also; 2] It helps the firm to make provisions against possible future losses. A provision makes in the form of the Reserves.

The advantages and favorable circumstances [benefits] of the balance sheet:

A balance sheet is a see in the current season of what organization resources, what its liabilities, and the investors’ enthusiasm for the organization investors’ on value. It utilizes inside to help deal with the business and remotely to report the organization’s money related condition. The upsides of the balance sheet include the significant data it passes on; notwithstanding, the utilization of obsolete qualities for specific resources is a significant weakness.

The accompanying 7 best advantages and preferences of the balance sheet beneath are;

Keeping Things in Balance:

The balance sheet condition shows that an organization’s resources equivalent to its liabilities in addition to its investors’ value. Since this condition should consistently hold, any deviation from it demonstrates a disappointment of the organization’s bookkeeping frameworks. The exceptionally organized arrangement of the balance sheet breaks the three significant parts into a progression of records with dollar esteems starting at a given date. In that capacity, it is a minimal, effectively comprehended the wellspring of current data, and it shows patterns when contrasted with past balance sheets.

Figuring and Analyzing Ratios:

One of the advantages of a balance sheet is that supervisors, speculators, moneylenders, and controllers take the proportion of an organization by figuring monetary proportions utilizing data from the balance sheet, frequently related to different reports, for example, the pay proclamation. For instance, balance sheet information uses to look at liquidity, which is the capacity of the organization to cover its present tabs, by separating current resources by current liabilities or the current proportions. Many balance sheet proportions help show how an organization thinks about its rivals and can help recognize significant money related patterns.

Acquiring Credit and Capital:

The significance of a balance sheet is likewise apparent should a business need to acquire credit extensions or advances. Before a loaning foundation will loan cash or stretch out credit extensions to another or set up a business, the moneylender will probably require a balance sheet to help Assess a business’ reliability and budgetary state. If your balance sheet is precise and cutting-edge, it will furnish the bank with an image of the business’ capacity to reimburse its obligation. Without a balance sheet, the bank by and large will require different records or deny the credit altogether.

Business Preview or Snapshot:

The Balance Sheet otherwise calls for the announcement of the budgetary position. It is the depiction of what business claims (for example resources) and what business owes (for example liabilities). The distinction between resources and liabilities is known as the total assets of the business. Total assets are additionally called investors’ value. Also, the Balance Sheet gives the data that proprietors need to know and exploit the equivalent. They help in the administration of working capital. It rattles off the current resources and the liabilities that the business owes that should be paid as of now. Working Capital Management makes it simpler by the handling of data on the Balance Sheet.

Assurance of Risk and Return:

The balance Sheet compartmentalizes itself into different parts among which short and long-haul resources and liabilities are significant ones. Current and Long-term resources mirror the capacity of the business to create free incomes and keep up the activities. Then again, short-and long haul obligation commitments give a birds-eye perspective on how a business ought to organize its budgetary commitments. To put it plainly, the balance sheet shows you the budgetary situation of the business.

Making sure about extra capital:

Moneylenders require a Balance Sheet to decide the monetary wellbeing and reliability of the business. Planned financial specialists investigate the balance sheet to comprehend where their cash will contribute and how they will reimburse. Also, Relative Balance Sheet more than scarcely any year viably shows the capacity of the business to gather installments from borrowers and reimburse obligations to loan bosses. The better the balance sheet, the better the possibility of getting higher financing. Also, the capacity to reimburse credits is straightforwardly identified with the nature of the balance sheet.

Money related Ratios as Silver Lining:

Money-related proportions infer by investigating the different segments of the balance sheet. Proportions utilize in the investigation of fiscal summaries to demonstrate the organization’s operational proficiency, liquidity, benefit, and dis-solvability. Budgetary proportions make it simpler to examinations the capital structure, stock cycle, and normal borrowers period in the event of reimbursement. On the off chance that the business is consistently adjusting the obligation; it views as incredible and there are budgetary proportions inferred to do likewise. This data distinguishes patterns after some time and permits the business to see the budgetary structure and operational proficiency of the business. Further, many balance sheet proportions are useful in contrasting the business with its immediate rivals.

Disadvantages [Hindrance] and limitations [restrictions] of the balance sheet:

The accompanying 6 best disadvantages or hindrances and restrictions or limitations of the balance sheet underneath are;

Misquoted Long-Term Assets:

Long haul resources require to last over one year and incorporate things like property, plant, and hardware. The balance sheet records the estimation of long haul resources at the cost paid for them, known as the verifiable or book esteem. One of the constraints of a balance sheet is that it overlooks the current estimation of these resources.

Devaluation lessens the estimation of long haul resources as indicated by a self-assertive timetable made for charge purposes yet doesn’t really reflect genuine mileage. Moreover, the balance sheet disregards any addition in esteem or the cash it would take to supplant a resource at current costs. Book worth can considerably downplay long haul resources, mutilating the abundance of the organization.

Missing Assets:

Just resources procured by exchanges wrote about the balance sheet. Along these lines, it discards some truly important resources that not exchange arrange and can’t communicate in money-related terms. For instance, an organization may have an exceptionally important gathering of specialized specialists that would be difficult to supplant yet not giving an account of the balance sheet. Also, resources grew inside, for example, an online web deals channel can have colossal worth that the balance sheet overlooks.

Valuation of Internally Generated Assets:

The significant restriction of the balance sheet is that lone obtained resources represent. Consequently, when the resources grew inside by experiencing innovative work works, these resources do not perceive at market esteem, maybe at a cost that will in general by and large lower over the worth or now and then higher than the market esteem. Assume, the business constructs the site and starts the online business. The balance sheet to a great extent overlooks the worth capacity of the expense of the site.

Mis-expressed Long-term resources:

Long haul resources require to last over one year and incorporate plant and apparatus, building, and so forth The Balance Sheet records the estimation of the resources at verifiable or book esteem. The devaluation that has been determined is for charge purposes or is dependably assessed according to acknowledged approaches. In any case, this doesn’t mirror the genuine mileage of resources. Also, the Balance Sheet likewise disregards the cash esteem that the business would need to supplant the resources being used.

For example, Machinery was bought in 2015 with an expected existence of 5 years. In 2019, the hardware records at an authentic cost less aggregated devaluation. On the off chance that the straight-line strategy utilizes, the apparatus would totally discount before the finish of the 2020 money-related year. This ought not to be the situation. Apparatus has market esteem which might be higher or lower than the recorded worth. Rescue worth can assess however once more, this isn’t a reality yet just dependent on certain bookkeeping strategies and suppositions.

Preview at a specific date:

As a balance sheet portrays a money-related situation as on a specific date; the administration or the proprietors need a balance sheet as sound as could reasonably be expected. Also, they would simply reimburse the bank obligation on the last date; thus, as to pay off the obligation as on that date. Organizations can control the money, borrowers, and leaser’s information to control loan specialists. For example, a high money balance toward the end date of the bookkeeping time frame ought to affirm solid liquidity holds. Be that as it may, the organization’s goal for the utilization of money can be unique. Consequently, at a given timeframe, the figures for the balance sheet can be misdirecting.

Needs Comparison:

To make total utilization of the apparent multitude of things yet to be a determined sheet; one must contrast the business balance sheet and that of contenders and their own balance sheet over the different bookkeeping time frames. It is, subsequently, a basic errand to make the correlation with bear the products of the balance sheet.

Balance Sheet: Meaning, Objectives, Advantages, and Limitations; Image from Pixabay.

Trading Account Essay [in Hindi]: The first step of the final account is a trading account. A trading account is a nominal account that prepares at the end of the accounting year. They help to find out gross profit or gross loss during the accounting period. The trading account consists of two sides “debit and credit”. All direct expenses are debited and direct incomes are credited in the trading account. The trading account contains mainly the purchase of goods, The sale of goods, and expenses relating to the daily operation of the factory.

Here are the essay and article of Trading Account: Meaning, Definition, Advantages, Disadvantages, Limitations, Needs & Importance, and Objectives.

What is the Trading Account in Accounting? The account prepares to know the gross profit or gross loss of a company concern calls a trading account. It should note that the report of the business determined through a trading account is not final. The true reports the net profit or the net loss which is determined through profit and loss account. It can calculate using the following formula;

After preparing the trial balance, the next step is to create a trading account; A trading accounts one of the financial statements that show the result of the purchase and sale of goods and services during the accounting period; The main purpose of preparing the trading accounts to find out the gross profit or gross loss during the accounting period; Gross profit is said to be when the goods sold have more income than sales.

Conversely, when sales proceeds are less than the cost of goods sold, there is a gross loss; to calculate the cost of goods sold, we have to take into account the direct expenditure on stock, purchase, purchase or manufacture of goods and closing of stock; The balance of this account i.e. gross profit or gross loss can mention on the profit and loss account in accounting.

Meaning and Definition of Trading Account in Accounting:

A business account is designed primarily to know the profitability of “goods” bought or manufactured and sold by businessmen; The difference between the selling price and cost price of goods is the gross result.

The term “consignment” means goods purchased for resale; It does not include property; If the sales proceeds exceed the cost of goods sold, then the gross profit made; If the amount sold is less than the cost of goods sold, a gross loss occurs.

After the Trading account, the Profit / Loss account can be prepared separately or they can be shown as an account in which Trading and Profit and Loss account is with two classes; The first part of this section which deals with the study of the result of trading transactions alone is known as a trading account. A trading account can define as an account that discloses the consequences of buying and selling goods.

Advantages of Trading Account in Accounting:

The following are the Major Benefits or Advantages below are;

It shows the relationship between gross profit and gross loss, sales that help to measure profitability or losses position.

The account shows the ratio between the cost of goods sold and gross profit.

They give information about the efficiency of trading activities.

They help to compare the cost of goods sold and gross profit.

It provides information regarding stock and the cost of goods sold.

The result of trading can know separately.

The various items of this account of different periods can compare.

The adjustment in the selling price can make by knowing the percentage of gross profit on net sales.

Over-stocking/under-stocking can know to act wisely.

If the gross loss discloses, the business can close immediately because the loss will further increase when the indirect and non-expenses add to it.

The progress can study based on the gross profit ratio, year after year.

Disadvantages and limitations of Trading Account in Accounting:

The following are the Major limitations or disadvantages below are;

It only defines the gross profit or gross loss, so this account can not result from net profits and net loss for the company; the company needs to make another account in accounting for net profits and net loss, it calls profit or loss account.

Its report can not share with the company shareholder.

They only mention direct expenses, not to indirect and non-expenses.

Needs & Importance of Trading Account in Accounting:

It is very important to want to know what is the gross profit or gross loss; for the company to also want to know whether purchasing goods, what manufacturing of goods and sales are sufficient for earning or not.

The following main needs and importance below are.

It helps to know gross profit or loss.

They provide information about direct expenses.

They provide safety against possibilities of loss.

It helps in comparison with closing stock with last year’s stock.

Trading Account: Meaning, Definition, Advantages, Disadvantages, Limitations, Needs & Importance, and Objectives; Image from Pixabay.

Objectives of preparing a Trading Account in Accounting:

What are the purpose or objectives of preparing a trading account in accounting for the business year? The profit or loss rated by trading accounts the gross result of the business but is not the net profit report. If so, then a question in mind why we need to prepare a trading account? So we got an answer; this account is necessary because we need to prepare a balance sheet for our company revenue and expense transaction; and, also need to know what gross & net profit.

First objectives:

The gross profit of a business is very important data since all business expenses are met out of it. So the amount of gross profit should be adequate to meet the indirect or non-expenses of a company’s concern.

The number of net sales can determine through this account. Gross sales can ascertain from the sales account in the ledger, but net sales cannot so obtain. The true sales of a business are net – not gross sales. Net sales determine by deducting sales returns from gross sales in the trading account.

The success or failure of a company can fixate by comparing net sales of the current year with that of the last year. It should note that an increase in the number of total sales of the current year over the last year may not observe as a sign of success, since sales may increase because of rising in the price level.

To Show Gross Profit and Loss; the Trading account determines gross profit and the gross loss of the business at the end of the period. For Net Purchase and Sales; the Trading account determines the amount of net purchase and sales during the accounting period. Cost of Good Sold; It calculates the cost of goods sold at the end of the period.

Second objectives:

The percentage of gross profit on net sales (gross profit ratio) can easily determine from the trading accounts. This percentage is a very important yardstick for measuring the success or failure of a business. Compared to last year, if the rate increases, it indicates success; on the other hand, if the rate decreases, it is an indication of failure.

The percentage of different items of buying expenses (direct expenses) on gross profit can easily determine and by comparing the percentage of the current year with that of the previous year the variations can be ascertained. An analysis of variances will disclose their cause which will help in controlling the number of expenses.

Inventory or stock turnover ratio can analyze from the trading account in accounting. The success or failure of a company can measure by this determination. A higher rate indicates a favorable sign i.e. goods sold soon after their purchase. On the other hand, a low rate of signifies deterioration, i.e. goods sold long after their purchase.

Fixation Of Price; They help to fix the selling price of the product by showing the relationship between sales and cost of goods sold. To Know Expenses; It helps to know the factory expenses. To Show Stock Position; They give detailed information about the stock position. The efficiency of Business; It helps to measure business efficiency by comparing sales and expenses.

Profit and Loss Account – P&L meaning, definition, and advantages. The company prepares four types of financial statements every quarter and every year: The balance sheet, P&L Statement, Cash flow statement, and last the statement of retained earnings. In the profit and loss report, also referred to as the income details; the company lists out all its expenses and revenue. When revenue exceeds expenditures, the company is earning a profit. As well as when the expenditures are more than the company revenue, the company has incurred a loss.

Here are the short essay and articles for Profit and Loss (P&L) Account – Meaning, Definition, and Advantages.

It is counting by taking a business’s total revenue and subtracting the total expenses, including tax. If the report figures out we know as net income is negative, the company has earned a loss; and, if it is positive, the company has made a profit. A P&L account reports and statements are important to investors and traders as they offer an in-depth look at company performance. Generally, one negative profit & loss is seen as a warning sign, while a few in succession are taken to mean that there could be something fundamentally wrong with the company’s operations.

Meaning and Definition of Profit and Loss (P&L) Account:

What is a profit and loss (P&L) account? A P&L account shows a company’s revenue and expenses over a particular period of time; typically either one month or consolidated months over a year. These figures show whether your company has earned a profit or a loss over that time period. P&L accounts show your net revenue and expenses; and, also show whether your profession has earned more income than it has spent on its running costs.

If that is the case, then your business has earned a profit. The P&L account represents the benefit of a profession. It cannot, for example, show you if you are running out of cash as you construct stock. Overall want to know what net profit & loss increase or decrease, for this kind of insight, you need a balance sheet. The P&L account is also known as a P&L report, an income statement, a statement of operation, a statement of financial results, or an income and expense statement.

Benefits or Advantages of Profit and Loss (P&L) Account:

The following benefits and advantages of the profit and loss account below are:

For information on Net results; They give the actual information about net profit or a net loss of the business for an accounting period. So, it is very useful to know the financial condition of the firm.

For the knowledge of Total Expenses; They give actual information about indirect expenses.

Assessment of Ratio; They serve to assess and fixate the ratio between net profit to sales; and, the ratio between net profit to operating expenses. It helps to understand the direction capacity of the firm.

Controlling of Profit and loss; They help in control and detaining indirect or non-expenses by providing important information about these expenses.

Profit and Loss Account: Meaning, Definition, and Advantages; Image from Pixabay.

Disadvantages and limitations of Profit and Loss (P&L) Account:

The following disadvantages of the profit and loss account below are:

The main disadvantage that comes to mind when thinking about P&L accounting is accuracy. Data on depreciation and asset value is usually subjective or volatile; and, it is difficult to attribute accurate values to these fields. Nevertheless, these factors weigh heavily on a P&L account.

Also, when a manager is constantly using a P&L account to make his/her business decisions, choices end up being made on a relatively small sample of data, with only the short-term in mind.

The P&L account is ready and prepares for a certain period and hence it is an interim report. In an absolute sense, the true profits or losses can ascertain only after the concern has run its entire life; a point at which all the inputs to the business from its start-up to its final liquidation can ascertain and can arrive at the precise profit for its whole life.

But since this is not possible, the P&L account prepares at regular intervals by estimating what proportion of the life profit of the company has been earned in a particular period. To arrive at this estimate, the accountant has to make many assumptions about the future of the company and the uncertainties that surround it.

The profit as disclosed by the P&L account is not absolute but is relative as the profit & loss account is based upon various accounting conventions and concepts, and depends upon the correct opinion of revenue and count of expired costs.

The different types of Financial Accounting; Financial accounting classifies under the head of accounting functions that specifically maintain the financial transactions of companies; Accounting essay; Financial accounting explains the different types with their objectives or intentions or motives. The guidelines under accounting use to summarize and classify all transactions; It also involves preparing the financial statements of a company which gives an overview of the economic stability of a company to its investors.

This article can explain the Financial accounting different types with their objectives or intentions or motives.

This pertains to the recording of all business transactions in the books of prime entry, posting them into respective ledger accounts, balancing them, and preparing a trial balance, from and out of which a profit and loss account showing the results of the business and also a balance sheet depicting assets and liabilities of the business concern is prepared. This in turn forms the basis for analysis and interpretation for furnishing meaningful data to the management.

The Accounting essays in types of accounting are part, both methods rely on the same conceptual framework of double-entry accounting for recording and reporting analysis data at the end of a certain period; Two types or methods of financial accounting are cash and accrual or remedial account; Although they differ, both methods rely on the same conceptual framework as double-entry accounting for recording, analyzing, and reporting at the end of a given period of time; Such as a month, quarter or financial year.

The information generated by accounting is used by various interested groups such as individuals, managers, investors, creditors, government, regulatory agencies, taxation authorities, employees, trade unions, consumers, and the general public. Depending on the purpose and method, accounting can be broad of three types; 1] financial accounting, 2] cost accounting, and 3] management accounting. Financial accounting is mainly concerned with the preparation of financial statements. It is used on some well-defined concepts and conventions and helps formulate comprehensive financial policies.

Cash Account:

If you are the owner of a business, by adopting cash accounting you can only focus on corporate transactions involving cash. Other economic events with no monetary input do not matter because they do not make it to the financial statements. The business prefers to go for the cash accounting method only to focus on cash transactions that involve cash. Any other transaction that does not include any monetary value does not go into the financial statements.

Under this method, all-cash credit cash entries are based on the number of related loans and transactions carried out. Under the cash accounting method, a corporate bookkeeper always debits or credits the cash account in each journal entry on a transaction basis. For example, to record customer remittances, the bookkeeper debits the cash account and credits the sales revenue account. Do not mistake cash debit accounting for banking debit. The former means an increase in the company’s money, while the latter reduces the money in the customer’s account.

Accrual Account:

The records of the company maintain the transaction under all modes irrespective of any monetary value. It also involves making entries about cash which is beyond other transactions that do not include monetary transactions. The method acquired in financial accounting is depositing an item and recording it legally when a cash transaction occurs. Under the contingency method of accounting, a company records all transaction data regardless of monetary inflows or outflows.

In other words, this accounting type incorporates the cash accounting method but takes into account all transactions that carry out the operating activities of the corporation. In a financial dictionary, “earned” means an item to store and record as legally binding, even if there is no cash payment.

The phrases “accounts payable” and “accounts receivable” perfectly illustrate the concept of pronunciation. The accounting, also known as the payable seller, represents the amount of money that the seller of a business paid at a given point in time. The entity accrues the debtors until it settles the underlying debts. The same analysis applies to customers. Receivables are another name for accounts receivable that represent the money customers pay to a business.

What are the different types of Financial Accounting? Image from Pixabay.

Objectives or intentions or motives of financial accounting:

What are the intentions or motives of financial accounting? Knowing the goals of financial accounting can have the effect of being an accountant and truly understanding what your business is doing. Accounting Objectives; Accounting norms can appear to be unfamiliar and discretionary; however, by learning the calculated structure you will have a reasonable foundation to comprehend the hypothesis of accounting rules without falling back on repetition retention. The goal of financial accounting is to give data to the end-client; however, the calculated system, or Statements of Financial Accounting Concepts (SFAC), mentions to us what characteristics that data must-have.

Significance:

For data to be valuable to end-clients, it must be important. That implies that it must assistance a financial assertion peruser to settle on choices about the financial prosperity of the organization. For financial specialists, this verifiable think back serves to help settle on venture choices. To be important, data should likewise be current. Organizations report financial outcomes on a quarterly or yearly premise to fulfill this target. End-clients need the latest data conceivable to settle on the best choices.

Unwavering quality:

Accounting data must be solid. If an organization doesn’t create dependable financial proclamations, at that point speculators can’t pick up the data they have to decide. Dependable data can check, is liberated from predisposition, and isn’t deceiving. To assist organizations with meeting this goal, public bookkeepers will freely confirm accounting medicines and exchanges and issue conclusions dependent on these reviews. This makes end-clients more all right with their dependence on financial data.

It is both Reliability and Relevance; A significant target is to get ready for such financial proclamations that are dependable, and choices can found on it. For this reason, such Accounting should speak to a dependable portrayal of exchanges and occasions embraced by the business, ought to speak to in their genuine substance and monetary reality point of view.

Straightforward:

Among all the goals examined above, it is the essential target that Financial Accounts are set up so that they are effectively justifiable by proposed clients. Nonetheless, while meeting this goal as a primary concern; it must be similarly fundamental to guarantee that no material data discard because it will be mind-boggling and unwieldy to comprehend for different clients. To put it plainly, endeavors must make to plan Financial Accounts simply to know at every possible opportunity.

Similarity:

An auxiliary nature of financial data is that it must be equivalent. This is the reason we have a setup arrangement for recording and detailing accounting data. Financial specialists regularly are given decisions on where and when to contribute. By having tantamount information, these speculators can make relative decisions about their venture openings. Nonetheless, similarity, being an auxiliary quality, must take on a supporting role to pertinence and dependability.

Consistency:

Consistency is another auxiliary nature of financial data. Since end clients are frequently given financial data that traverses different timeframes; these clients should have the option to look at data across financial periods. As guidelines change, and as organizations change, it won’t generally be conceivable to have totally steady data. Be that as it may, when accounting data isn’t steady, norms require the revelation of the irregularity. This is a case of the essential nature of dependability taking a front seat to the optional nature of consistency.

Meeting the Objective of Various Stakeholders:

Another fundamental target is addressing the requirements of different partners, which are related to the business. Various partners have various purposes, for example; loan specialists to the business mean to evaluate the ability of the business to pay interest and head; which loan to the business or planned moneylenders; so they are more intrigued by the dissolvability of the business and spotlight on that perspective. Additionally, clients are keen on knowing the development and steadiness of the business and spotlight more on income explanations; and, financial articulations to decide the capacity of the business to give better business terms and a reliable gracefully of products and enterprises.

What is ABC (activity based costing)? It is the collection of financial, operational, performance information tracing the significant activities of the firm to product costs in production management. In other words, the knowledge of find out estimates costs of production for product costs.

What does mean ABC (activity based costing)? Meaning, Definition, Features or characteristics, advantages, and disadvantages.

Activity-based costing (ABC) is a new term develop for finding out the cost. The basic feature of ABC is its focus on activities as the fundamental cost objects. It uses activities as the basis for calculating the costs of products and services. The Activity-Based Costing (ABC) is a costing system, which focuses on activities performed to produce products. ABC is the costing in which costs first trace to activities and then to products. This costing system assumes that activities are responsible for the incurrence of costs and create the demands for activities.

For example, an online learning firm prepares tax returns; suppose Udemy teaches online students. Fees charge to products based on individual product’s use of each activity. In the traditional absorption costing system, fees first trace not to activities but an organizational unit, such as a department or plant and then to products. It means under both, ABC and traditional absorption costing system the second and final stage consists of tracing fees to the course.

Activity Based Costing: Meaning, Features, and Advantages; Image from Pixabay.

Definition of ABC (activity based costing):

What is the ABC (activity based costing) definition? The following ABC definitions below;

According to CIMA as;

“Cost attribution to cost units on the basis of the benefit received from indirect activities e.g. ordering, setting up, assuring quality.”

According to CAM-1 organization of Arlinton Texas as;

“The collection of financial and operational performance information tracing the significant activities of the firm to product Costs.”

It bases on the belief that in the production process various activities give rise to costs. Generally, Activity Based Costing (ABC) defines as an accounting technique that allows an organization to determine the actual cost associated with each product and service produced by the organization without regard to the organizational structure. Amongst various benefits associated with the ABC approach, one of the major ones is that it helps to define the activities of the organization in terms of value-adding activities.

Features or Highlights or Characteristics of ABC (activity based costing):

What are the ABC (activity based costing) features or highlights or characteristics? The following ABC features below;

The simple traditional distinction made between fixed cost and variable cost is not enough to guide to provide quality information to design a cost system.

It is a two-stage product costing method that first assigns costs to activities and then allocates them to products based on each product’s consumption of activities.

They can use by any organization that wants a better understanding of the costs of the goods and services it provides, including manufacturing, service, and even non- profit organizations.

The cost pools in the two-stage approach now accumulate activity-related costs.

An activity is any discrete task that an organization undertakes to make or deliver a product or service.

It bases on the concept that products consume activities and activities to consume resources.

The more appropriate distinction between cost behavior patterns is scale related, scope related, decisions related, and time-related. In other words, cost behavior is all performance-related product costs.

Cost drivers need to identify. A cost driver is a structural determinant of cost-related activity. The logic behind this is that cost drivers dictate the cost behavior pattern. In tracing overhead cost to the product, a cost behavior pattern must understand so that appropriate cost drivers could identify.

ABC cost method is activity-based cost management:

What is activity-based cost management? Cost management is an accounting method that calculates material costs, labor costs, management costs, financial costs, etc. according to certain standards by the current accounting system.

This management approach sometimes fails to reflect the direct link between the activities undertaken and costs. Also, the ABC cost method is equivalent to a filter. It readjusts the original cost method so that people can see the direct connection between the cost consumption and the work they engage in so that people can analyze which cost inputs are effective. Which cost inputs are invalid.

The ABC (activity based costing) cost method mainly focuses on the production and operation process, strengthens operation management, focuses on specific activities and corresponding costs, and strengthens activity-based cost management.

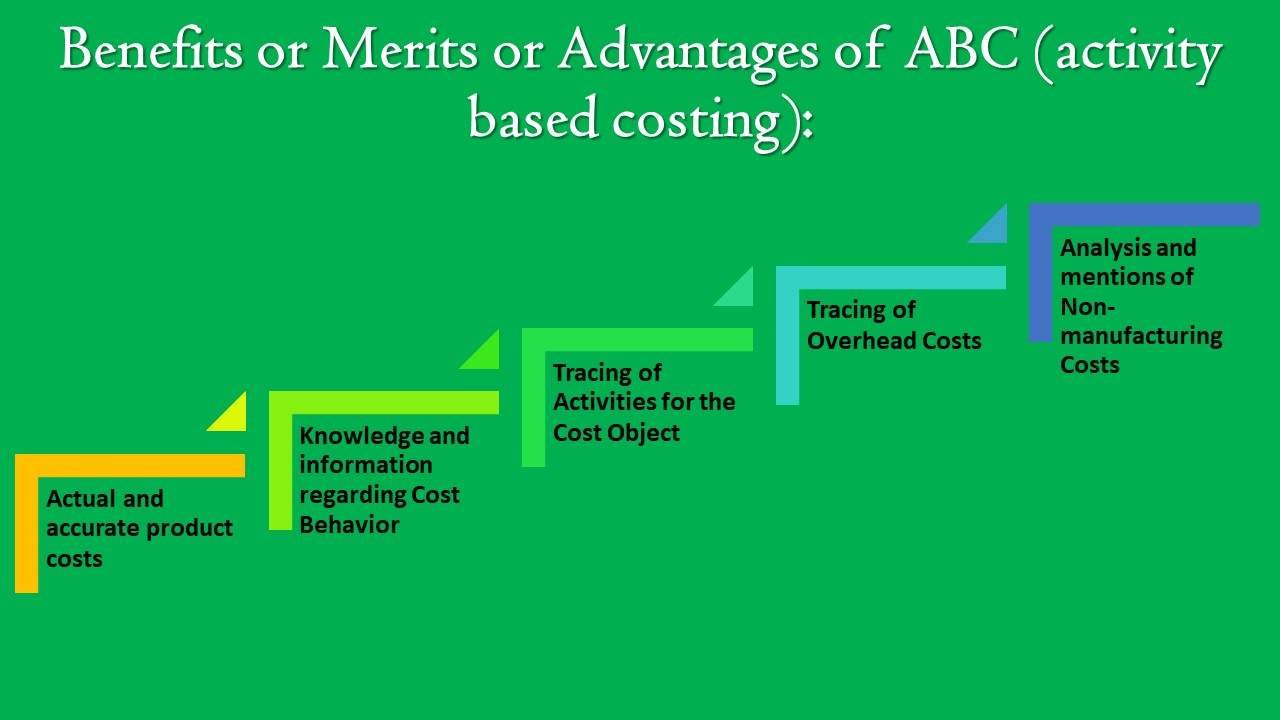

Benefits or Merits or Advantages of ABC (activity based costing):

What are the ABC (activity based costing) benefits or merits or advantages? The following ABC advantages below;

Actual and accurate product costs:

ABC brings actual, accuracy, and reliability in product costs determination by focusing on cause and effect relationships in the incurrence of the cost. It recognizes that it is activities which cause producing costs, not products and it is a product which consumes activities. In advanced manufacturing environment and technology where support functions over-heads constitute a large share of total or overall costs, ABC provides more realistic product costs. It produces reliable and correct product cost data in case of greater diversity among the products manufactured such as low-volume products, high-volume products.

Knowledge and information regarding Cost Behavior:

It identifies the real nature of cost behavior and helps in reducing costs and identifying activities that do not add value to the product, in other words producing costs. With ABC, managers can control many fixed overhead costs by exercising more control over the activities which have caused these fixed overhead costs. This is possible since the behavior of many fixed overhead costs about activities now becomes more visible and clear.

Tracing of Activities for the Cost Object:

ABC uses multiple cost drivers, many of which transaction-based rather than product volume. Further, ABC concern with all activities within and beyond the factory to trace more overheads to the products.

Tracing of Overhead Costs:

ABC traces costs to areas of managerial responsibility, processes, customers, departments besides the product costs. Costs tracing, accurate allocation of costs to various products lead to proper pricing policy. Also, Cost driver rates can use advantageously for the design of new products or existing products as they indicate overhead costs that are likely to apply in costing the product.

Analysis and mentions of Non-manufacturing Costs:

Some costs term as non-manufacturing costs; for example, product promotion or advertisement. Even though, advertising is a non-manufacturing cost which constitutes a major portion of the total cost of any product. These non-manufacturing costs can be easily allocated since the relationship between costs; and, their causes can properly understand by using ABC.

Limitations or Demerits or Disadvantages of ABC (activity based costing):

What are the ABC (activity based costing) limitations or demerits or disadvantages? The following ABC disadvantages below;

Service costs are High:

Implementing an ABC system requires substantial resources, which is costly to maintain.

Report or data collection problem:

It is a complex system which needs a lot of record for calculations.

Non-useable for small organizations:

In small organizations, the CEO or owner or managers accustom to using traditional costing systems to run their operations and traditional costing systems often use in performance evaluations. Some companies are producing only one product or a few products; so, the ABC cannot apply in there.

Activation or selection problem:

Some difficulties emerge in the implementation of the ABC system; such as the selection of cost drivers, assignment of common costs, varying cost driver rates, etc.

Different timeline of terms:

Since there are a lot of steps and groundwork required to come out with a costing based on this system, it is quite a time to consume. For example, large companies for the best costing system they produce the large size of production and give many products to us, but small or single handle company produces and give a single product. So, the large or multinational company collects many records and ABC work easy for long-term periods, as well as small organizations for difficult in short-term periods.

Understand the concept of Trial Balance [In Hindi]. Learn about its meaning, definition, objectives, advantages, methods, and limitations. It is a listing of all the accounts and their respective balances. It is a statement of debit balance and credit balance extracted from ledger accounts on a particular date. This article explains Trial Balance with the topic of Introduction, Meaning, Definition, Objectives, Advantages, Methods, and Limitations. It is a two-column schedule listing the titles and balances of all the accounts in the order in which they appear in the ledger. The debit balances lists in the left-hand column and the credit balances in the right-hand column. In the case of General Ledger, the totals of the two columns should agree.

Here is the article explaining Trial Balance with the topic of Introduction, Meaning, Definition, Objectives, Advantages, Methods, and Limitations in accounting.

We, now, know the fundamental principle of the double-entry system of accounting where for every debit, there must be a corresponding credit. Therefore, for every debit or a series of debits given to one or several accounts, there is a corresponding credit or a series of credits of an equal amount given to some other account or accounts and vice-versa. Hence, according to this principle, the total of debit amounts must equal the credit amounts of the ledger at any date. If the various accounts in the ledger are balanced, then the total of all debit balances must be equal to the total of all credit balances.

If the same is not true then the books of accounts are arithmetically inaccurate. It is, therefore, at the end of the financial year or at any other time, the balances of all the ledger account extract and record in a statement known as Trial Balance and finally totaled up to see whether the total of debit balances is equal to the total of credit balances.

Meaning of Trial Balance:

They may thus define as a statement of debit and credit totals or balances extracted from the various accounts in the ledger books to test the arithmetical accuracy of the books. The agreement of the Trial Balance reveals that both the aspects of each transaction have been recorded and that the books are arithmetically accurate. If both sides of Trial Balance do not agree with each other, it shows that there are some errors, which must detect and rectify if the correct final accounts are to prepare.

Thus, Trial Balance forms a connecting link between the ledger accounts and the final accounts. It is a statement of debit and credit balances taken out from all ledger accounts including cash books. The golden rules that “Accounting equation remains balanced all the time” and “For every business transaction there is an equal debit and credit” shall always prevail in the whole accounting theory. Therefore, the total of all debit balances must be equal to the total of all credit balances. To verify this, a schedule known as they prepare.

Balances of debits and credits are to extract from all ledger accounts, including cash books, and shown in this schedule. This schedule prepares to assure the management of the arithmetical accuracy of books of accounts. This schedule facilitates the preparation of final accounts. Generally, it prepares at the end of each accounting year; however, it can prepare at the end of each month, quarter, or the end of any chosen period.

Definition of Trial Balance:

It is a list of debit and credit balances of all the ledger accounts extracted on a given date. Following are the main definitions of the trial balance;

Accounting in the first definition is as,

“Trail balance is the list of debit and credit balances, taken out from the ledger, it also includes the balances of cash and bank taken from the cash book.”

Accounting in the second definition is as,

“The statement prepared with the help of ledger balances at the end of the financial year (or at any other date) to find out whether debt total agrees with credit total is called a trial balance.”

When one account debit, another account credit with an equal amount. Therefore, it is quite evident that the total of debit balances of the ledger accounts of given transactions will be equal to the total of the credit balances. It must state here that the total of the debit balance column must be equal to the total of the credit balance column. This is so because under the double-entry system, for each item of debit there is a corresponding credit, and secondly all the transactions recorded in the books of original entry transfer to the ledger.

Objectives of Trial Balance:

The following are the main objectives of preparing the trial balance:

1] To check the arithmetical accuracy of books of accounts:

According to the principle of the double-entry system of book-keeping, every business transaction has two aspects, debit and credit. They base on the double-entry principle of debit equals credit or credit equals debt. As a result, the debit and credit columns of they must always be equal. If they do, it assumes that the recordings of financial transactions are accurate.

Conversely, if they do not, it assumes that they are not arithmetically accurate. Therefore, one important purpose of preparing trial balance is to provide a check on the arithmetical accuracy of the recordings of the financial transactions. So, the agreement of the trial balance is proof of the arithmetical accuracy of the books of accounts. However, it is not conclusive evidence of their accuracy as there may be certain errors. Which they may not be able to disclose.

2] Helpful in preparing final accounts:

They record the balances of all the ledger accounts at one place which helps in the preparation of final accounts, i.e. Trading and Profit and Loss Account and Balance Sheet [Hindi]. But, unless they agree, the final accounts cannot prepare. Final accounts prepare to show profit and loss and the financial position of the business at the end of an accounting period.

These accounts prepare by using the debit and credit of all ledger accounts. Therefore, since the trial balance is a statement of the debit and credit balances of the ledger accounts, it provides the basis for the preparation of the final accounts. So, if the trial balance does not agree, errors locate and necessary corrections are made at the earliest. So, that there may not be unnecessary delay in the preparation of the final accounts.

3] To serve as an aid to the management:

By comparing the trial balances of different years changes in figures of certain important items such as purchases, sales, debtors, etc. ascertain and their analysis make for taking managerial decisions. So, it serves as an aid to the management.

4] To Summarize the financial transactions: